Beige Book shows concerns about trade policy

Manufacturing was mixed, but two-thirds of districts said activity was little changed or had declined.

Manufacturing was mixed, but two-thirds of districts said activity was little changed or had declined.

SMU’s flat-rolled steel prices were flat or lower as tariff-related uncertainty continued to drag on the market.

The market appears to be pausing after a turbulent run. But tension remains just beneath the surface. With net long positioning still elevated, sentiment-driven selling could quickly reignite volatility. Still, supply constraints and limited imports are laying the groundwork for a resilient physical market. This moment of calm feels more like a crossroads than a conclusion.

Meanwhile, an increasing number think it's too early to say whether the penalties are going to bring more manufacturing to the US.

Steel buyers responding to this week’s SMU market survey report a continued softening in sheet lead times. Meanwhile, plate lead times have moderately extended and are at a one-year high.

Nearly half of the steel buyers responding to this week’s SMU market survey say domestic mills are showing increased willingness to negotiate pricing on new spot orders. This marks a significant shift from the firmer stance mills held in prior weeks.

Current Sentiment Index dropped six points to +42 this week compared to two weeks earlier. It has fallen in every successive survey since reaching a 2025 high of +66 on Feb. 19.

Steel prices slipped again this week, with all five of SMU’s sheet and plate indices trending lower for the second week in a row.

Firms were pessimistic, with the future general business conditions index falling to its second lowest reading in the more than 20-year history of the survey

A look at the HR futures market.

This week is the first time all of our indices have moved lower in unison since July 2024.

The construction sector added 13,000 jobs, seasonally adjusted, in March, but tariffs could undermine the industry.

Supply chains are working through what the tariffs mean for them

Market dynamics are shifting rapidly, with futures pricing diverging from physical fundamentals, creating a complex landscape for steel traders.

Buyers responding to our latest market survey reported that sheet lead times continue to gradually decline from recent highs. Meanwhile, plate lead times increased to levels last seen one year ago.

Four out of every five steel buyers who responded to our latest market survey say domestic mills are unwilling to negotiate on new order spot pricing. Mills have shown little flexibility on pricing for nearly two months.

Sheet and plate prices were mixed on Tuesday as the market took a wait-and-see approach to the Trump administration’s “Liberation Day” tariffs.

US manufacturing activity slowed in March after two straight months of expansion, according to supply executives contributing to the Institute for Supply Management (ISM)’s latest report.

The Chicago Business Barometer increased for the third-consecutive month in March. Despite this, it still reflects contracting business conditions, as it has since December 2023.

Another eventful week in the physical and financial steel markets is coming to a close, but with a markedly different tone than the last update at the end of February.

Transportation equipment led the increase, rising 1.5% to $98.3 billion.

SMU's steel price indices moved in differing directions this week but remained largely stable as cautious buyers await clarity on pending steel tariffs and trade cases.

People remain concerned about inflation, trade policies, and tariffs.

SMU’s Buyers’ Sentiment Indices showed mixed movements this week but remain strong, reflecting continued confidence among steel buyers.

Are President Trump's tariff policies helping? Steel buyers offer their opinions on the impact of Trump's tariffs.

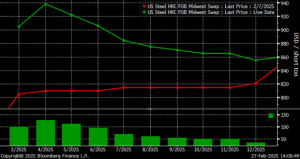

Over the past couple of weeks, Midwest HRC futures have been drifting lower on light volume. This begs the question if the rally has run out of steam, or is it catching its breath after ripping roughly $150 in less than two weeks? The April CME Midwest HRC future made an intraday high at $976 […]

After a multi-week increase, buyers responding to our market survey this week reported that lead times are stabilizing or marginally declining for each of the sheet and plate products we track.

Single-family starts last month hit a rate of 1.10 million, a month-over-month increase of 11.4%, census data shows.

The majority of the steel buyers responding to our latest market survey continue to report that domestic mills remain firm on pricing, showing little willingness to talk price on new spot orders this week.

The ABI is a leading indicator for near-term nonresidential construction activity and projects business conditions ~9-12 months down the road (the typical lead time between architecture billings and construction spending).