Market Data

April 22, 2025

SMU price ranges: Tags flat or down, sheet momentum 'lower'

Written by Brett Linton & Michael Cowden

SMU’s flat-rolled steel prices were flat or lower as tariff-related uncertainty continued to drag on the market.

The prices

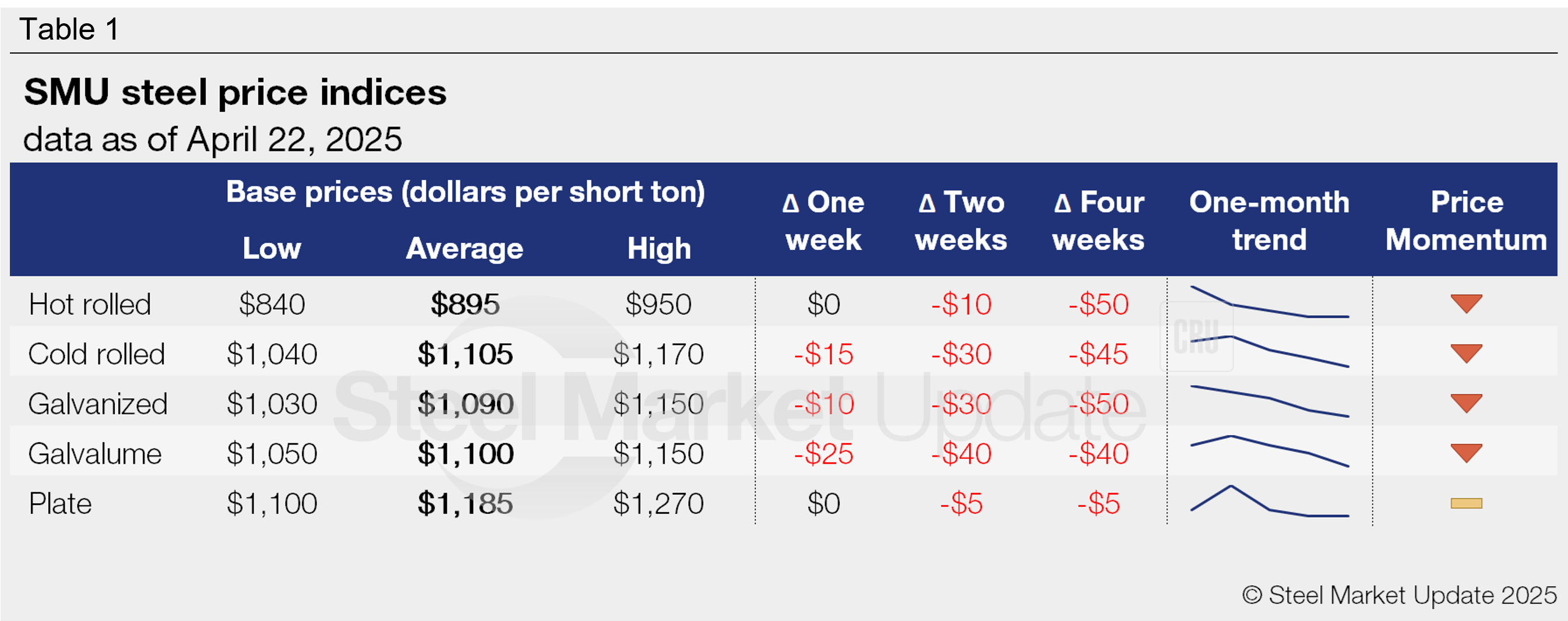

Our hot-rolled coil price stands at $895 per short ton (st) on average. That’s unchanged from a week ago and comes after four consecutive weeks of declining prices.

The high end of our range remains at $950/st, which is where smaller spot tonnage from certain mills is transacting. The lower end of our range continues to be $840/st. That’s where tonnage from new capacity is or from mills competing with that new capacity. Also, large spot buyers, those capable of buying tens of thousands of tons, are in the mid/low $800s/st, market participants said.

Prices for cold-rolled (CR) and coated products, in contrast, continued to tick lower. SMU’s CR price stands at $1,105/st on average, down $15/st from last week. Galvanized base prices are at $1,090/st on average (down $10/st). And Galvalume base prices are at $1,100/st (down $25/st).

Plate prices, meanwhile, were unchanged at $1,185/st.

Sheet momentum lower, plate remains at neutral

SMU has also adjusted all its sheet price momentum indicators from neutral to lower.

Recall that we adjusted sheet momentum higher in late January following Trump’s inauguration. We changed it to neutral on April 8, after “Liberation Day” tariffs on April 2 roiled markets. We last had momentum lower in late October, during a period of weak prices last fall.

We made the adjustment to lower following several weeks of declining sheet prices, lower scrap prices earlier this month, and signs of weakness in the scrap export market. We also adjusted them lower on shorter lead times, a decrease in sentiment, and mills’ increasing willingness to negotiate lower prices.

Market commentary

In short, the trends we saw in February and March, when panic buying ahead of Section 232 gripped the market, have reversed on concerns about the broader “Liberation Day” tariffs and their impact on supply chains.

To be clear, the music hasn’t stopped on demand. But while some sources say demand remains on firm footing, others tell us that they have seen a notable drop in activity more recently. The result: some market participants tell us they are buying only as needed or only to their contract minimums.

At the same time, most spring maintenance outages have been wrapped up, and significant maintenance activity isn’t likely to occur again until next fall. Also, there are concerns about seasonally slower activity as lead times stretch closer to the summer months. And some sources noted that tariffs could hurt export-oriented markets, such as agriculture, or those with complex supply chains, such as automotive.

Refer to Table 1 (click to enlarge) for our latest price indices and trends.

Hot-rolled coil

The SMU price range is $840-950/st, averaging $895/st FOB mill, east of the Rockies. Our range is unchanged w/w. Our price momentum indicator for hot-rolled steel has been adjusted to lower, meaning we expect prices to decline over the next 30 days.

Hot rolled lead times range from 3-6 weeks, averaging 5.0 weeks as of our April 16 market survey.

Cold-rolled coil

The SMU price range is $1,040–1,170/st, averaging $1,105/st FOB mill, east of the Rockies. The lower end of our range is down $20/st w/w, while the top end is down $10/st. Our overall average is down $15/st w/w. Our price momentum indicator for cold-rolled steel has been adjusted to lower, meaning we expect prices to decline over the next 30 days.

Cold rolled lead times range from 5-8 weeks, averaging 6.6 weeks through our latest survey.

Galvanized coil

The SMU price range is $1,030–1,150/st, averaging $1,090/st FOB mill, east of the Rockies. The lower end of our range is unchanged w/w, while the top end is down $20/st. Our overall average is down $10/st w/w. Our price momentum indicator for galvanized steel has been adjusted to lower, meaning we expect prices to decline over the next 30 days.

Galvanized .060” G90 benchmark: SMU price range is $1,127–1,247/st, averaging $1,187/st FOB mill, east of the Rockies.

Galvanized lead times range from 4-8 weeks, averaging 6.8 weeks through our latest survey.

Galvalume coil

The SMU price range is $1,050–1,150/st, averaging $1,100/st FOB mill, east of the Rockies. The lower end of our range is down $10/st w/w, while the top end is down $40/st. Our overall average is down $25/st w/w. Our price momentum indicator for Galvalume steel has been adjusted to lower, meaning we expect prices to decline over the next 30 days.

Galvalume .0142” AZ50, grade 80 benchmark: SMU price range is $1,344–1,444/st, averaging $1,394/st FOB mill, east of the Rockies.

Galvalume lead times range from 7-9 weeks, averaging 7.5 weeks through our latest survey.

Plate

The SMU price range is $1,100–1,270/st, averaging $1,185/st FOB mill. Our range is unchanged w/w. Our price momentum indicator for plate remains at neutral, meaning we see no clear direction for prices over the next 30 days.

Plate lead times range from 4-7 weeks, averaging 5.9 weeks through our latest survey.

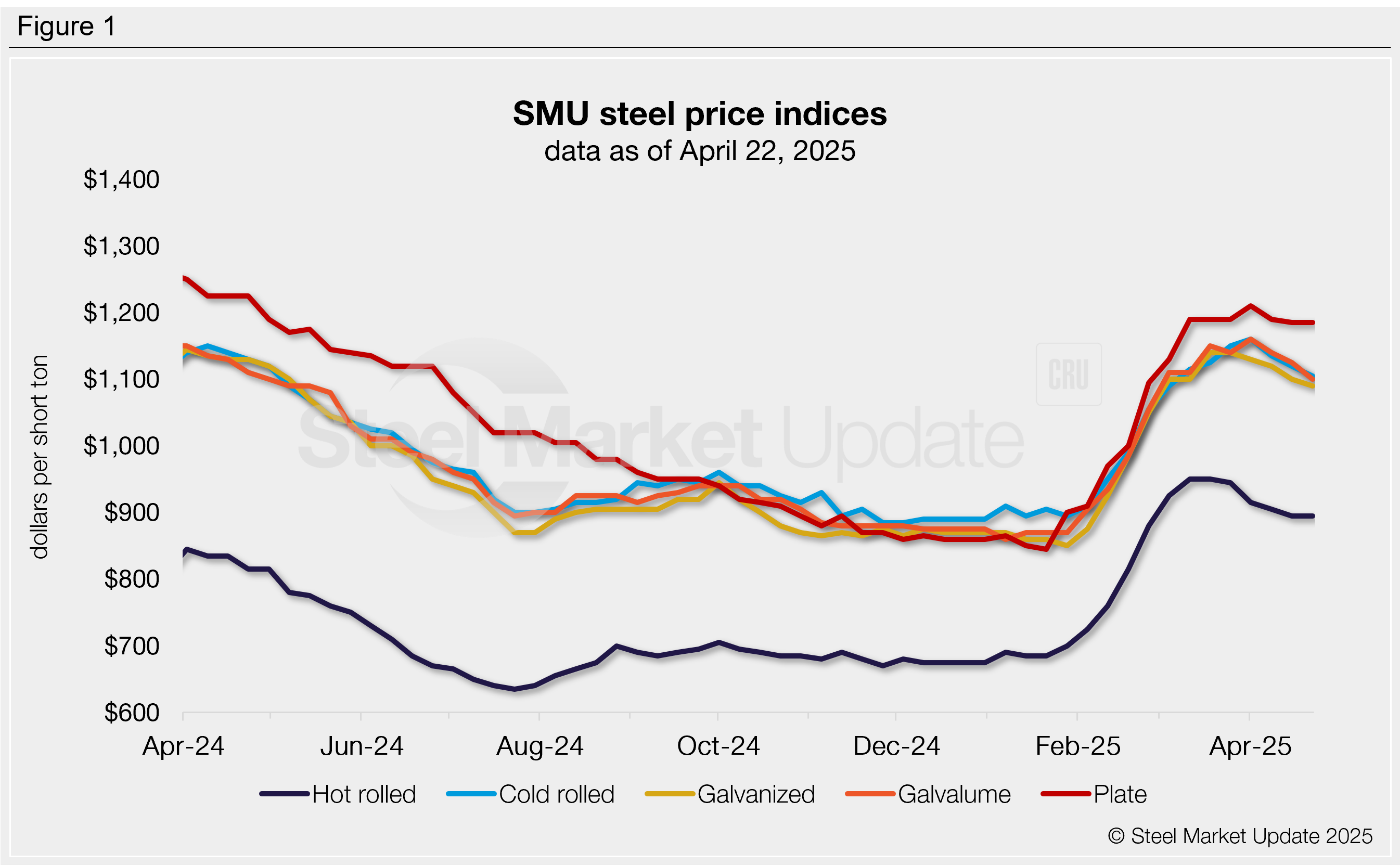

SMU note: Above is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume, and plate price history. This data is also available on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@steelmarketupdate.com.

Brett Linton

Read more from Brett Linton