Prices

July 20, 2017

July Foreign Steel Imports Poised to Break 3.5 Million Tons

Written by John Packard

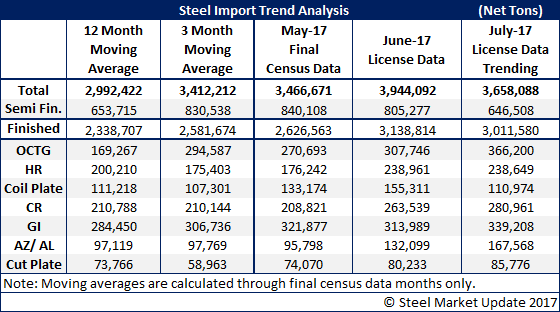

The U.S. Department of Commerce (DOC) released new foreign steel import license data on July 18. The trend for July is for steel imports to remain quite high, in the mid 3-million-net-ton range. We expect imports to be lower than June’s 3.9 million net tons, but above the 12-month and 3-month moving averages.

Finished steel imports (removing slabs/billets from the data) are anticipated to reach 3.0 million net tons.

Slab/billet imports are trending lower for some reason. Semi-finished steels (slabs/billets/blooms) are only purchased by steel producers, from which they roll sheet, long products and pipe and tube.

With Section 232 recommendations about to be released, don’t be surprised if items on the graphic below are all hit to some degree. South Korea, with no oil drilling industry of its own, is the largest exporter of OCTG (oil country tubular goods), tripling what is coming from Mexico and quadruple the OCTG exports of Argentina. Other top exporters by tonnage on OCTG are Taiwan, Austria and Brazil.

Hot rolled numbers have been growing with Turkey now taking top honors (pushing Canada out of the way). In third through fifth place are: Egypt, Italy and Germany.

Cold rolled and coated (galvanized and Galvalume) are all growing. CRC imports are poised to be +100,000 tons greater than both the 12-month and 3-month moving averages.

Galvanized is another sticky wicket, trending toward the low to mid 300,000 net tons. The top importers so far this month are: Canada, South Africa, Turkey and Taiwan. Vietnam tonnage is being scaled back as is UAE and South Korea.

Galvalume/aluminized are also poised to bring in large tonnage for the niche products. July is on pace to collect 167,000+, well above its 12-month and 3-month moving averages.