CRU

June 13, 2021

CRU: Scrap Exporting Markets Play Catchup During June Trade

Written by Ryan McKinley

By Senior Analyst Ryan McKinley, from CRU’s Steelmaking Metallics Monitor

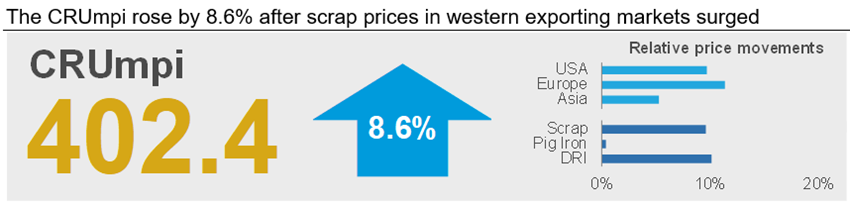

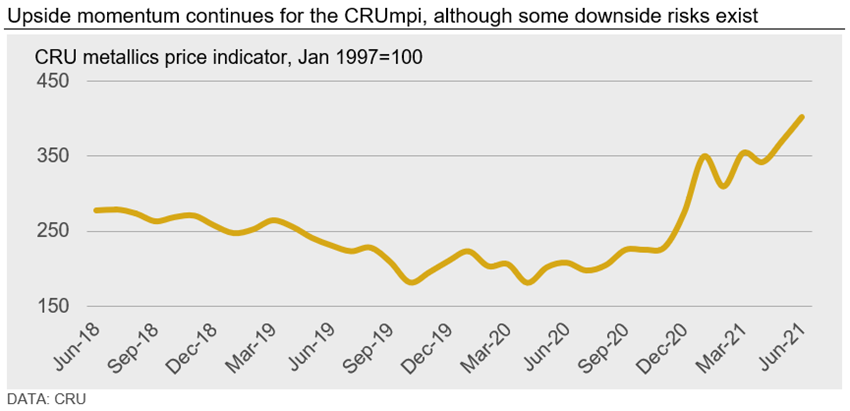

The CRU metallics price indicator (CRUmpi) increased by 8.6% m/m in June to 402.4. This increase is primarily a reflection of large price increases for scrap in Europe and the U.S., although some increases occurred in Asia as well.

After rising substantially in May, pig iron price movements were much more subdued as importers pushed back on higher-priced offers.

Prices in scrap exporting markets rose notably in June, and markets in the West, like the U.S. and Europe, rose by more than those in the East, like Japan. In the U.S., strong demand both domestically and abroad resulted in a strong increase in obsolete grade pricing, while supply-side issues resulted in an even larger increase for prime grades. Similar forces created an uplift in European prices as well, and European mills are now paying a premium to Turkish mills as they attempt to secure higher-quality shredded scrap as a substitute for prime grades. China was the only market where prices declined m/m. This decrease was in part caused by potential government action seeking to curb commodity prices in general. While this decrease did not carry over to the rest of Asia, prices in the region in overall were little changed m/m.

Steel capacity utilisation rates in the U.S. passed the 80% mark in late-May for the first time since the beginning of the Covid-19 pandemic. With finished steel demand high and prices at record levels, mills increased scrap prices substantially m/m to ensure they had enough supply to meet their needs. While both prime grades and obsolete grades rose by $50-60/long ton because of supply/demand imbalances (n.b. a large increase under more normal market conditions), steel prices continue to vastly outpace scrap.

Price increases were also substantial in Europe, even after Turkish scrap importers paused buying activity in late-May. Demand for finished steel in Europe is also strong, with German rebar prices reaching up to €830/metric ton compared to €770/ton a month earlier. This price rise has caused heightened competition between European mills for scrap and has added pressure on Turkish buyers reluctant to push their import prices higher given uncertainty in Asian steel markets. Moreover, Turkish buyers faced additional difficulties securing material at lower prices because of a recent announcement by the Russian government that it will increase its minimum duty on its own scrap exporters.

While steel and scrap markets are hot in other areas of the world, Chinese prices have fallen in recent weeks after the government signalled it will begin a crackdown on rapidly rising commodity prices. Since this development, both steel and scrap pricing within the country have fallen precipitously, tumbling by ~15% for rebar and ~9% for scrap over the course of two weeks. Sentiment has also turned bearish because of seasonally weak demand from the construction sector.

The fall in Chinese scrap prices did not carry over into other parts of Asia. In Japan, firm demand caused an increase in both domestic and export pricing even as sentiment turns more bearish in Vietnam because of falling billet prices. Overall, price movements in this region were not as strong as in other areas.

After making substantial gains in May, pig iron prices were essentially unchanged m/m around the world. Instead, prime scrap in markets like the U.S. has now caught up to a historically more normal level compared to pig iron, and importers have pushed back on higher offers. Conversely, HBI prices rose in tandem with scrap after moving little the prior month.

Outlook: Mixed signals for July price movements

Metallics demand is unlikely to fall in July m/m, providing relative stability to prices. While steel prices keep rising in most regions, there are some downside risks mounting in Asia as China pursues lowering commodity prices while seasonal pressures also weigh on steel. Meanwhile, a new Covid outbreak threatens to hamper steel demand in Vietnam.

However, China is poised to enact a new export tariff on steel, meaning Turkish exporters may become again more competitive in Asia and continue purchasing scrap at elevated price levels. For these reasons, we expect developments in the Asian market to be a leading indicator for price direction in western market for July, barring a major unforeseen event.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com