CRU aluminum news roundup

A roundup of recent aluminum news from CRU.

A roundup of recent aluminum news from CRU.

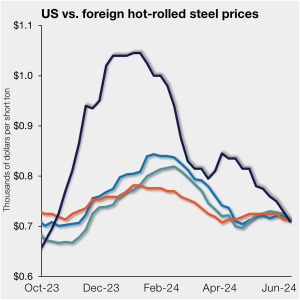

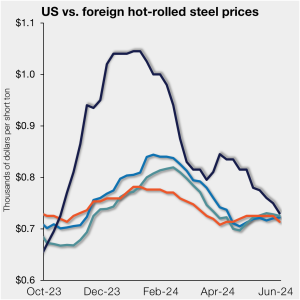

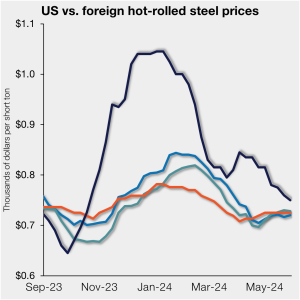

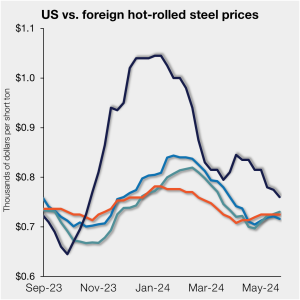

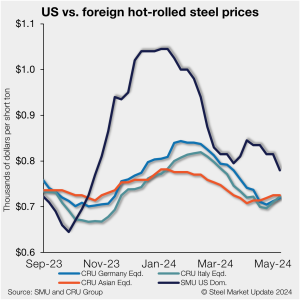

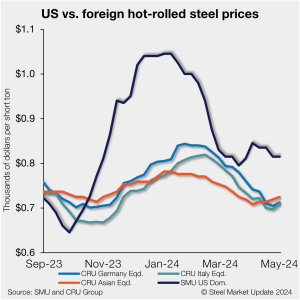

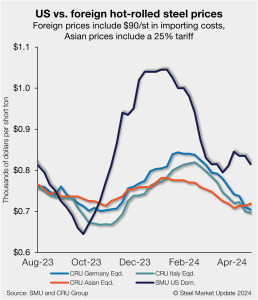

US hot-rolled (HR) coil prices fell further this past week, bringing them even with offshore hot band prices on a landed basis.

The USMCA is an important trade agreement, as long as the member countries honor its requirements. These were the sentiments echoed by top officials of the Steel Manufacturers Association (SMA) and Metals Service Center Institute (MSCI) during a press conference at their annual meeting last week in Scottsdale, Ariz.

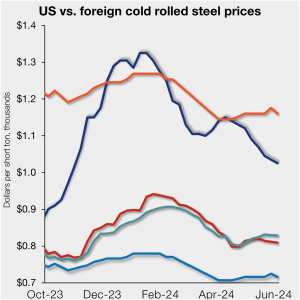

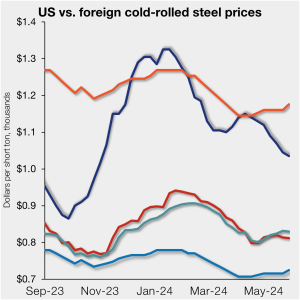

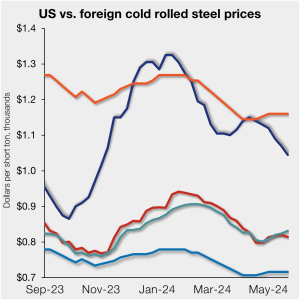

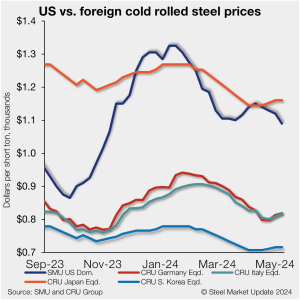

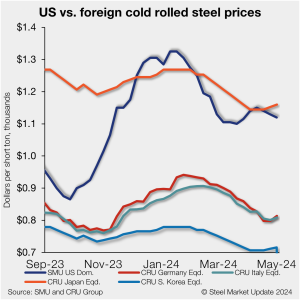

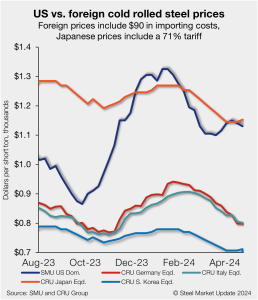

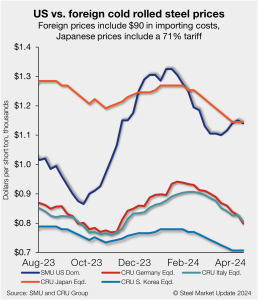

Offshore cold-rolled (CR) coil prices remain notably cheaper than domestic product. That remains the case even as US CR coil prices continue to tick lower.

US hot-rolled (HR) coil prices ticked down again this past week, nearly reaching parity with offshore hot band prices on a landed basis. This week, domestic HR coil tags were $730 per short ton (st) on average based on SMU’s latest check of the market on Tuesday, June 4. Domestic HR coil prices are now […]

When you step out of the airport in Phoenix in June, the heat tends to focus your mind. I was in town to attend the Steel Manufacturers Association/Metals Service Center Institute (MSCI) annual meeting in Scottsdale, Ariz. The desert locale with palm trees, swimming pools, and the obligatory high-powered air conditioning was fitting for 2024. Between the presidential election and the geopolitical situation, things have definitely been heating up.

President Joe Biden announced that the US will extend the suspension of Section 232 tariffs on steel products imported from Ukraine for another year. The Biden administration first lifted the 25% Section 232 tariffs on steel imports from Ukraine after the breakout of war with Russia in 2022. The initial waiver was good for one […]

Hot-rolled coil prices are known for their volatility. There are a variety of hedging strategies industry players have used to manage it, one of them being the use of HRC futures. However, some have been hesitant to dip in their toe, and their money, in futures and have preferred other approaches.

Offshore cold-rolled (CR) coil prices remain significantly cheaper than domestic product. That remains the cause even as US CR coil prices continued to tick lower. All told, US CR prices are now 17.6% more expensive than imports. While still high, that premium is down from 19.4% last week and down from 31.5% in early January.

US hot-rolled (HR) coil prices ticked down further this past week, moving closer to parity with offshore hot band prices on a landed basis. This week, domestic HR coil tags were $750/st on average based on SMU’s latest check of the market on Tuesday, May 28.

Cleveland-Cliffs is potentially eyeing a buy of NLMK USA’s Midwest assets, according to a report in Bloomberg.

The Biden administration recently announced tariffs on several products from China, including steel and aluminum. There has been much rejoicing over this move and there has been a great deal of support from the steel industry.

In conjunction with President Biden’s visit to Vietnam in September 2023, Vietnam’s government petitioned the US Department of Commerce (DOC) for “market economy” treatment. This would be a major trade concession, as DOC has recognized for years that Vietnam’s economy does not operate according to market principles. However, graduating Vietnam to market economy status would […]

The LME 3-month price for aluminum was broadly stable on the morning of May 24 and, at the writing of this article, was last seen trading at $2,627 per metric ton. The price fell sharply during the week from its recent peak amid hawkish comments from Fed officials, as indicated in the minutes of the […]

Offshore cold-rolled (CR) coil prices remain a cheaper option over domestic product, even as US CR coil prices tick lower, according to SMU’s latest check of the market.

US hot-rolled (HR) coil prices declined again and now stand nearly even with offshore hot band on a landed basis.

The USMCA should be strong enough to handle trade disagreements on steel between the US and Mexico, according to the American Iron and Steel Institute’s (AISI’s) Kevin Dempsey.

US hot-rolled (HR) coil prices saw further declines this week, while foreign prices were steady to slightly higher in the three regions we monitor

Cleveland-Cliffs’ Lourenco Goncalves thinks trade measures announced by the US government on Tuesday against China were just the opening salvo in a series of trade actions. Case in point: The Biden administration targeted China’s “unfair” trade policies with additional tariffs on an array of Chinese-made goods - including steel, aluminum, and EVs.

The Biden administration announced a series of actions on Tuesday targeting China’s "unfair" trade policies. These actions will, among other things, make imports of steel and aluminum from the Asian nation even more prohibitive.

Offshore cold-rolled (CR) coil prices remain much less expensive than domestic product, even as domestic prices have slipped to a six-month low, according to SMU’s latest check of the market.

US hot-rolled (HR) coil prices declined again, tightening their premium over offshore hot band, and moving closer to parity.

Tariffs on unfairly traded steel and other products help to stabilize America’s most important industries, safeguard tens of thousands of jobs, and protect national security. My union, the United Steelworkers (USW), never seeks these remedies lightly. And presidents, Republican and Democrat alike, implement them only after diligent investigations documenting the harm that foreign adversaries intentionally inflict upon our country with dumping, overproduction and other kinds of trade cheating. I don’t think Lewis Leibowitz considered these points while criticizing tariffs in his excessively pro-free-trade column, “Where is the voice of the consumer?” on May 5.

Is it just me, or does it seem like the summer doldrums might have arrived a little early? I could be wrong there. It’s possible we could see a jump in prices should buyers need to step back into the market to restock. I’ll be curious to see what service center inventories are when we update those figures on May 15. In the meantime, just about everyone we survey thinks HR prices have peaked or soon will. (See slide 17 in the April 26 survey.) Lead times have flattened out. And some of you tell me that you’re starting to see signs of them pulling back. (We’ll know more when we update our lead time data on Thursday.)

Foreign cold-rolled (CR) coil remains much less expensive than domestic product even as domestic prices continue to decline, according to SMU’s latest check of the market.

US hot-rolled (HR) coil price premium over offshore hot band has tightened on the back of lower domestic tags, though stateside HR coil remains markedly more expensive than imports.

Foreign cold-rolled (CR) coil remains much less expensive than domestic product, according to SMU’s latest check of the market.

US hot-rolled (HR) coil remains more expensive than offshore hot band, though with a tighter premium as prices stateside and abroad have ticked lower in recent weeks.

Last week gave us a glimpse into the effect of the 2024 election campaign on trade policy. In a major announcement, the Biden administration pressed the US Trade Representative (USTR) to triple certain Section 301 tariffs on steel and aluminum. It’s a lot to unpack. You can find the full text of the announcement here. […]

Foreign cold-rolled (CR) coil remains less expensive than domestic product, according to SMU’s latest check of the market.