Analysis

March 26, 2024

Final thoughts

Written by Michael Cowden

SMU’s sheet prices firmed up modestly this week, even as CME hot rolled (HR) futures declined. What gives?

My channel checks suggest that demand remains stable and buyers have returned to the market following new HR base prices announced by mills earlier this month.

I’m looking forward to seeing whether lead times, which have stabilized, will start extending. SMU will have more to share on that front when we release updated lead time figures on Thursday.

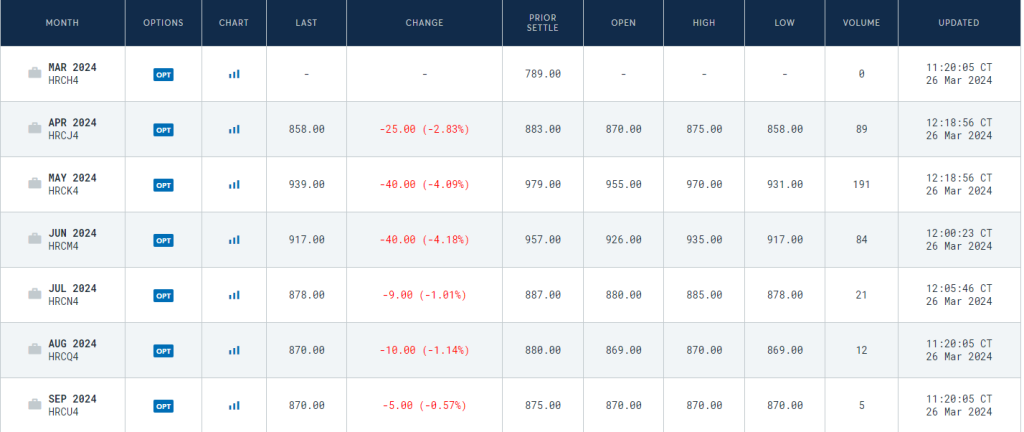

As for HR futures, what a reversal! As David Feldstein wrote last Thursday, bulls expected mill price increase announcements. And we briefly saw the May contract climb as high as ~$1,000 per short ton (st).

Here is what things looked like on Tuesday afternoon:

That’s a lot of red. Late last week, it would have been almost all green.

Mexico trade action rumors subside

There are two things that come to mind that might have caused this. For starters, we hadn’t (when this article was filed) seen a new round of price increases. I think it’s still possible we’ll see a price hike before Good Friday.

But I’ve also heard from some contacts that any increase might not come until after Easter. I’m not sure that rumored second increase is in doubt. While futures have backed off, they’re still well above current spot prices.

What’s missing now is whatever special sauce had CME HR futures in the high $900s/st. I can only guess as to that sauce’s main ingredients. And here’s my guess: There had been speculation last week that trade action against Mexico might be imminent. And that didn’t happen.

Recall that bi-partisan legislation has been introduced alleging that Mexico has “surged” steel exports to the US. And there have been calls in some corners for executive action by President Biden.

Mexico has of course threatened to retaliate. Perhaps we got used to shock trade policy moves via Twitter (ahem, X) under former President Trump. And perhaps what’s happening now is not trade policy via social media but instead what was the norm before Trump. Namely, trade negotiations, which could take time and which might not result in something as extreme as an immediate re-imposition of Section 232 tariffs.

Again, that’s just a guess. I’d be curious to know your thoughts.

Timing of a second increase and the HR-CR spread

I’ve questioned in recent columns and webinars whether the HR increase we saw in early March could look like one we saw in mid/late June of last year. Then, a rumored second increase before July 4 never materialized. And that June price hike succeeded mostly at “stopping the bleeding” rather than in raising prices.

I’m still in the camp that thinks we’ll see another round of sheet price increases, whether before or after the holidays. I could be wrong. But I also suspect that we’ll see continued gains on HR.

What I’m a little less sure of is where cold rolled (CR) and coated base prices go from here. Mills spelled out target prices for HR earlier this month. They didn’t spell out new base prices for tandem products.

Based on SMU’s current spot prices, which were updated Tuesday afternoon, the spread between HR and CR is $305/st. Some of you tell me you’re seeing that gap as wide as $350/st. That’s well above the $200/st post-pandemic spread we’ve gotten used to.

So what happens from here: Does HR rise to close that gap? Do CR/coated prices fall? Or are we seeing a “new normal” HR-CR spread of $300-350/st? Let me know what you think.

Baltimore bridge collapse and the next Community Chat

The collapse of the Francis Scott Key Bridge is a tragedy. If there is any upside, it’s that it happened in the middle of the night and not during rush hour – when the loss of life could have been much, much higher.

Given the nature of our publication, the next question might seem cold. But it’s one we are obliged to ask. What will the impact be on steel and ferrous scrap?

Media reports indicate that the main impacts could be on coal exports and on both imports and exports of passenger vehicles.

My preliminary channel checks indicate that there could be some impact on steel imports and scrap exports as well – but not to the same extent. For example, we will likely see force majeure declared and imports diverted to places like Philadelphia; Camden, N.J.; and Norfolk, Va. But the steel won’t be stuck at sea indefinitely.

Also, I’m told that clearing the shipping channel will be a huge priority – and that the project will be expedited. I don’t know how many weeks that might take.

We’ll get a more definitive take when we catch up with Anton Posner, CEO of Mercury Resources, for an SMU Community Chat on Wednesday, April 3 at 11 a.m. ET. It will be a timely chat and one worth your time. You can sign up here.

Thank you for your continued support of Steel Market Update.