Analysis

April 25, 2024

Final thoughts

Written by Michael Cowden

I’ve gotten some questions lately about whether the huge gap between domestic hot-rolled coil (HR) prices and those for cold-rolled (CR) and coated is sustainable.

I remember being asked similar questions about the wide spread between HR and plate that developed in early 2022. I thought at the time that there was no way that spread could hold.

Turned out, I was wrong. That was humbling. And so I’m not going to make any bold predictions this time.

Instead, I’m going to highlight some charts, data, and ideas to frame the issue. I’ll share my thoughts. And I invite you to share yours with me at michael@steelmarketupdate.com.

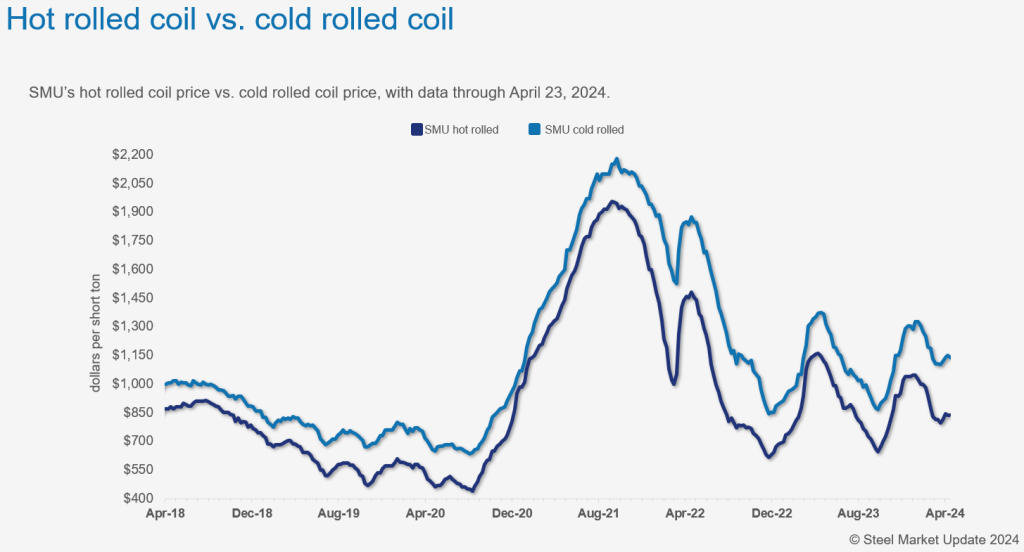

HR-CR spread inflation

Let’s start with the spread between domestic HR and CR:

It now stands at more than $300 per short ton (st). That’s 58% higher than the $200/st figure we saw a year ago. Talk about inflation!

A $200/st HR-CR/coated spread had been roughly the norm for the post-pandemic era. But it ballooned to approximately $300/st in January. It has stayed there since. And that’s despite sheet prices falling in the first two months of the year and, over the last two months, recovering – or at least stabilizing. (You can keep tabs here with SMU’s pricing tool.)

I know some of you never thought $200/st was sustainable. Why? Rewind to before the pandemic, and the HR-CR/coated spread was typically more like $100-150/st. Also, there were times during the snapback in demand following lockdowns that CR carried little premium over HR.

The question now: Is $300/st sustainable? If it is, why? And if it’s not, why not?

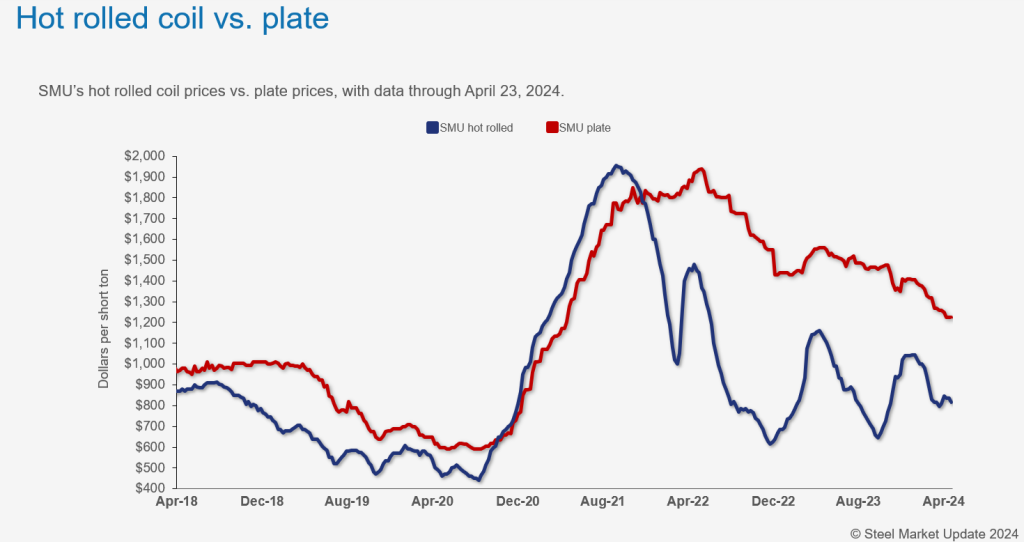

The HR-plate precedent

What I outlined above is roughly analogous to what we’ve seen in plate:

Before the pandemic, discrete plate typically carried a premium over HR. That makes sense. Plate is a value-added product. On a very basic level, it requires more time on the mill. Mills should be able to recoup more money for that time.

Pre-pandemic, discrete plate typically carried a $100-150/st premium over HR. That premium could sometimes disappear (or invert) when demand for HR was strong and/or when plate demand was weak. We saw that in late 2020 and throughout most of 2021 as HR demand surged.

But in early 2022, plate had re-established its premium. And by March of that year, it had inflated to an unprecedented (those words, again) $820/st premium over HR. That gap has slowly narrowed over time. It now stands at $410/st – half of what it was, but still well above any pre-pandemic norm.

In plate, at least, there are some obvious things you can point to at least partly explain things.

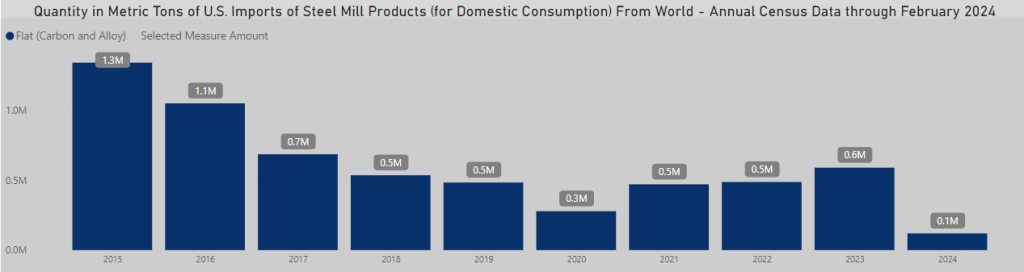

A trade case targeting plate from a dozen nations – unprecedented in scope – was launched in 2016. That case was mostly successful in 2017. And plate imports, as seen in the chart below, have never recovered to where they were:

The success of the case also made overseas plate sources unscathed by duties more important to the US market. And one of them – Azovstal, in Ukraine – was destroyed when it became a battlefield between Ukrainian and Russian troops in 2022.

Also, plate is more consolidated in the US than sheet. And there are only three major domestic plate producers – Cleveland-Cliffs, Nucor, and SSAB.

Yes, thicker coil might nibble away at discrete plate’s premium. And so too could competition from smaller players like JSW Steel USA, Algoma Steel, and Evraz North America. But that’s a topic for another column.

Can stronger demand offset increased supply?

Steel Dynamics Inc. (SDI) chairman and CEO Mark Millett in the company’s earnings call on Wednesday pointed to some good reasons why tandem products might carry a robust premium over HR. Namely, stronger demand – in particular from the solar industry.

It’s a solid point, and one I’ve heard from other contacts. Still, some folks I talk to remain highly skeptical that the spread will hold.

Some point to increased domestic coating capacity. Wolfe Research managing director Timna Tanners has estimated it to be ~4.34 million tons per year. (See slide 26 in the deck here from our Community Chat webinar in February.)

SDI, for example, is ramping up new coating lines right now at its mills in Terre Haute, Ind., and Sinton, Texas. So, too, is Big River in Osceola, Ark. Nucor has also announced additional coating capacity at its mill in Crawfordsville, Ind.

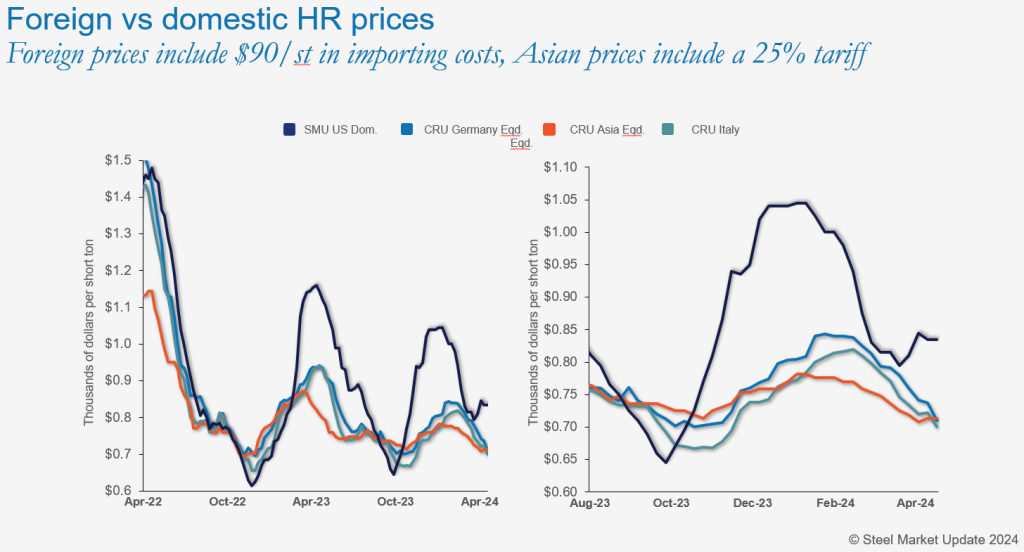

Others note increased competition from imports from East and Southeast Asia. Imports of tandem products from South Korea, Taiwan, and Vietnam have accounted for the bulk of US CR/coated imports in the first quarter. (That’s not including imports from Canada and Mexico, with which the US shares closely linked supply chains.)

In fact, the US imported slightly more than 500,000 metric tons (mt) of cold-rolled and coated product in March, according to preliminary figures from the US government. That marked the highest level for such imports since March 2022 (~570,000/mt).

April data is not available yet. Because the month is not complete. But you can see why March imports might have trended higher.

Here’s the spread between US HR prices and those abroad:

US prices, after falling throughout January and February, normalized with prices abroad once freight and duties were accounted for. But a gap has opened up again because US prices have been stable as those abroad slip.

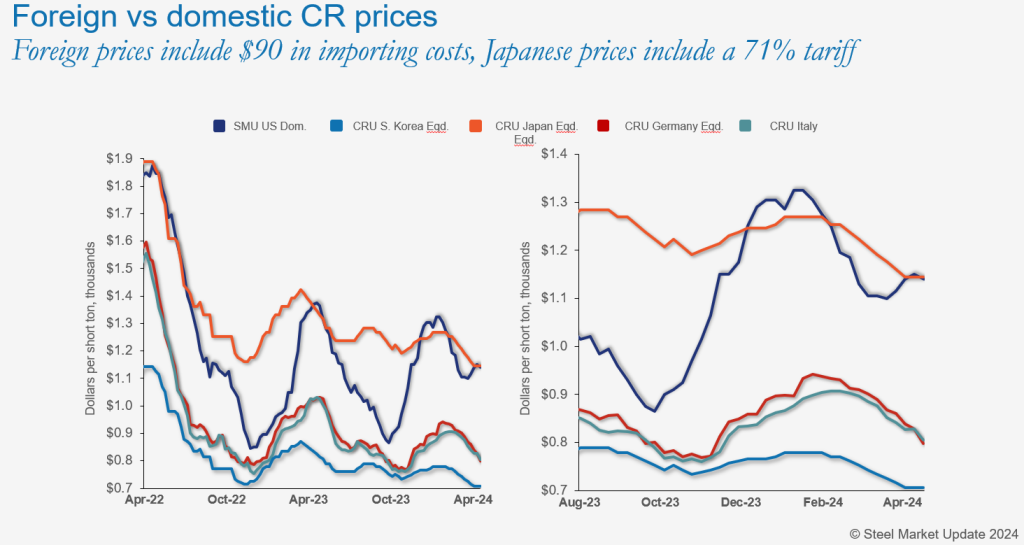

In CR (and by extension galv base), in contrast, US prices never reached parity with world prices – even after declines earlier this year:

What was the last CR/coated import offer you received? My guess is the price is compelling, even if the lead time is longer than you’d like.

My takeaway

On the face of it, it’s hard to see how increased domestic supply and increased imports don’t result in the spread between HR and CR/galv narrowing. I’d assume to something resembling a post-pandemic norm of ~$200/st.

That’s unless domestic demand for tandem products is somehow so strong that it offsets that increased supply. But maybe I’m missing some key variable? If you know what it might be, let me know!

SMU Community Chat

SMU is excited to host David Stickler, CEO of Hybar, for our next Community Chat on Wednesday, May 1, at 11 a.m. ET.

We’ll talk about the new mills Hybar is (or will be) building, what it means to be a “green” steelmaker, and how renewables, hydrogen, and traditional energy sources all have roles to play in the steel industry of the future.

And we’ll take your questions too. So sign up here, and bring some good ones to the Q&A on Wednesday!