Analysis

January 21, 2015

Final Thoughts

Written by John Packard

I was conversing with a consulting friend who reported to me that steel prices are taking a beating in Europe. He referenced hot rolled prices being offered out of Russia into Europe for 365 to 375 euros. He also reported that the sales of the Italian steel mill, ILVA would not succeed and the mill will be run by the government. Our source reported that just like the U.S. there is just too much capacity in Europe.

I got an email from Diann Scott, Senior Purchasing Manager for Kloeckner Metals and one of the attendees at our Steel 101 conference we just held in South Carolina, “…this was the best class/seminar I have ever attended on steel… I would recommend your seminar to anyone.”

Next Steel 101 workshop will be in Chicago with a tour of the NLMK Indiana steel mill.

Another thank you to our Nucor hosts at Nucor Berkeley. The tour was great and very helpful to those who were learning about the steel making and rolling process for the first time. I learned a lot from the metallurgist who took my group out into the mill. I was impressed with the equipment, knowledge and dedication of the Nucor employees.

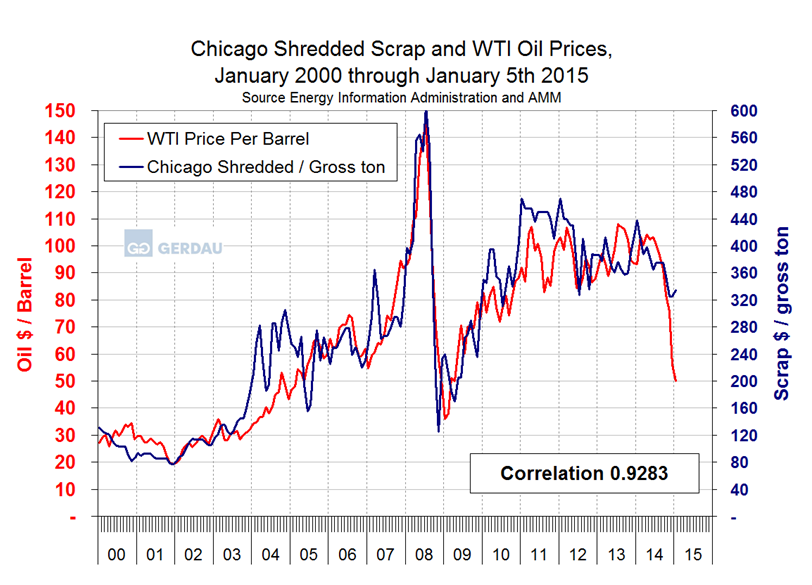

Peter Wright, one of our Steel 101 instructors, metallurgist and consultant to SMU and long products producer Gerdau, got a question from one of our former Steel 101 students regarding the price of scrap and its relationship to WTI oil pricing. The graph below gives you a long history of WTI and shredded scrap pricing and you can clearly see there is a very high correlation between the two. Based on Peter’s analysis scrap prices are about $100 per gross ton too high at this time…

By the way, for those of you who are not aware, the United Steel Workers union represents union workers at about 64 percent of the oil refining capacity in the United States. Their contract expires on February 1, 2015 and, according to the USW, the union is looking for double the pay raise they received in their last contract. The starting pay is $37.50 per hour. Keep an eye on this one.

The union workers should be aware of some of the statistics I saw this evening in the Armada Executive Intelligence Brief: U.S. crude oil inventories hit a 13 year high. Oil inventories grew by 10.1 million barrels over the past week. Gasoline inventories were up 0.6 million barrels, well above the upper limit of their historical average. Finally, production volumes were up 4.9 percent over one year ago.

Ray Culley and I continue to work diligently on a Senior Managers and Executive level workshop. We are developing the agenda and working on inviting instructors/speakers for what we think will be an excellent two-day program. One of the keys is we want this program to provide actionable information on a variety of topics. We will have more on this program soon.

I am also working hard on our 5th Steel Summit Conference which will be held in Atlanta on September 1 & 2, 2015. Block out the dates on your calendar.

As always your business is truly appreciated by all of us here at Steel Market Update.

John Packard, Publisher