Overseas

June 11, 2015

Analysis of World Export vs. Domestic Hot Rolled Coil Price Spread

Written by Brett Linton

One of the key items Steel Market Update watches is the spread between world hot rolled export pricing and the HRC spot price average here in the United States.

The following calculation is used by Steel Market Update in order to identify the spread between world hot rolled export prices as determined by SteelBenchmarker and domestic (US) hot rolled prices determined by SMU. Steel Market Update compares the world hot rolled export price to which dollars are added for freight, handling, trader margin, etc. The number generated is then compared to the spot (FOB Mill) domestic hot rolled price using the SMU Hot Rolled Index average for this week, with the result being the spread between domestic and world hot rolled coil prices. This is a ‘theoretical’ calculation as freight costs, trader margin and other costs can fluctuate.

This theoretical price spread analysis is based on our review of world export prices and the hot rolled steel price index produced by SMU earlier this week. As the spread narrows, the competitiveness of imported steel into the United States is reduced. If it widens then foreign steel becomes more attractive to U.S. flat rolled steel buyers.

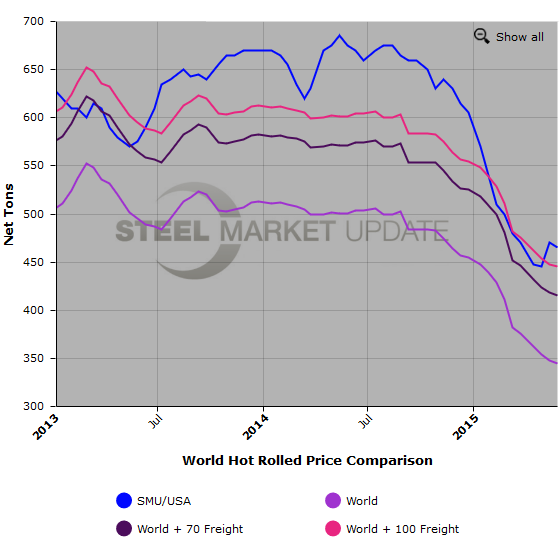

Over the past few months the trend has been for a narrowing of the spread between foreign and domestic steel. This should result in lower imports of foreign steel in the coming months. However, with the recent price announcements and increases in pricing the spread has started to widen which could pose a problem for the domestic mills should the spread get out of hand (widen too much).![]() The world export price for hot rolled bands is $347 per net ton ($383 per metric ton) FOB the port of export according to data released by SteelBenchmarker earlier this week. This is up $2 per ton from the previous release in late-May and down $1 per ton from one month ago.

The world export price for hot rolled bands is $347 per net ton ($383 per metric ton) FOB the port of export according to data released by SteelBenchmarker earlier this week. This is up $2 per ton from the previous release in late-May and down $1 per ton from one month ago.

SMU uses a minimum of $70 to as much as $100 per ton for freight, handling, and trader margin, which is then added to the export number in order to get the steel to ports in the United States. This puts our ‘theoretical’ selling price for hot rolled coil exported to the United States as ranging from $417 to $447 per ton CIF USA Port.

The latest Steel Market Update hot rolled price average is $460 per ton for domestic steel; this is down $5 from late-May and down $10 per ton from one month ago. The theoretical spread between the world HR export price and the SMU HR price is $13 to $43 per ton ($113 prior to import costs), down $7 per ton from our previous analysis and down $9 from one month ago.

The $13 to $43 spread is in line with what we have seen over the past few months. In mid-May the spread reached a four month high of $22 to $52 per ton ($122 prior to import costs). Earlier in the year we had lower spreads; in early February it was -$19 to $11 and was the lowest seen since late-May 2013. In 2014, the highest spread seen was in mid-May at $84 to $114 per ton ($184 prior to import costs). One year ago the spread was $66 to $96 per ton ($166 prior to import costs).

The above numbers are based on ‘theoretical’ calculations. This is where we believe prices and price offers should be if the SteelBenchmarker world export number is correct.

SMU did channel checks on foreign spot pricing this afternoon (Thursday). What we found is there were offers out there in the $420-$430 per ton range but many offers were pulled today due to the price announcements out of Nucor and ArcelorMittal. Just because the world export price has not fluctuated does not mean traders don’t recognize an opportunity for them to make more money.

As I spoke to one large HRC buyer who participates regularly in the foreign markets, he told us that the foreign mills are taking a look at what is happening in the North American markets and they will then come back into the market with new pricing.

Freight is an important part of the final determination on whether to import foreign steel or buy from a domestic mill supplier. Domestic prices are referenced as FOB the producing mill while foreign prices are FOB the Port (Houston, NOLA, Savannah, Los Angeles, Camden, etc.) or in the case mentioned above the Mexican border. Inland freight, from either a domestic mill or from the port, can dramatically impact the competitiveness of both domestic and foreign steel.

Below is a graph comparing world HR export prices against the SMU domestic HR average price. We also have included a comparison with freight and traders’ costs added which gives you a better indication of the true price spread. You will need to view the graph on our website to use it’s interactive features, you can do so by clicking here. If you need assistance with either logging in or navigating the website, please contact our office at 800-432-3475 or info@SteelMarketUpdate.com.