Market Data

May 12, 2019

Service Center Spot Pricing Collapsing

Written by John Packard

There is no more debate, service centers are moving off inventories at deeper discounts to their end customers than they did just a few weeks ago.

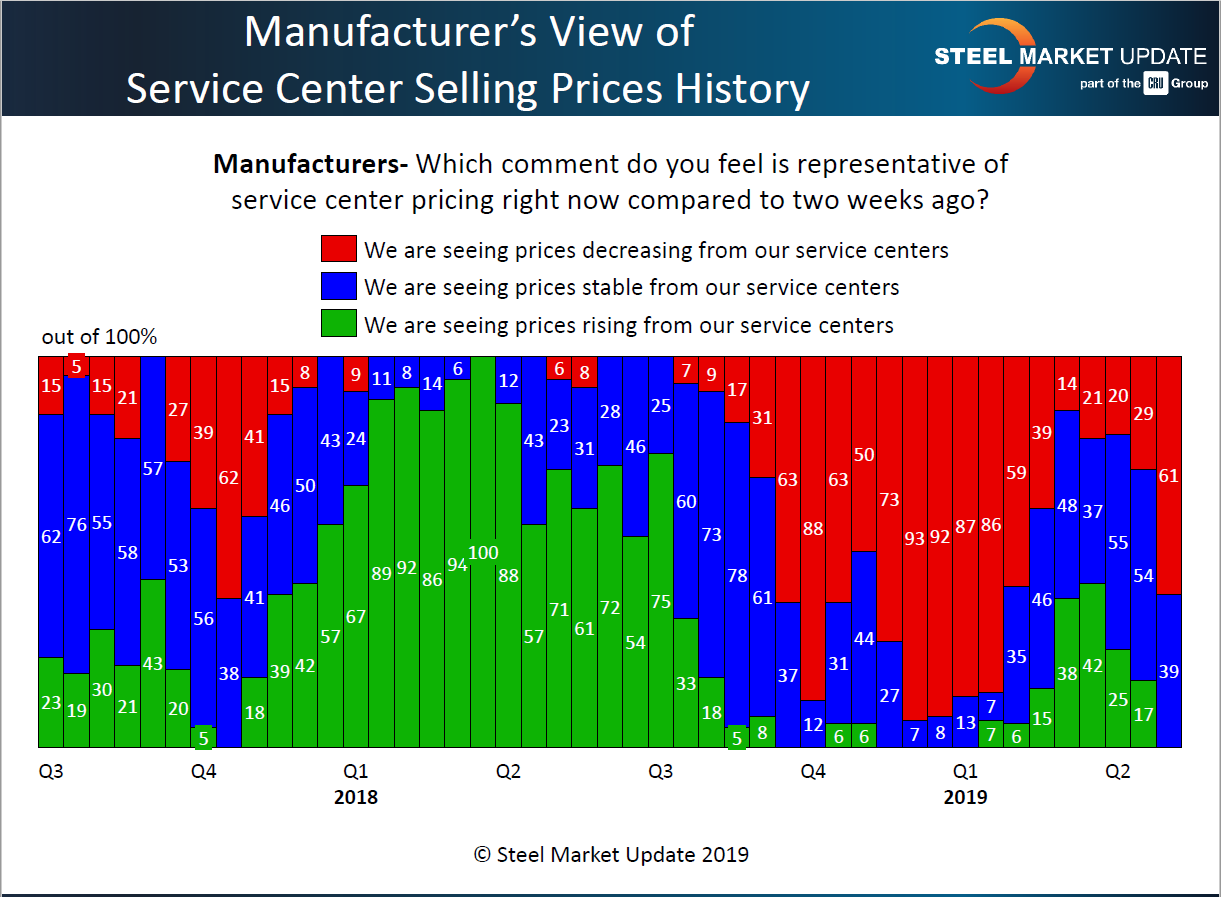

The lower spot prices to service center customers were captured during the Steel Market Update flat rolled and plate steel market trends analysis conducted this past week. As you can see in the graphic below, 61 percent of the manufacturing companies reported their steel distributors as decreasing spot prices compared to two weeks earlier. This is more than double the 29 percent who reported lower spot prices during our mid-April market trends analysis.

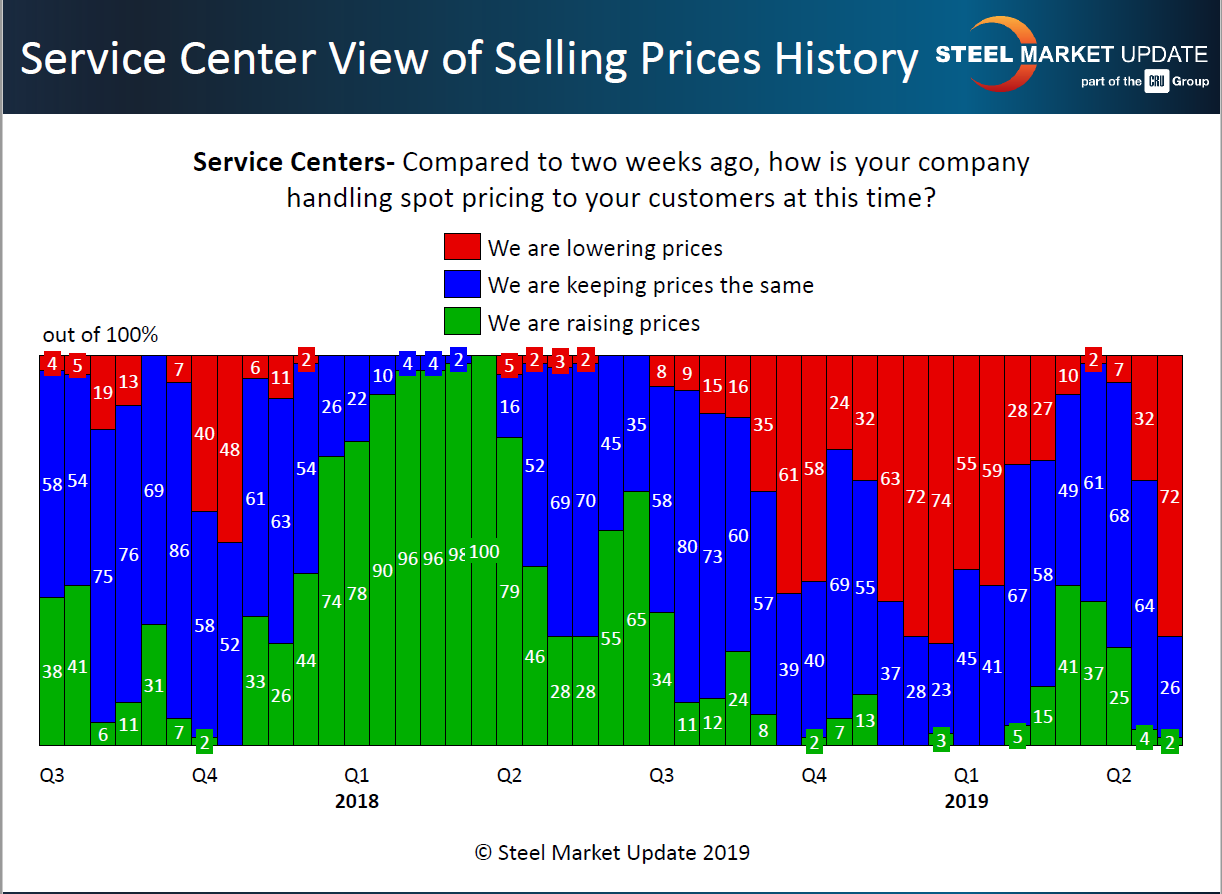

The service centers, who were questioned separately from the manufacturing companies shown above, reported their company as lowering spot prices by an even greater percentage than their customers. We had 72 percent of the steel distributors responding to our questionnaire reporting lower spot pricing compared to 32 percent during our mid-April survey and 7 percent at the beginning of the month of April. The 72 percent puts distributors at levels not seen since late November and into December 2018.

The history of our analysis of the service center spot pricing to their customers finds that when 75 percent of the steel distributors (or higher) are reporting declining spot prices to their end customers, the service centers reach a point SMU has termed “capitulation.” By this we mean sentiment becomes so negative at the distributors and the pain of consistently lower spot prices provides an opportunity of desire for the steel mills to announce price increases and to boost market sentiment.

We normally need to see a prolonged painful period where service centers are dropping spot prices and potentially squeezing margins before full capitulation is realized.

Steel Market Update recently attended the Metals Industry Boy Scout Dinner in Chicago and found a large number of service center executives complaining about weakening order books, contracts that were not being released as promised and lower spot pricing squeezing margins.

Steel mill base pricing has dropped from July 2018 highs of $915 per ton, based on the SMU HRC index, to $640 per ton this past week, a $275 negative move over the past 10 months. Domestic mill prices are now below those of foreign producers (partially due to the Section 232 influence on foreign pricing).

SMU is carefully watching the data we are gathering from manufacturing companies and service centers regarding spot pricing, inventory levels and demand as clues to how far flat rolled and plate prices can fall, and how soon we may see a rebound in pricing. Stay tuned. Our next market trends analysis will be conducted the week of May 20.

If you or your company are interested in becoming a data provider and working with SMU on our flat rolled and plate steel market trends analysis, please contact John@SteelMarketUpdate.com for details. Data providers receive access to a large PowerPoint presentation with the graphics shown above and much, much more prior to the information being shared with the public (and much of the data is never shared with the public other than our Premium level members).