Analysis

July 14, 2026

SMU Survey: Mills benefit from tariffs as buyers wait for supply

Written by Laura Miller

SMU’s July 10 Flat-Rolled Steel Survey results paint a picture of a steel market being squeezed from every direction. Tariffs are holding prices up and giving mills a clear advantage, while manufacturers and traders say the policy is pushing their costs higher. The Iran conflict is still disrupting freight, though its impact is slowly easing. Even so, buyers say the real pressure now is simple availability. Spot tons are scarce, imports are stalled, and many expect no real relief until late summer.

Uneven tariff impact

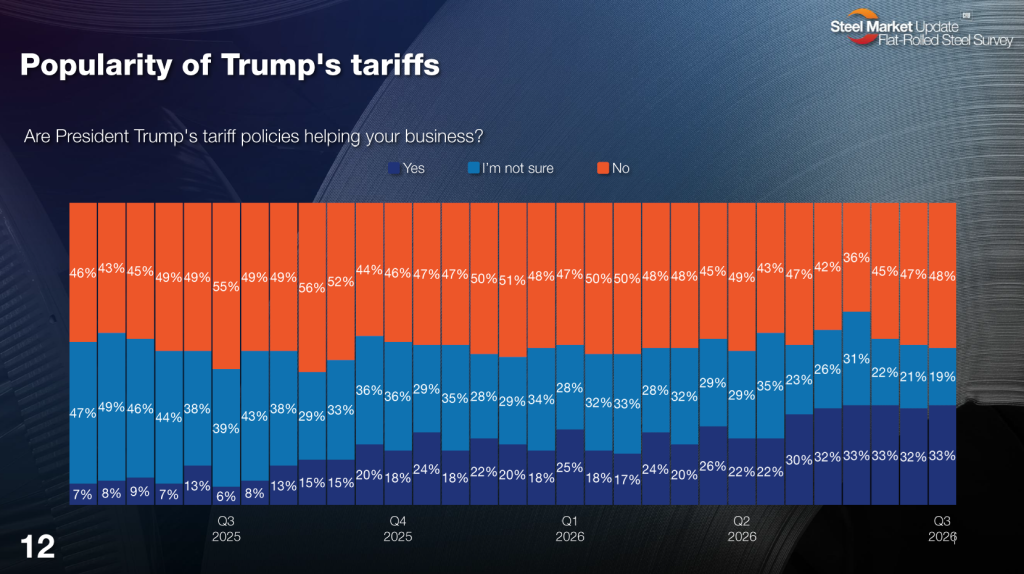

Opinions on tariffs are becoming clearer. Thirty-three percent of surveyed respondents now say the tariff policies are helping their businesses (Slide 12 below). That is tied for the highest share since we started asking the question in Q2’25. The number of unsure respondents is at its lowest point (19%). Still, nearly half (48%) say tariffs are not helping them at all.

Mills and service centers are seeing the most relief. Several say tariffs are keeping the market firm. One service center told us tariffs are “keeping prices insulated and moving higher.” Another said their inventory value has appreciated thanks to the tariffs. Others described a tighter market where “tariffs are making markets tight, and prices climb,” and “higher prices are trickling down from the mills to us.”

Some mills also see structural benefits, saying the policy is shifting buying patterns. One mill respondent noted more “onshoring of demand and localized purchases for USA content.” Another said they see “fewer imports and more reshoring.”

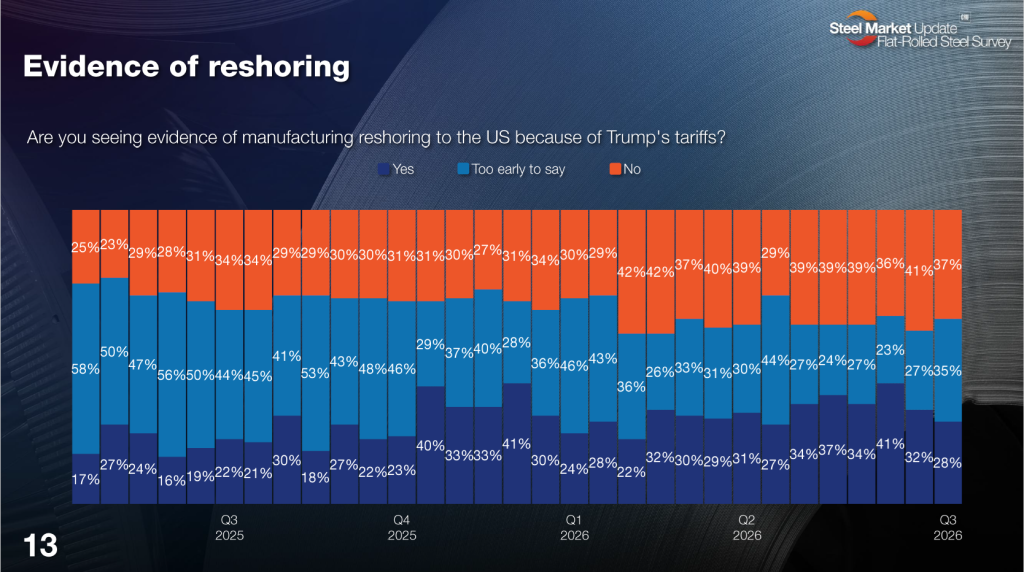

Still, only 28% of surveyed respondents said they are seeing evidence of reshoring, the lowest percentage since early this year (Slide 13). As one service center put it, “Definitely some, but the permanence and overall shakeout is not yet clear.” Another said, “Work is being done to reshore. While it will take years, the wheels are in motion.”

Manufacturers and traders paint a very different picture of tariffs. Many say they have driven up costs, squeezed margins, and limited supply options. Even a mill respondent noted that Section 232 tariffs have hurt their exports. A manufacturer said domestic mills “have full control on pricing,” while a trading company observed that tariffs are “hurting manufacturers and end users, only helping mills.” Another respondent went further, calling mill profits “sickening” and saying domestic producers keep prices “equal or above the imports.”

Impact of Iran conflict

The Iran conflict is also still affecting business, but the impact appears to be easing somewhat.

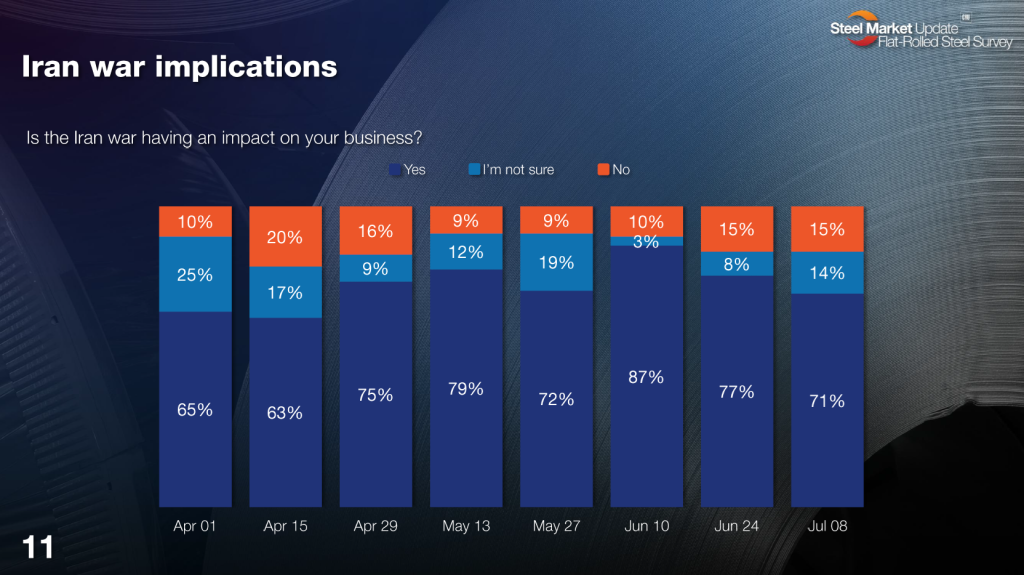

Seventy-one percent of respondents said the war is affecting them, but this is the lowest level since mid-April (Slide 11). Shipping problems and elevated freight costs remain the biggest complaints. One trading company said, “My offshore suppliers cannot ship.” A service center said simply, “Stopped imports.” A supplier said shipping costs are now restricting their product’s reach. Some manufacturers say consumer spending is weakening. One said the conflict “has given people another reason to panic/not spend money,” adding that gas prices are making things worse.

A few mills see an upside. One said lower import activity has “reduced competitive pressure in our market.” Mirroring the tariff effect, less foreign steel means tighter supply and stronger mill margins.

Relief coming?

Multiple comments throughout the survey highlighted the tight market, but when do buyers expect relief?

One service center noted they are reducing their inventory, but “not by choice… need more steel.” Another service center, commenting on lead times, noted they’re normal for contract tons, but spot tons “do not exist.” There is “very little available,” commented another.

Still another service center respondent said mill negotiability rates on hot rolled are “hard to tell” because there are “no real offers out there.” They “believe it will be August’s end before we hear of any availability.” Another buyer thinks mills will become more negotiable on prices starting in early August.

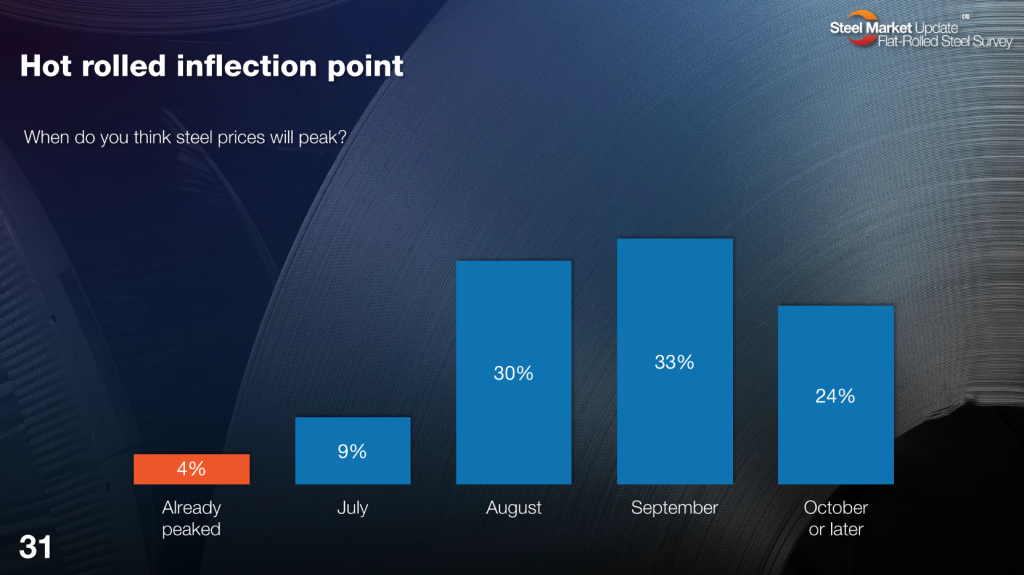

August is also when 30% of respondents anticipate hot-rolled steel prices to peak (Slide 31). A third of respondents think they won’t peak until September. Still others (24%) don’t see any price relief until October or later.

Premium subscribers can access the full survey results here.