Market Data

June 23, 2019

Service Center Spot Pricing: Only a Matter of Time Now…

Written by John Packard

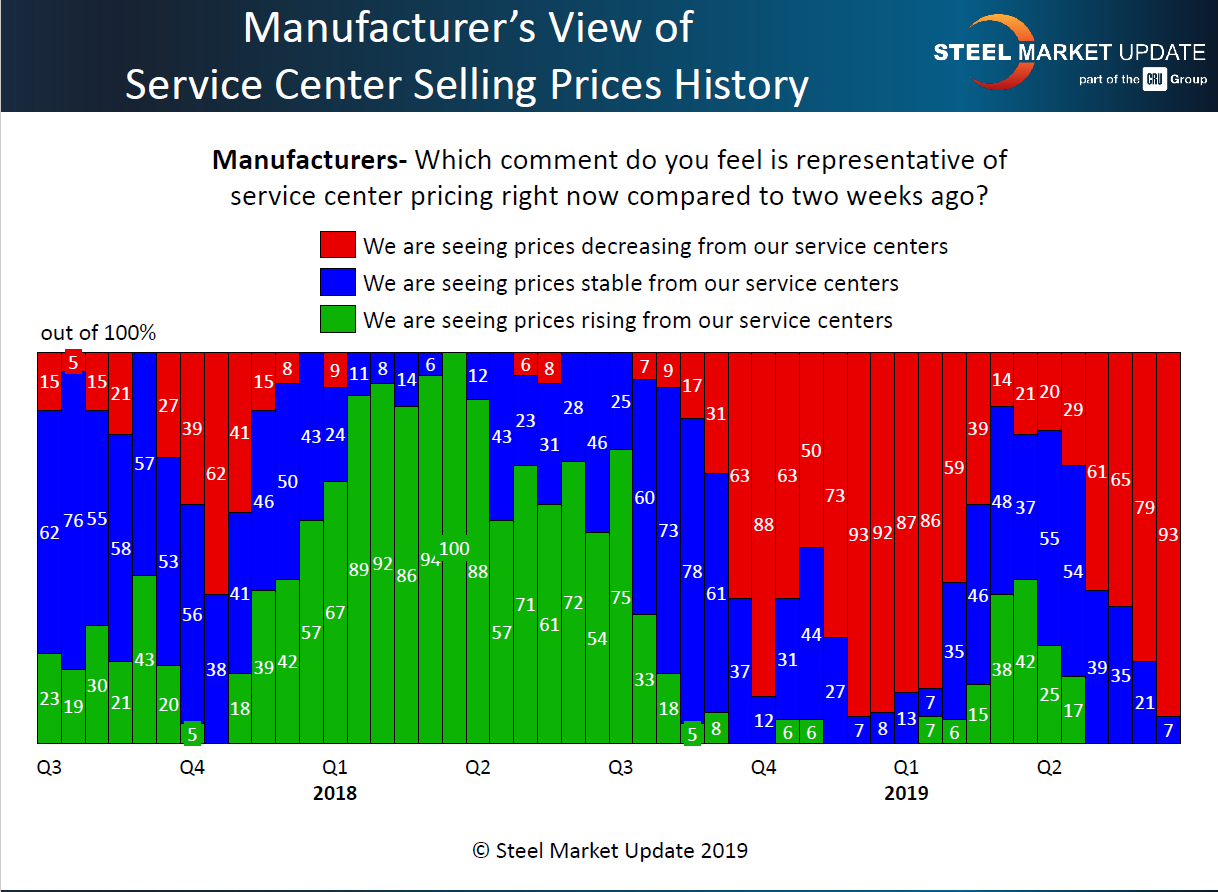

One thing is certain in this crazy steel market, service centers are taking their spot prices lower and lower as each week passes. Manufacturing companies are almost unanimous in their view that flat rolled steel distributors are decreasing their spot offers. We saw 93 percent of the manufacturing companies responding to last week’s SMU flat rolled and plate steel market trends questionnaire reporting service center spot prices as in decline compared to two weeks ago (see below). This represents an increase of 14 percentage points compared to the beginning of the month of June, and is 28 percentage points greater than one month ago.

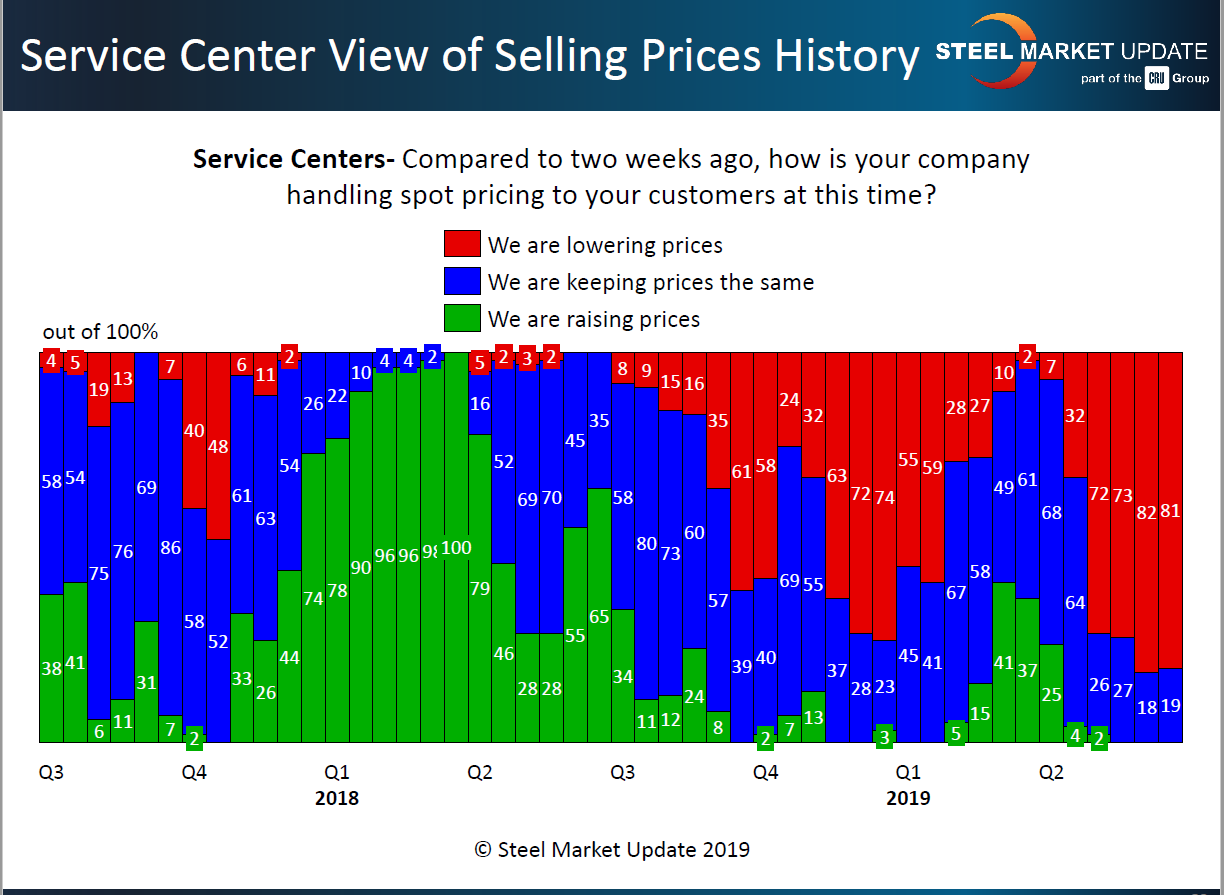

Eighty-one percent of the service centers agreed with their manufacturing customers as they too reported spot prices as dropping over the past two weeks. This puts the distributors within the “capitulation” window that Steel Market Update describes as being when 75 percent or more of the distributors are reporting spot prices as dropping. In a “normal” market that would be a clear sign for the domestic steel mills to raise prices, as the service centers would be inclined to support the increases as a way of holding the value of their inventories and potentially taking the pressure off of stressed margins.

As you all know, we are far from a normal market due to the interference by the U.S. government, which has chosen to institute Section 232 tariffs on steel to the tune of 25 percent. This has artificially increased foreign steel prices and played havoc with the psyche of the steel buyers. After flat rolled spot prices peaked almost one year ago, we have seen a constant drift lower as $900 per ton hot rolled is now 40 percent off the highs. Last week’s HRC average was $550 per ton, however the low end of our range was close to $500 per ton. There are signs there may be HRC offers out there below $500 per ton.

So, even though service centers are dumping high-priced inventories they can replace those tons at significant discounts. The real squeeze, the real total capitulation, will come when distributors no longer feel they can buy cheaper tons next week than what is being offered today.

For that to happen, the domestic steel mills will need to announce price increases and follow through on collecting those increases (they were not able to in late January/early February 2019 and we had a “dead-cat bounce” before prices continued their slide). The market believes there is pent-up demand among end-users, which would be released if buyers thought prices were moving higher from here. This would then move lead times out, which is a clear sign of stronger order books at the mills. Stronger order books mean tighter negotiations and the cycle begins anew.