Prices

January 30, 2020

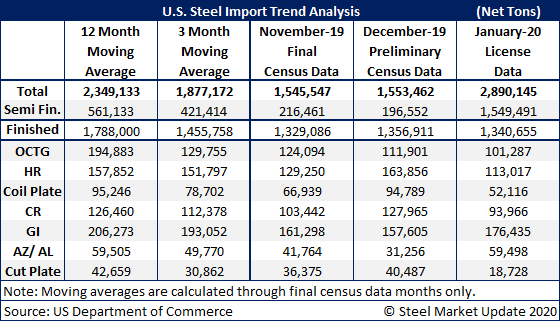

Steel Import Trends in December and January

Written by Brett Linton

Finished steel imports continued to trend downwards into January, slipping over 200,000 tons from our last update and resting at 1.34 million tons. This is in line with the final November and preliminary December data, but down considerably compared to the 3-month and 12-month moving averages.

Based on the latest Commerce Department import license data, total steel imports in December are expected to be in the 1.55 million ton range when the numbers are final, quite a fall from the 2.34 million tons the DOC reported just last week. This difference is likely due to imports reaching their annual quota limits in December.

January semi-finished licenses increased to 1.55 million tons, but will most likely be offset by much smaller totals in February and March as the quarterly quota limits average out. Thus the current total of January finished and semi-finished licenses from Commerce, at nearly 2.9 million tons, is artificially inflated and will correct in the coming months.

Steel Market Update has not projected any of the import data in the table below, as tariffs and import quotas skew any forecasts.