Analysis

March 6, 2020

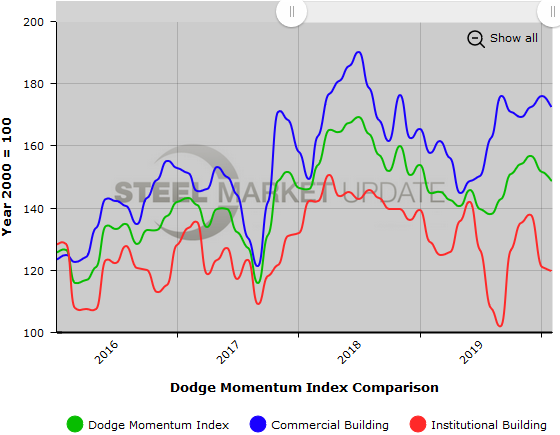

Dodge Momentum Index Dips in February

Written by Sandy Williams

Nonresidential construction planning slowed in February, according to the latest report from Dodge Data & Analytics. The Dodge Momentum Index moved 1.8 percent lower to 148.7 from the revised January reading of 151.4. The Momentum Index is a monthly measure of initial reports for nonresidential building projects in planning, which have been shown to lead construction spending for nonresidential buildings by a full year.

February’s decline occurred in both components of the Index, with the commercial component falling 2.1 percent and the institutional component declining by 1.2 percent.

While the overall Momentum Index has declined for two consecutive months, it remains 11 percent higher on a year-over-year basis. The commercial component is 20 percent higher than a year ago, while the institutional component is 2 percent lower. This continues to suggest that construction activity should remain near its recent highs in 2020, said Dodge.

In February, six projects valued at $100 million or more entered the planning stage.

Below is a graph showing the history of the Dodge Momentum Index. You will need to view the graph on our website to use its interactive features; you can do so by clicking here. If you need assistance logging in to or navigating the website, please contact us at info@SteelMarketUpdate.com.