Analysis

April 16, 2026

Final Thoughts: Inventories are lean like it's 2021

Written by Michael Cowden

The spot market squeeze that’s characterized the sheet market lately doesn’t show any signs of easing – at least not this week.

Lead times remain extended. Mills remain unwilling to negotiate lower spot prices. And why would they?

Sheet inventories leanest since 2021

I say that because here’s another key data point (as our premium subscribers already know): Service centers held only 2.24 months of supply (49.3 days of supply) of sheet products in March, according to our latest figures. If you check our archives, you’ll see that’s the lowest sheet inventories we’ve seen since June 2021 – which was hardly a bad year for steel.

(Editor’s note: Service center inventories are a great reason to consider upgrading from executive to premium. Give us a shout at smu@crugroup.com if you’d like to learn more.)

Meanwhile, HR lead times average six to seven weeks. (That’s not a 6-7 joke. But, if you have kids, feel free to insert one.) CR and coated lead times average about eight weeks. In other words, there is not much wiggle room between inventories and lead times.

Lead times are a fast-moving target

And the lead time/inventory gap might be getting tighter. At certain mills, lead times have extended by a week since we closed our most recent steel market survey. And at others, lead times are significantly longer than the averages we post.

One mill, for example, recently published HR lead times stretching into late June/early July. (We hear they’re struggling to come back from production issues earlier in the year.) Meanwhile, some of you continue to tell me you can’t get spot tons at all – even from mills that might have shorter lead times for contract tons.

With lead times, as with prices, it’s been a slow upward grind, not the kind of spike we’ve seen in the past stemming from outside shocks (e.g., the war in Ukraine) or supply-demand dynamics (e.g., mills slow to restart after Covid).

In fact, we haven’t seen HR lead times as long as they are now since Nov-Dec 2023, according to our lead time archives. The surge then came ahead of the resolution of a United Auto Workers (UAW) strike. To be clear, lead times now are nowhere near as long as they were in June 2021. They were 10-11 weeks on average then! And sheet inventories in June 2021 were even leaner (2.16 months).

Has better demand entered the chat?

I wonder if we should consider adding improved demand to the list of things keeping supply tight? Or, to put it a different way, is this still a “demandless” recovery, or has better demand entered the chat?

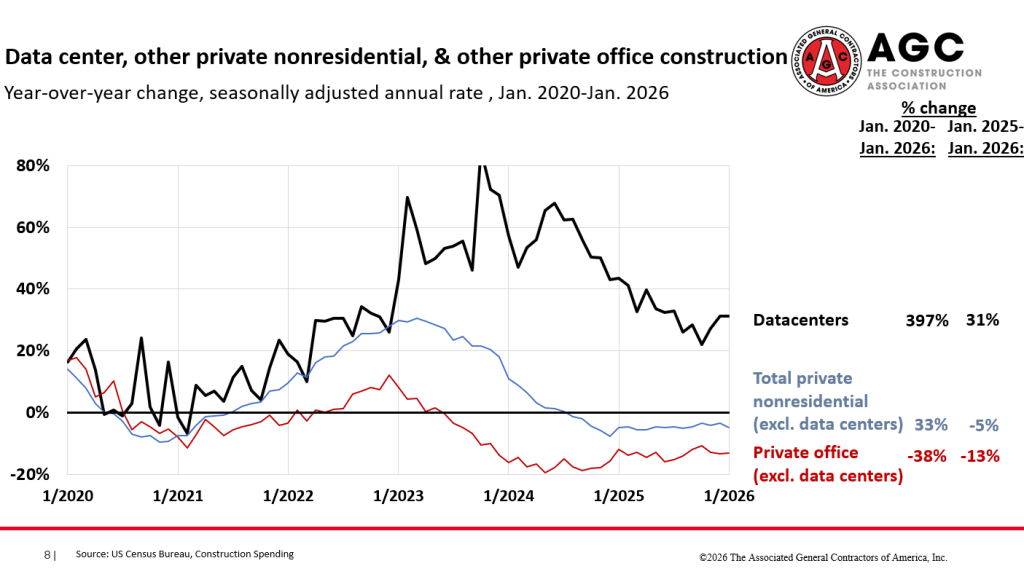

I ask that, in part, because the Federal Reserve’s Beige Book noted stronger manufacturing demand, driven in part by data center construction. It echoed what Ken Simonson, chief economist for the Associated General Contractors of America (AGC), said during his Community Chat on Wednesday.

SMU and AMU subscribers can listen to a replay of the Chat here. (Our apologies for some fumbling with the slides at the beginning of Ken’s presentation.) If you want to cut straight to it, look at this slide:

What I found particularly interesting was this: Ken acknowledged data centers face a long list of headwinds—increased regulation, intense local opposition in some areas, difficulty securing enough power, and a lack of skilled workers. But he doesn’t think that will change underlying demand for the centers. It might just extend the buildout, which is arguably good for steel demand, given how steel-intensive data centers are. (As I’ve noted before, Nucor has a helpful graphic on the matter.)

Not everyone agrees

There are big differences of opinion out there. Some of you think inflation – whether it’s higher steel or fuel prices, or the impact on consumers – will lead to demand destruction. It’s a valid concern.

Others remind me HR prices got to nearly $2,000/st in 2021 despite fretting about demand destruction from the moment they crossed $1,000/st. That camp might point out it wasn’t high prices that caused steel prices to fall in the fall of 2021. It was the simple fact mills finally caught up to demand in the back half of the year. And, so, in their eyes, there’s nothing to stop prices from rising as long as demand remains solid and supply tight. That’s a valid point, too.

Mills talking down the market?

Here’s another thing I’ve been wondering. Typically, mills tend to talk up prices and lead times. Buyers tend to talk them down. (Everyone is their own spin machine.) But what we’re seeing now, it seems, is producers in some instances talking down prices and lead times.

Nucor, for example, says publicly that its HR lead times are 3-5 weeks. Maybe that’s an average? Because published HR lead times at some of its facilities are significantly longer than that.

It’s a similar dynamic when it comes to prices. Most mills have been following Nucor in nudging prices up by $5-10/st from one week to the next. It’s been a successful strategy to date. And it’s avoided the kinds of price spikes that have attracted a surge of imports in past cycles. (Related to that, steel buyers have gotten good at navigating such price spikes. But a slow rise in prices, one spanning more than six months, has arguably proven trickier to steer through.)

My point is this: SMU’s lead times are well beyond some published mill lead times. (Despite that, we get flak now and then for our lead times being too short.) Lead times tend to lead prices. So, could we see pricing indices start to outpace prices published by domestic mills?

Let us know your thoughts at smu@crugroup.com!

SMU-CRU VIP Industry Briefing

Do you want to dive into some of the topics above in more detail? Then join me at the SMU-CRU Briefing – “Scouting the Market So You Don’t Have To” – on April 23 at the Swissotel in Chicago.

The event will start at 8:30 a.m. and wrap up at 12:30 p.m. So we’ll leave you plenty of time to meet up with colleagues for a drink or three before the Metals Industry Scout Dinner in the evening.

Joining me will be CRU Research Principal Josh Spoores, Flack Global Metals Founder and CEO Jeremy Flack, Browns Gibbons Lang Managing Director Vince Pappalardo, and BMO Managing Director Andrew Pappas.

You can find out more and register here.