Analysis

March 23, 2020

Final Thoughts

Written by John Packard

There is no way to plan for this…

The stock market was up 2,100+ points today.

I don’t know anyone personally who has contracted the COVID-19 virus.

My kids are safe, albeit without incomes for the time being.

Gas prices are below $2.00 and headed lower.

The weather in Florida is perfect, and technically I am on vacation.

Why don’t I feel better about life?

Most of Southern Florida is in a “stay at home” mode. All beach access is restricted. The parks are closed. Restaurants are take-out only. The bars are closed.

It is worse in other states where all “non-essential” businesses have been ordered closed.

Buyers and sellers of steel are considering what their options are going to be in the coming weeks.

I received a call late last week from the top executive of a service center and we discussed the hard options facing his company and their employees. Right now, business is very good. Yet his sentiment was quite negative for the short-term future.

The head of purchasing for a large service center group told SMU that with scrap expected to be down dramatically in April (possibly even $100/gross ton) and with the impact of the restrictions on business due to COVID-19, the expectation is for steel prices to be lower. “The reality is that with demand so suspect, no one is going to want to buy, regardless of the pricing, unless they really need it,” he said.

Last week we reported the largest one-week drop (-45 points) in the SMU Steel Buyers Sentiment Index, declining to +13 points which is barely within the optimistic portion of the index. I got a comment from someone who was surprised that our index was not in the pessimistic range. Even with of all the negatives that are out there, the steel industry is nowhere near where it was in 2009 when our index reached -85. OEMs and service centers are still reporting good business conditions and a relatively healthy backlog. This is not a pessimistic industry and our index reflects that. I expect in the coming weeks as the virus spreads and more businesses are affected, we will see negative numbers in our index.

Here is what one service center executive said when speaking about business and his company on the other side of the COVID-19 emergency: “We are optimistic that we will be whole, yes, although we will need to be creative and smart in order to get there. We need mills to be stable and run effectively. We need everyone to be smart and manage their business for profitability as well as cash generation and keep a long-term perspective to do what’s best for customers and the industry as a whole. Our industry will be successful, but it will take everyone doing the right thing – for customers, suppliers, distribution companies, mills.”

We are still very early in this fight against COVID-19. My worry is that Americans will become impatient with the amount of time it will take to get this virus behind us. I also worry about moves the government (local, state and federal) might make, or not make, that will create a bigger problem than might otherwise have been the case had things been handled differently.

Here in Florida, the governor has an executive order calling for anyone from high infection areas (specifically New York and New Jersey) arriving by plane into the state to quarantine themselves for 14 days upon arrival. There are no restrictions on car, bus or train travel….

I don’t quite understand the logic (or how the order could ever be enforced).

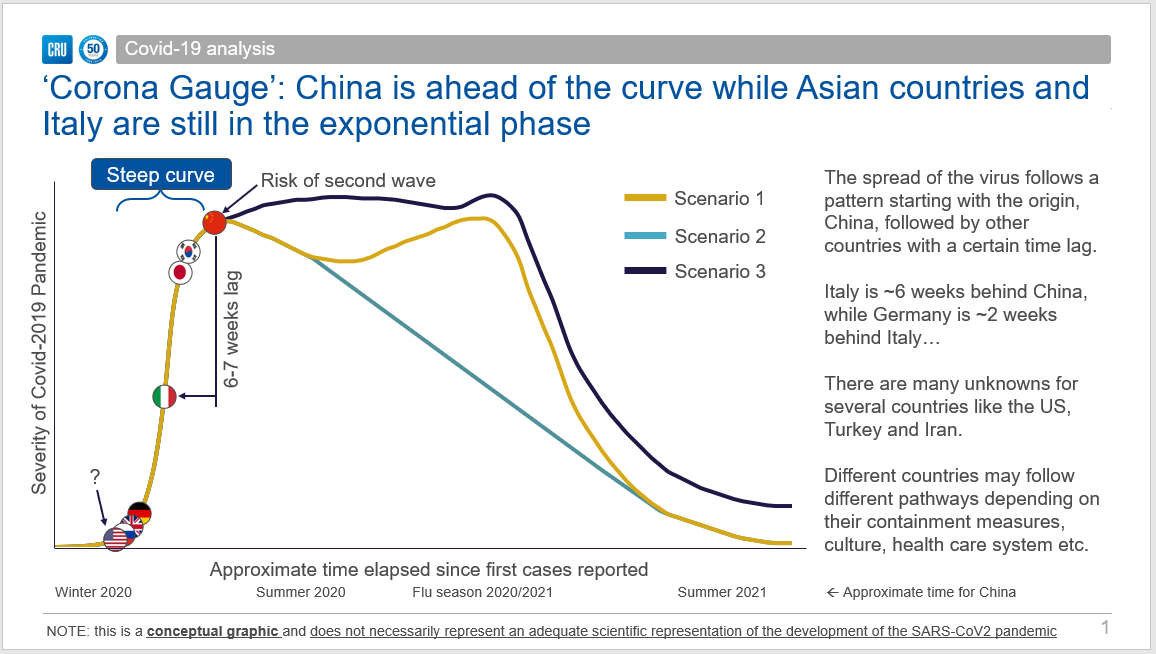

Earlier this week I listened to steel and commodity analysts with CRU discuss what was happening in various regions around the world. What struck me was a graphic that was used during the discussion. You may have seen graphics like the one below. The graph is not meant to specifically forecast the number of cases, it is only meant to represent the U.S. as being very early in the process with the ultimate peak still weeks away, and the number of cases unknown.

Today, the World Health Organization said the United States will overtake Italy as the focus of the global pandemic in the coming weeks.

Even so, Americans are optimistic and productive people and we will come out of this, and business will return to whatever the “new normal” is going to be.

Perhaps what is important right now is family and friends and what you can do as an individual to ensure their health and well-being.

I appreciate any comments you might have. You can reach out to me at John@SteelMarketUpdate.com and I will do my best to respond to you ASAP.

I wish everyone good health.

As always, your business is truly appreciated by all of us here at Steel Market Update.

John Packard, President & CEO