Product

March 25, 2020

Flat Rolled Steel Prices Down But No Collapse

Written by Brett Linton

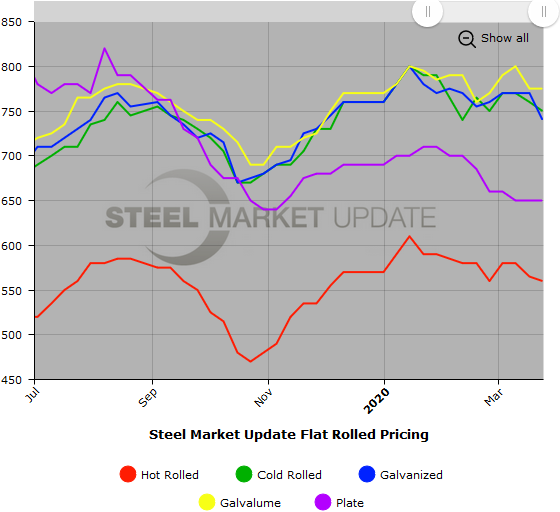

Steel prices continue to weaken due to the coronavirus’ effect on demand, but have not collapsed as many fear. Galvanized steel saw the biggest decline in the past week, with smaller adjustments for hot rolled and cold rolled products.

Here is how we see prices this week:

Hot Rolled Coil: SMU price range is $540-$580 per ton ($27.00-$29.00/cwt) with an average of $560 per ton ($28.00/cwt) FOB mill, east of the Rockies. The lower end of our range remained unchanged compared to one week ago, while the upper end declined $10 per ton. Our overall average is down $5 per ton over last week. Our price momentum on hot rolled steel is now Neutral until the market establishes a clear direction.

Hot Rolled Lead Times: 3-8 weeks

Cold Rolled Coil: SMU price range is $740-$760 per ton ($37.00-$38.00/cwt) with an average of $750 per ton ($37.50/cwt) FOB mill, east of the Rockies. The lower end of our range increased $10 per ton compared to last week, while the upper end declined $30. Our overall average is down $10 per ton over one week ago. Our price momentum on cold rolled steel is now Neutral until the market establishes a clear direction.

Cold Rolled Lead Times: 4-8 weeks

Galvanized Coil: SMU base price range is $35.00-$39.00/cwt ($700-$780 per ton) with an average of $37.00/cwt ($740 per ton) FOB mill, east of the Rockies. The lower end of our range declined $50 per ton to one week ago, while the upper end declined $10. Our overall average is down $30 per ton over last week. Our price momentum on galvanized steel is now Neutral until the market establishes a clear direction.

Galvanized .060” G90 Benchmark: SMU price range is $769-$849 per net ton with an average of $809 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 6-8 weeks

ARTICLE CONTINUES BELOW

{loadposition reserved_message}

Galvalume Coil: SMU base price range is $38.00-$39.50/cwt ($760-$790 per ton) with an average of $38.75/cwt ($775 per ton) FOB mill, east of the Rockies. The lower end of our range increased $10 per ton compared to last week, while the upper end declined $10. Our overall average is unchanged over one week ago. Our price momentum on Galvalume steel is now Neutral until the market establishes a clear direction.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU price range is $1,051-$1,081 per net ton with an average of $1,066 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 6-8 weeks

Plate: SMU price range is $640-$660 per ton ($32.00-$33.00/cwt) with an average of $650 per ton ($32.50/cwt) FOB delivered to the customer’s facility. The lower end of our range increased $20 per ton compared to one week ago, while the upper end declined $20. Our overall average is unchanged over last week. Our price momentum on plate steel is Lower, meaning we expect prices to decline over the next 30 days.

Plate Lead Times: 4-5 weeks

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume and plate price history. This data is available here on our website with our interactive pricing tool. Note that plate prices are not yet available on our website, but we are in the process of adding that dataset. If you need help navigating the website or need to know your login information, contact us at info@SteelMarketUpdate.com or 800-432-3475.