Market Data

October 3, 2021

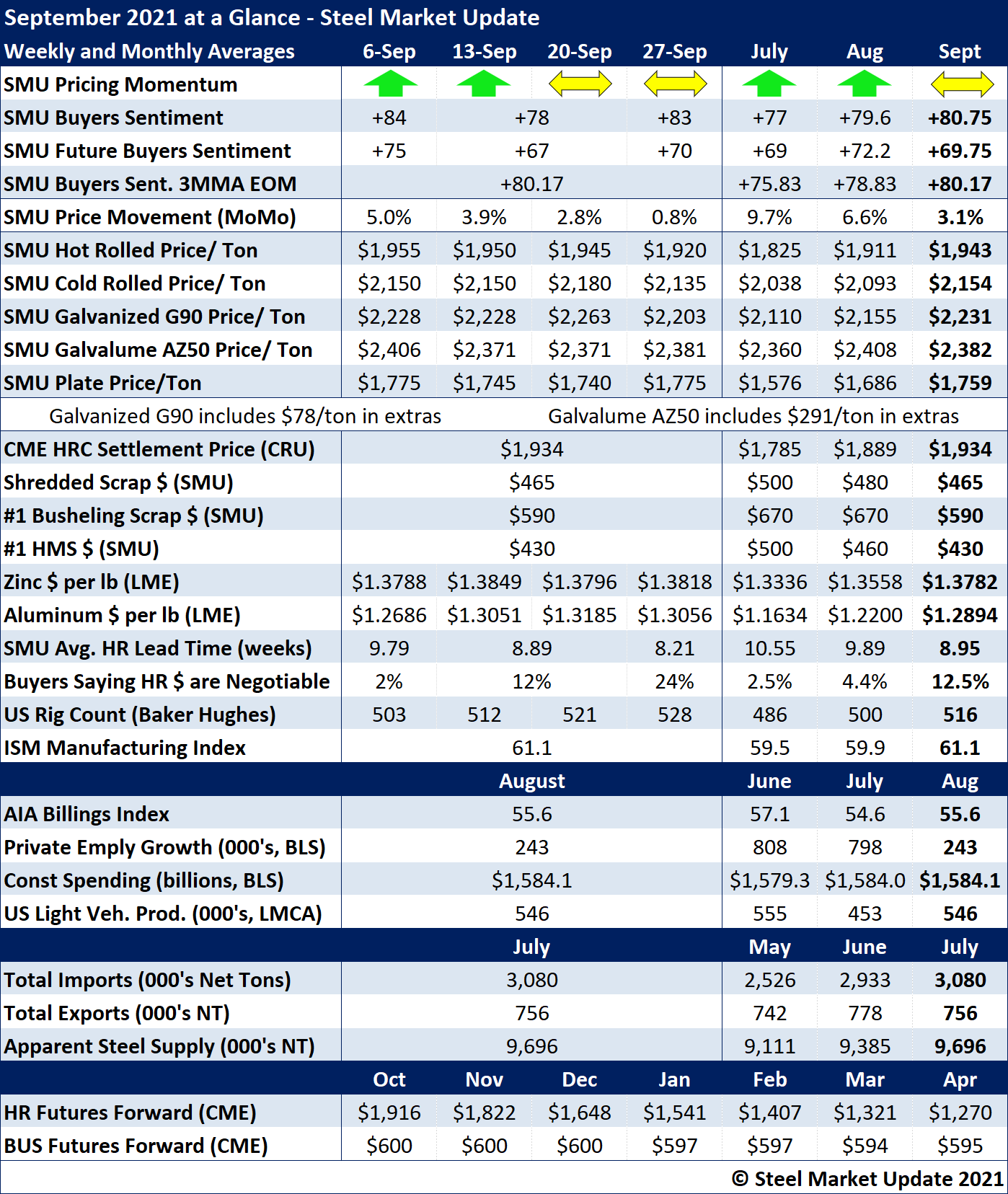

SMU's September At-a-Glance

Written by Brett Linton

Steel prices gradually declined through the month of September, following one full year of increasing prices. Hot rolled steel prices decreased $35 per ton ($1.75 per cwt) throughout the month, with the SMU index averaging $1,920 per ton ($96.00 per cwt) as of last Tuesday. The SMU Price Momentum Indicator was adjusted to neutral the week of Sept. 20 for all products, following a record one-year streak pointing higher. Our price momentum will remain Neutral until the market establishes a clear direction.

September scrap prices were flat to down $15-80 per ton from August, falling from the historically high levels seen in the summer months. Click here to view and compare prices within our interactive pricing tool.

Zinc spot prices reached a new multi-year high, rising to $1.4036 per pound on Sept. 10. Prices have since declined to $1.3631 as of Oct. 1. Aluminum spot prices continued to soar throughout the month, reaching another record high of $1.3386 per pound as of Sept. 23. Excluding the occasional 2-5 day surges seen in aluminum spot prices, this is the highest daily price seen in over 10 years. Aluminum prices ended the month at $1.2973 as of Oct. 1.

The SMU Buyers Sentiment Index remained highly optimistic throughout September, ending the month at +83. Recall that the early-September reading of +84 was the highest in our recorded history. Viewed as a three-month moving average, buyer sentiment also reached a new record high of +80.17.

Hot rolled lead times shrunk by nearly 1.6 weeks throughout September, ending the month at 8.21 weeks, the lowest level seen since February of this year. The percentage of buyers reporting mills willing to negotiate on HR prices has started to increase, rising from 2% in early September up to 24% as of last week.

Key indicators of steel demand continue to remain positive, as they have for months. The ISM Manufacturing Index indicated further economic expansion for the 15th consecutive month, and the AIA Billings Index indicates construction activity has recovered for the eighth month in a row. In the energy sector, the active drill rig count continues to recover, reaching a 17-month high. Total U.S. steel imports and apparent steel supply both have shown gains in recent months.

See the chart below for other key metrics in the month of September:

By Brett Linton, Brett@SteelMarketUpdate.com