Market Data

April 1, 2025

SMU price ranges: Tags mixed as market seeks tariff clarity ahead of 'Liberation Day'

Written by Brett Linton & Michael Cowden

Sheet and plate prices were mixed on Tuesday as the market took a wait-and-see approach to the Trump administration’s “Liberation Day” tariffs.

Prices

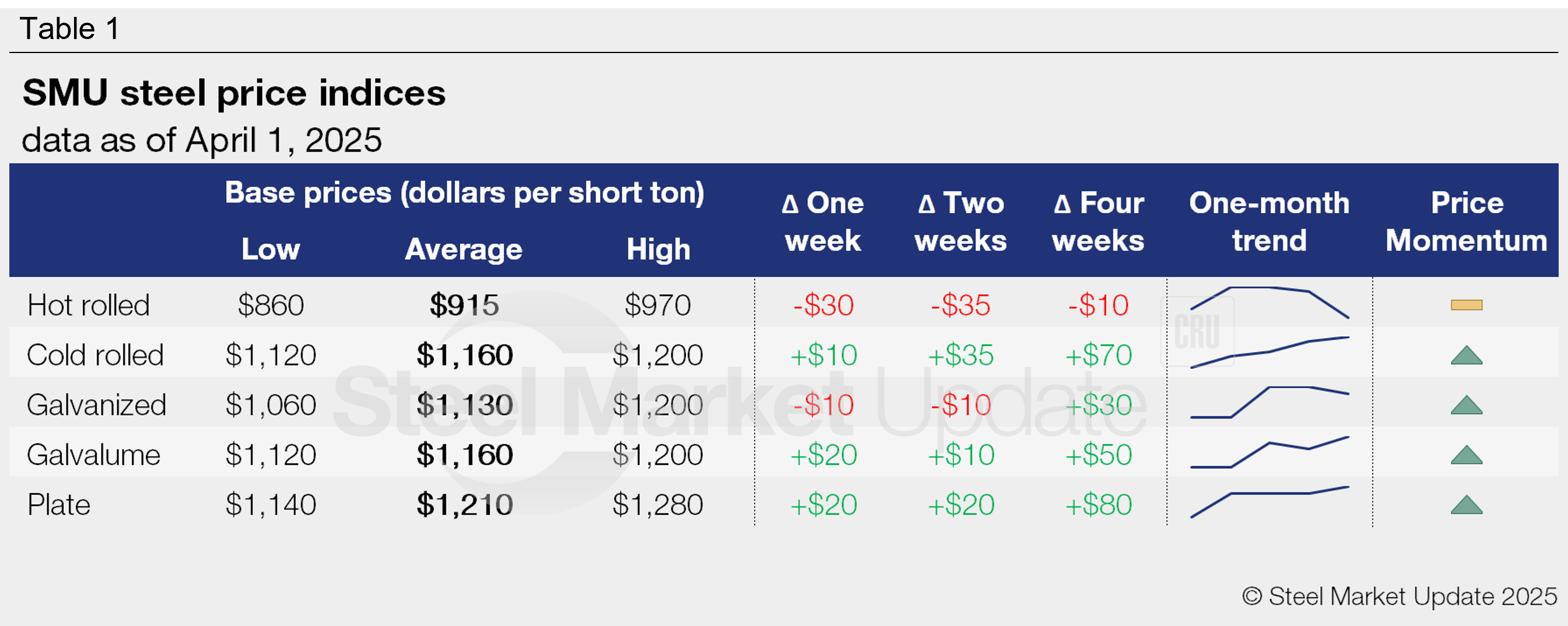

SMU’s hot-rolled coil price fell to $915 per short ton (st) on average, down $30/st from last week and down $35/st from a year-to-date peak of $950 ton in mid-March.

The lower end or our range ($860/st) reflects bigger deals as well as lower prices from new capacity that continues to ramp up. The higher end represents smaller spot deals. No very large deals (10,000 tons or more) were reported this week. That’s because big, speculative buyers have mostly moved to the sidelines as they wait on tariff news.

Cold-rolled prices, in contrast, weighed in at $1,160/st on average, up $10 from a week earlier. Coated prices were mixed. Galvanized base prices were at $1,130/st on average, down $10/st compared to last week. Galvalume prices rose $20/st to $1,160/st on average.

Plate, meanwhile, inched up $20/st to $1,210/st on average on the heels of price increases by US mills – even if the jury remains out on whether those price hikes will entirely stick.

Market commentary

Much depends on Trump’s tariff announcements on Wednesday. A lot hinges, too, on what preliminary anti-dumping numbers will be in the coated trade case. Those are scheduled to be released on Thursday.

What’s clear now is this: After a frenzy of buying ahead of revamped Section 232 tariffs going into effect in March, consumers have slowed the pace of purchases in recent weeks, market participants said.

That’s in part because there are too many variables to game out until the new tariff regime is unveiled. Sheet prices should move higher if tariffs are adjusted higher, lower if there are exemptions and exceptions, and could be little changed if there are – at least for steel – no major changes to existing tariffs, steel buyers said.

Some market participants expressed concerns that tariff-related inflation could hurt demand. Others said that any short-term pain would be justified if tariffs succeed in bringing more manufacturing back to the US. Some also noted that the effect of Section 232 tariffs on Canada has already been severe. Material was said to be stacking up north of the border without the typical outlet provided by the US market.

In short, market participants disagreed over whether the tariffs were good or bad for steel or the broader economy. But opinion was nearly unanimous on this point: Certainty after weeks of waiting for “Liberation Day” will be better than current state of limbo.

Recall that the 25% tariffs on cars and trucks that Trump has already announced are scheduled to go into effect at 12:01 am ET on Thursday, according to official documents. The White House has said other tariffs could go into effect as soon as Trump announces them. He is expected to do so at a 4 pm ET press conference on Wednesday.

Momentum

SMU’s momentum indicator for HR remains at Neutral. Our indicators for other products continue to point to Higher. That’s because prices continue to rise or because, in the case of coated products, tags could move higher after preliminary anti-dumping duties are announced.

Refer to Table 1 for the latest SMU steel price indices and how prices have trended in recent weeks (click to expand).

Hot-rolled coil

The SMU price range is $860-970/st, averaging $915/st FOB mill, east of the Rockies. The lower and upper ends of our range are down $30/st week over week (w/w). Our overall average is down $30/st w/w. Our price momentum indicator for hot-rolled steel remains at Neutral, meaning we see no clear direction for prices over the next 30 days.

Hot rolled lead times range from 4-8 weeks, averaging 5.6 weeks as of our March 19 market survey. We will publish updated lead times on Thursday.

Cold-rolled coil

The SMU price range is $1,120–1,200/st, averaging $1,160/st FOB mill, east of the Rockies. The lower end of our range is up $20/st w/w, while the top end is unchanged w/w. Our overall average is up $10/st w/w. Our price momentum indicator for cold-rolled steel remains at Higher, meaning we expect prices to increase over the next 30 days.

Cold rolled lead times range from 6-9 weeks, averaging 7.3 weeks through our latest survey.

Galvanized coil

The SMU price range is $1,060–1,200/st, averaging $1,130/st FOB mill, east of the Rockies. The lower end of our range is down $20/st w/w, while the top end is unchanged w/w. Our overall average is down $10/st w/w. Our price momentum indicator for galvanized steel remains at higher, meaning we expect prices to increase over the next 30 days.

Galvanized .060” G90 benchmark: SMU price range is $1,157–1,297/st, averaging $1,227/st FOB mill, east of the Rockies.

Galvanized lead times range from 6-10 weeks, averaging 7.5 weeks through our latest survey.

Galvalume coil

The SMU price range is $1,120–1,200/st, averaging $1,160/st FOB mill, east of the Rockies. The lower end of our range is up $40/st w/w, while the top end is unchanged w/w. Our overall average is up $20/st w/w. Our price momentum indicator for Galvalume steel remains at Higher, meaning we expect prices to increase over the next 30 days.

Galvalume .0142” AZ50, grade 80 benchmark: SMU price range is $1,414–1,494/st, averaging $1,454/st FOB mill, east of the Rockies.

Galvalume lead times range from 7-10 weeks, averaging 8.0 weeks through our latest survey.

Plate

The SMU price range is $1,140–1,280/st, averaging $1,210/st FOB mill. The lower end of our range is up $40/st w/w, while the top end is unchanged w/w. Our overall average is up $20/st w/w. Our price momentum indicator for plate remains at higher, meaning we expect prices to increase over the next 30 days.

Plate lead times range from 4-8 weeks, averaging 5.5 weeks through our latest survey.

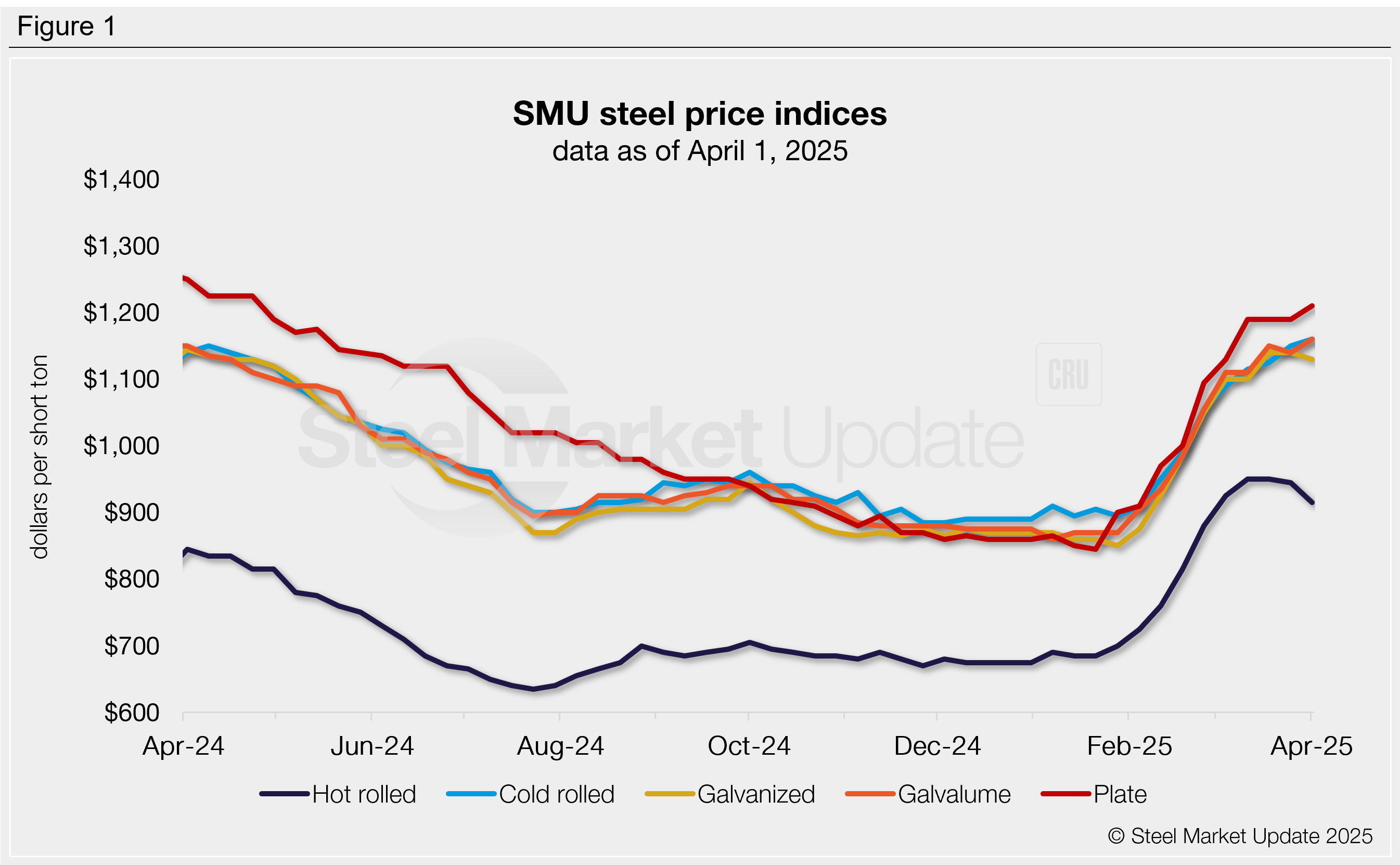

SMU note: Above is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume, and plate price history. This data is also available here on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@steelmarketupdate.com.

Brett Linton

Read more from Brett Linton