Market Data

May 1, 2025

SMU Survey: Sheet and plate lead times flatten out

Written by Brett Linton

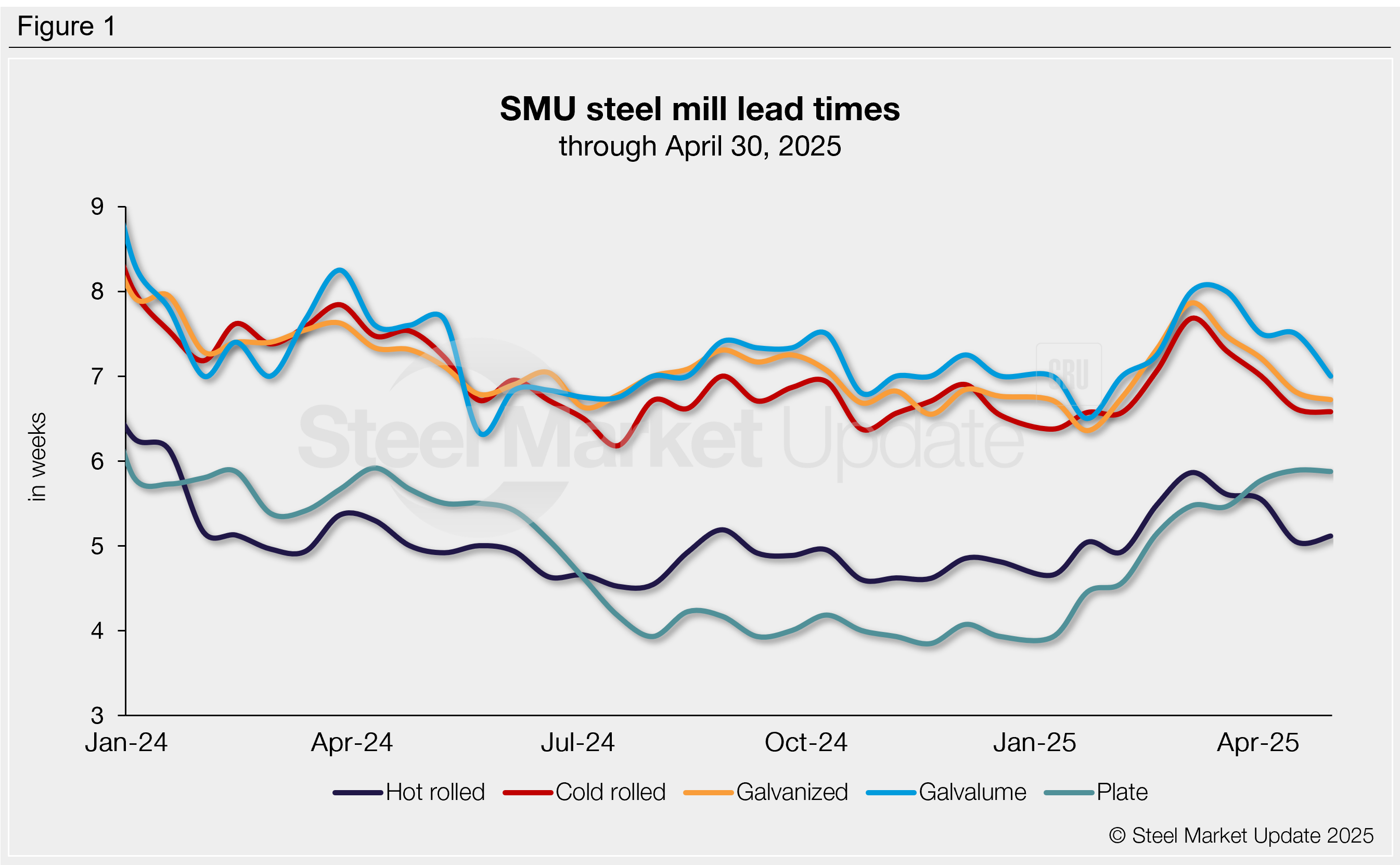

Sheet and plate lead times held steady this week, according to buyers responding to the latest SMU market survey. This week we saw little change from mid-April levels, with just one product (Galvalume) showing any significant movement.

Steel mill production times had stretched out back in February when buyers pulled forward orders on tariff worries and mill outages. That surge proved to be short-lived on sheet products, with lead times peaking in early March and shrinking after.

As of this week, most sheet lead times are roughly half a week longer than the lowest levels seen over the last year. Meanwhile, plate lead times are approximately two weeks longer, holding near one-year highs.

The average lead time for hot-rolled steel is just over five weeks. Tandem products range from seven-and-a-half to seven weeks, while plate remains just under six weeks.

Table 1 summarizes current lead times and recent changes by product (click to expand).

Compared to our April 16 market check, only one of our lead time ranges shifted this week, Galvalume. The shortest lead time declined from seven weeks to six, and the longest lead time decreased from nine weeks to eight.

No change in buyers’ outlook

The majority of buyers (76%) continue to predict lead times will hold steady across the next two months, a rate we have seen grow in each of our last six surveys. Of the remainder, 21% expect production times will contract further (unchanged from mid-April but was previously growing since mid-March). Just 3% anticipate lead times will extend from here, a rate we have seen gradually decline since February.

Here are some of the comments we collected:

“We are already seeing lead times slip, and coming out of the spring outages with demand so weak, they’ve got nowhere to go from here but lower.”

“Demand is too weak to cause lead times to extend and they can’t drop too much more.”

“Lead times will pull back in the next few months then flatten out.”

“I believe they will contract over the next two months and then be flat to up again.”

“They will stay flat. There is average demand but plenty of supply.”

Trends

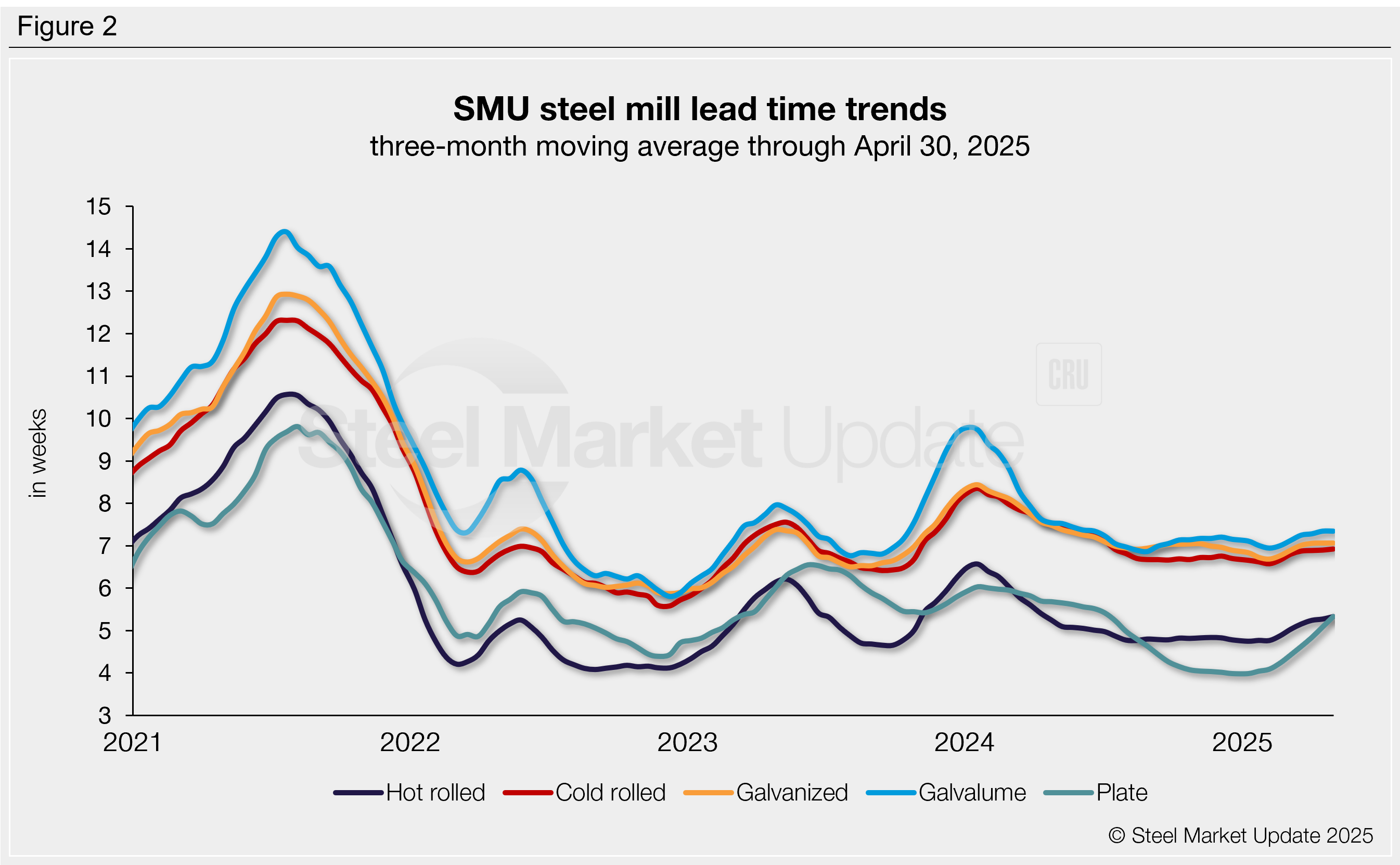

Lead times can be calculated on a three-month moving average (3MMA) basis to smooth out biweekly fluctuations and better highlight trends. This is now the sixth straight survey where our 3MMA lead times have increased across the board. These gains were preceded by a year-long decline, during which production times had fallen to multi-year lows (Figure 2).

Over the past three months, the average lead times by product are as follows: hot rolled at 5.33 weeks, cold rolled at 6.92 weeks, galvanized at 7.06 weeks, Galvalume at 7.34 weeks, and plate at 5.33 weeks.

Note: These lead times are based on the average from manufacturers and steel service centers participating in this week’s SMU market trends analysis survey. SMU measures lead times as the time it takes from when an order is placed with the mill to when it is processed and ready for shipping, not including delivery time to the buyer. Our lead times do not predict what any individual may get from any specific mill supplier. Consult your mill rep for actual lead times. To see an interactive history of our steel mill lead times data, visit our website. If you’d like to participate in our survey, contact us at info@steelmarketupdate.com.