Market Data

May 22, 2025

Steelmaking raw material costs mixed through May

Written by Brett Linton

Editor’s note: Steel Market Update is pleased to share this Premium content with Executive members. For information on how to upgrade to a Premium-level subscription, contact Luis Corona at luis.corona@crugroup.com.

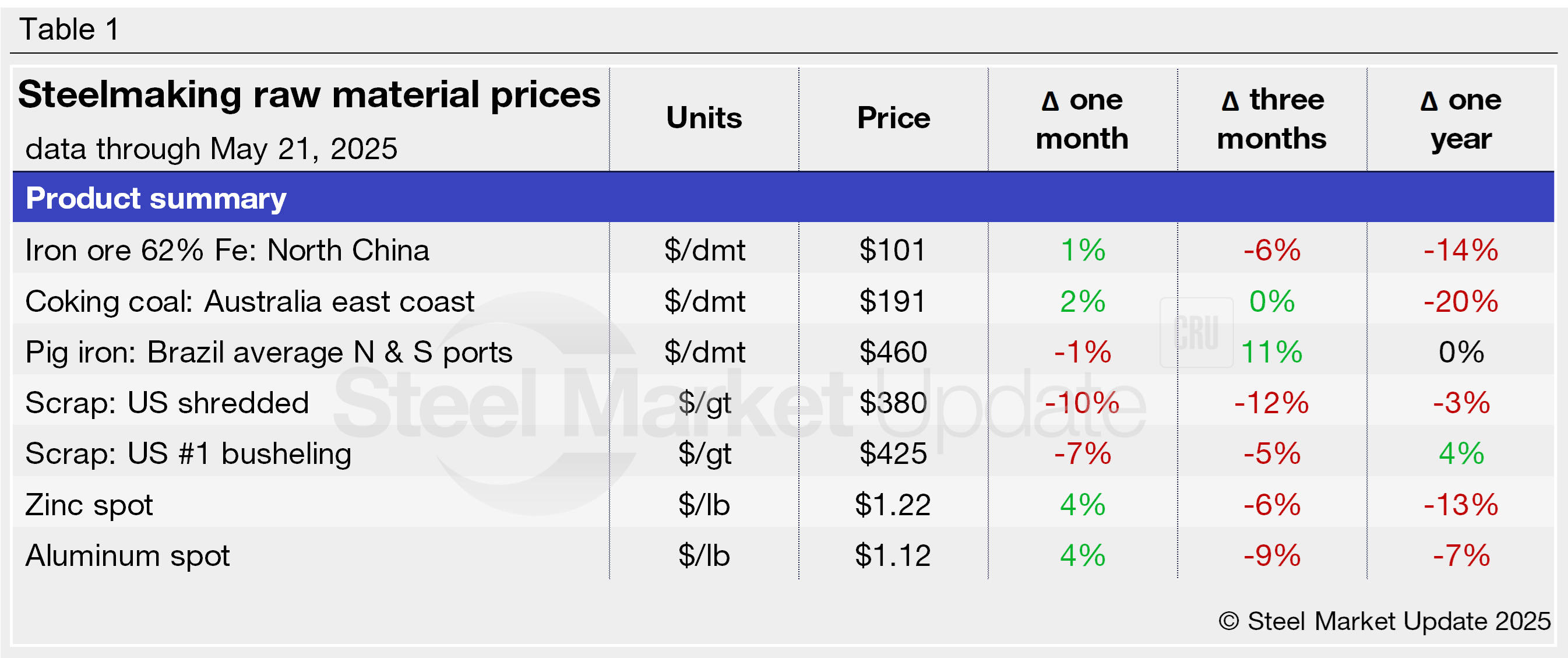

According to our latest analysis, prices for four of the seven steelmaking raw materials we track increased from April to May. However, select materials saw a collective 1% decline month over month and are down 4% compared to three months ago.

Zinc, aluminum, coking coal, and iron ore all saw month-over-month (m/m) price increases, while busheling scrap, shredded scrap, and pig iron declined. Five of the seven materials are now priced lower than they were three months ago, and most are similar to or cheaper than they were one year ago.

Table 1 (click to expand) shows the latest prices for each product and their changes from recent months.

Iron ore

The import price of 62% Fe Chinese iron ore fines has increased each of the last two weeks following the seven-month low of $97 per dry metric ton (dmt) reached in mid-April. Prices have generally hovered between $97-$109/dmt since October. As of May 21, the weekly spot price is up to a six-week high of $101/dmt delivered North China (Figure 1). Iron ore is 6% less expensive than it was three months ago and 14% cheaper than one year ago.

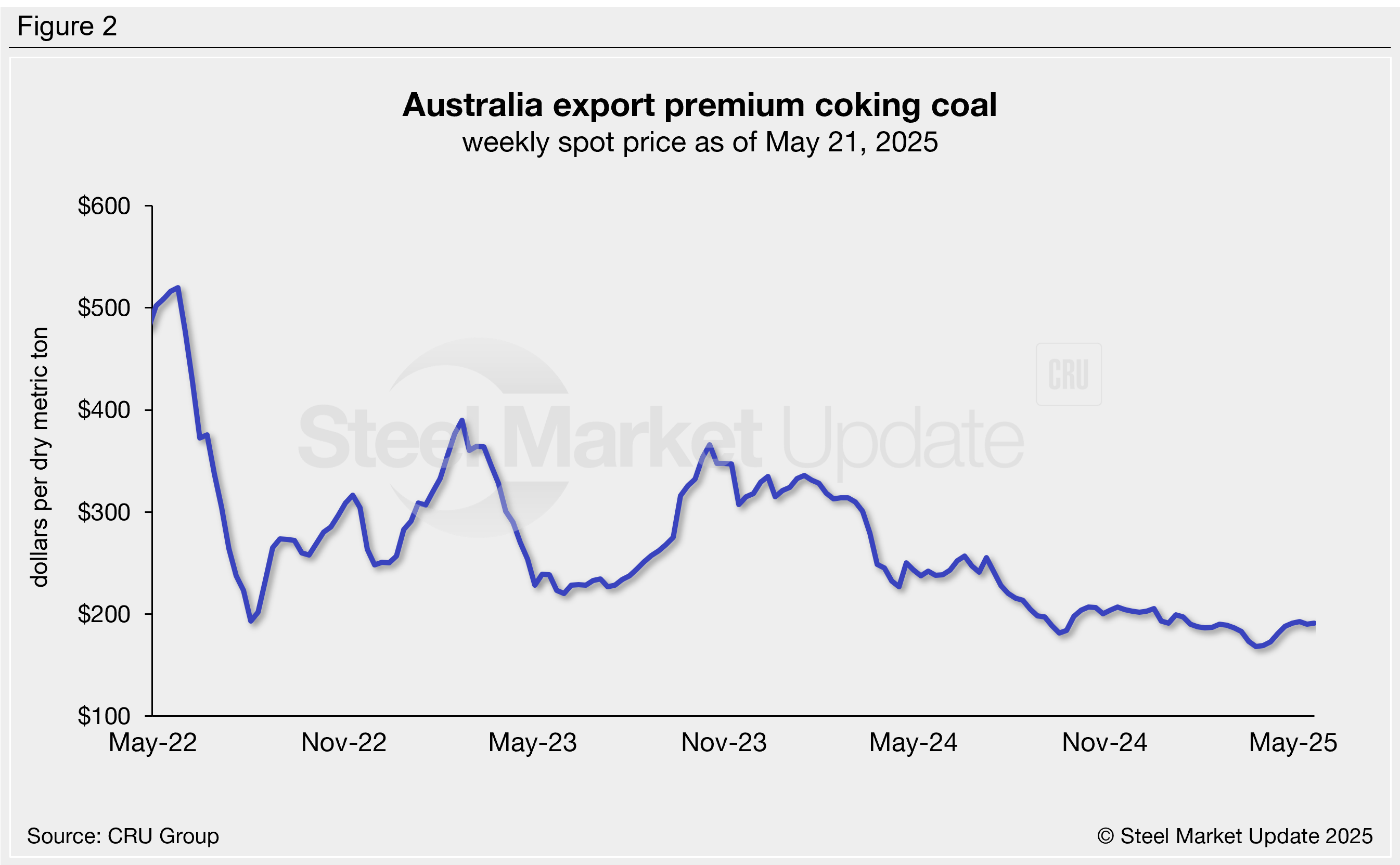

Coking coal

Premium hard coking coal prices have trended lower since late 2023, recently reaching a near four-year low of $168/dmt in late March. Prices have since ticked higher, increasing to $191/dmt this week (Figure 2). Coking coal is less than 1% more expensive than it was three months ago, though 20% lower than this time last year.

Pig iron

After falling to a four-year low of $415/dmt earlier this year, pig iron prices rebounded to $465/dmt in March and have remained in that ballpark since. The latest monthly price is down 1% in May to $460/dmt (Figure 3). Despite the recent dip, prices are 11% higher than they were three months ago and identical to May 2024 levels.

Recall that pig iron prices soared to a historic high of $975/dmt in April 2022 following the invasion of Ukraine. Most of the pig iron imported to the US was imported from Russia, Ukraine, and Brazil. This report uses Brazilian prices (now the primary source of US pig iron imports) and averages prices from the country’s northern and southern ports.

Scrap

Steel scrap prices have edged lower since peaking in March, slipping 7%-10% from April to May. Shredded scrap prices fell $40 per gross ton (gt) this month to $380/gt, while busheling scrap declined $30/gt to $425/gt (Figure 4). Scrap is down compared to prices seen three months ago, between 5%-12%. Compared to this time last year, busheling scrap prices are 4% more expensive, while shredded scrap is 3% cheaper.

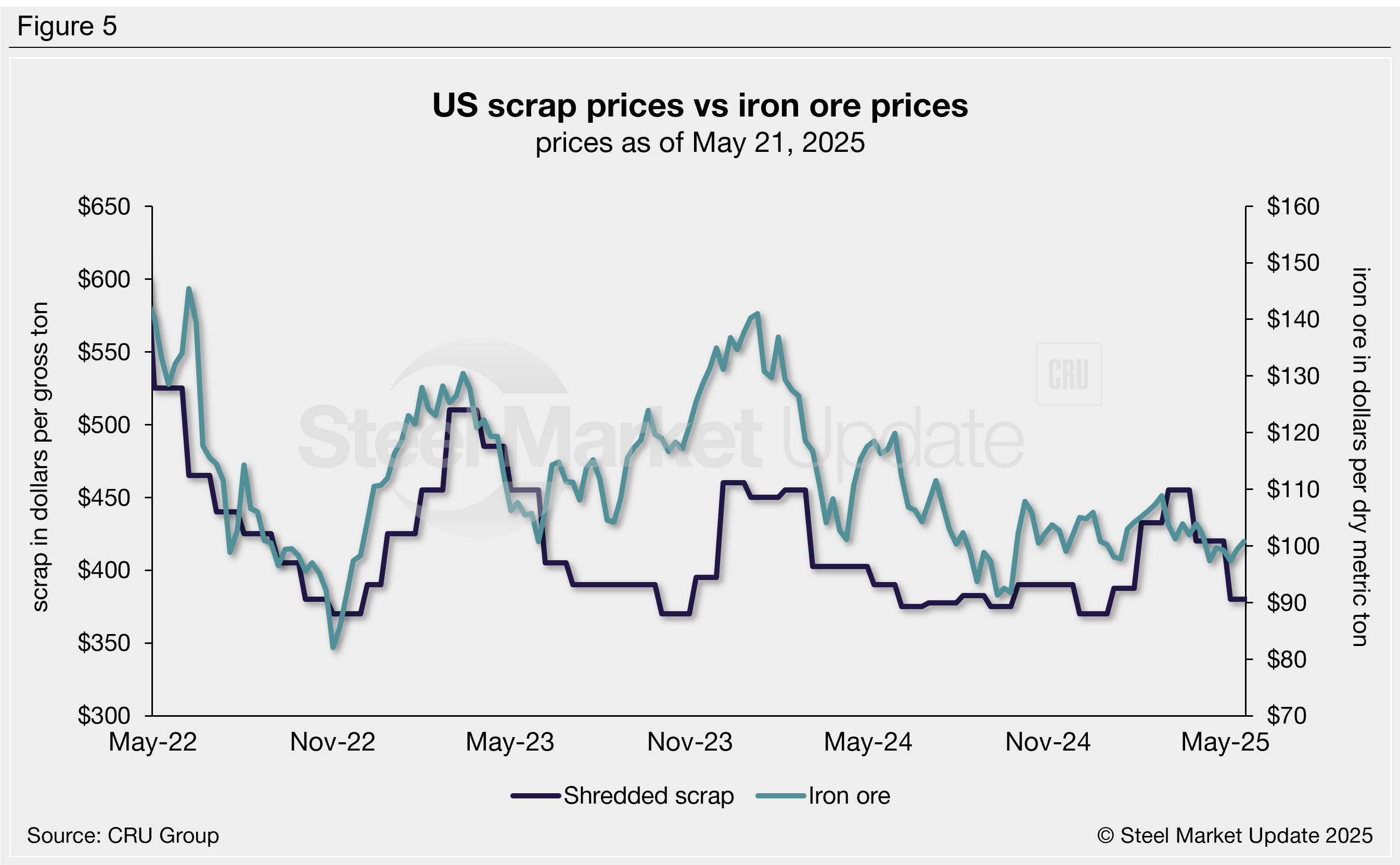

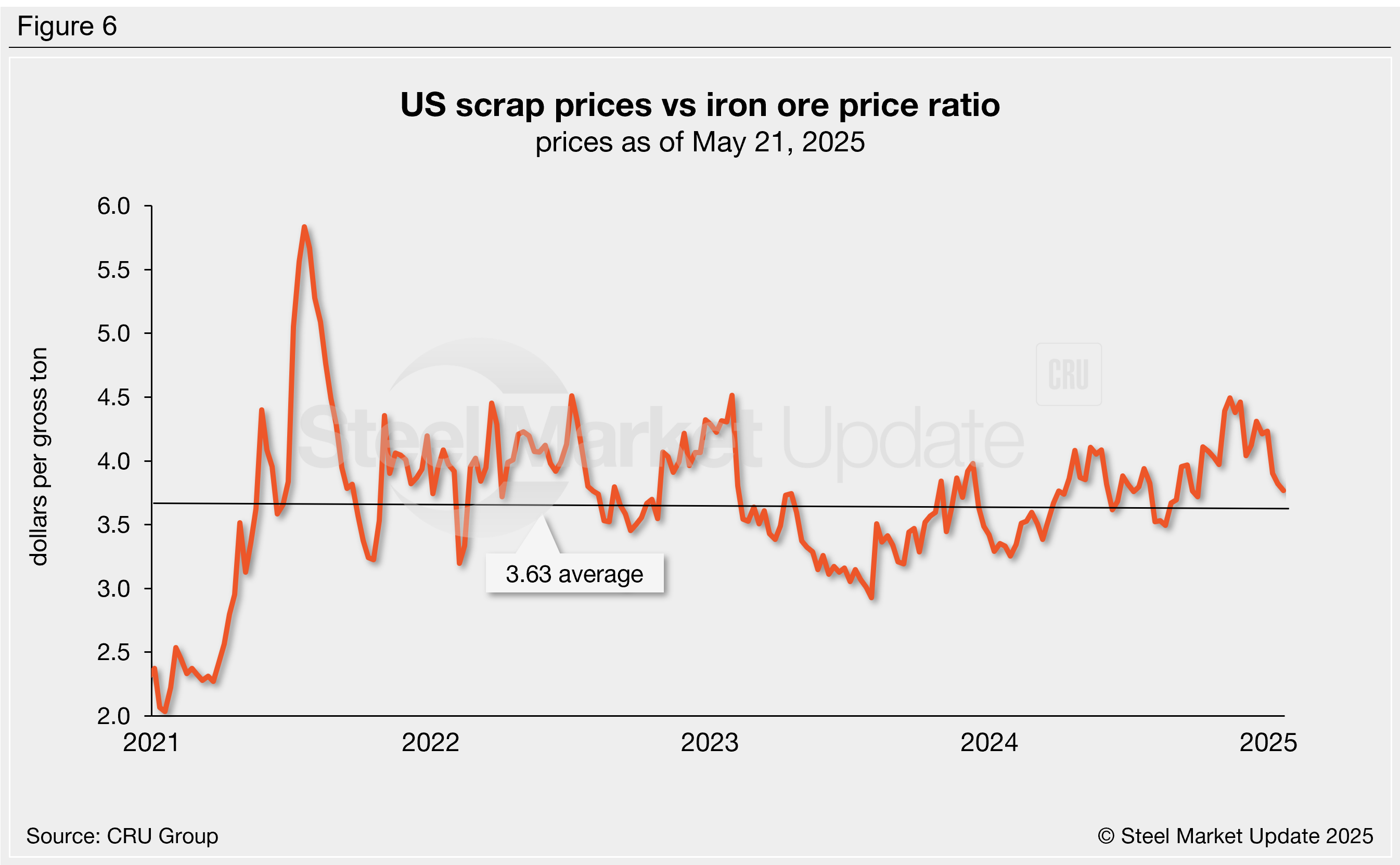

Fluctuations in scrap and iron ore prices provide insight into the competitiveness of integrated (blast furnace) mills, whose primary feedstock is iron ore, versus to mini-mills (electric arc furnace), whose primary feedstock is scrap. Figure 5 compares the prices of these two mill raw materials.

To compare these two mill feedstocks, SMU divides the shredded scrap price by the iron ore price to calculate a ratio. A high ratio favors the integrated mills, a lower ratio favors the mini-mill producers.

Integrated mills generally held the cost advantage from late 2021 through mid-2023, then it briefly shifted to mini-mill producers in the second half of 2023 (Figure 6). After bouncing around in 2024, the ratio has slightly favored integrated mills since last August. It has trended lower since touching to a near two-year high in March (4.50), standing at 3.77 as of May 21.

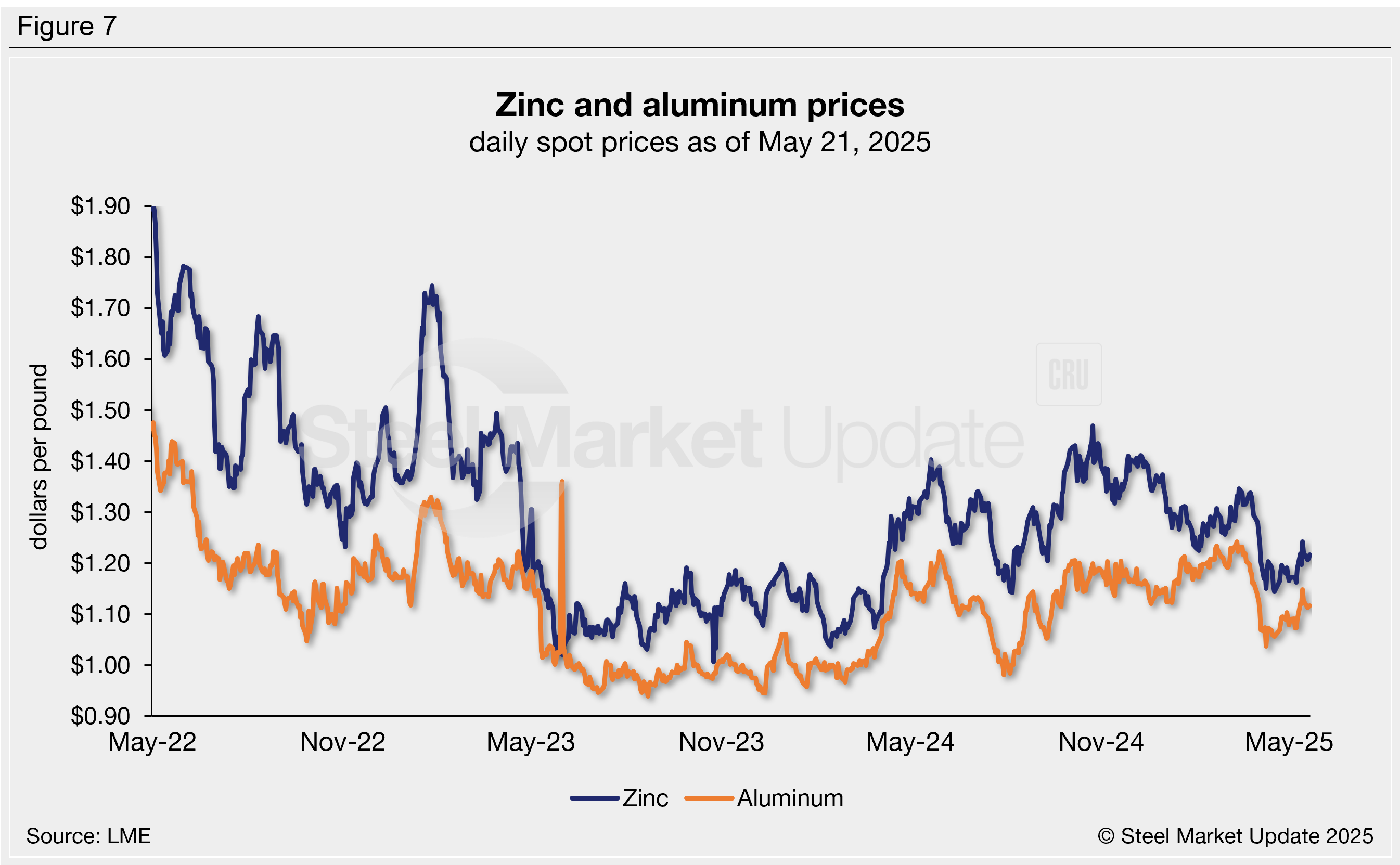

Zinc and aluminum

Zinc and aluminum are used in some coated steel products. Fluctuations in spot prices can prompt steel mills to adjust their galvanized and Galvalume coating extras.

Zinc prices have generally moved higher over the past month but remain near some of the lowest levels recorded in the last eight months. The latest LME cash price for zinc is $1.22 per pound as of May 21, 4% higher than a one month ago. Zinc prices are 6% lower than they were three months ago, and 13% cheaper than price seen one year ago (Figure 7).

Aluminum price movements have closely mirrored zinc over the last four months. The latest LME cash price is $1.12/lb, up 4% m/m. Aluminum prices are 9% lower than they were three months ago and down 7% from May 2024 levels. Note that aluminum spot prices can be volatile at times, though sharp swings typically correct within a few days, as seen once in Figure 7.