Market Data

May 29, 2025

SMU Survey: Sheet lead times fall to multi-year low

Written by Brett Linton

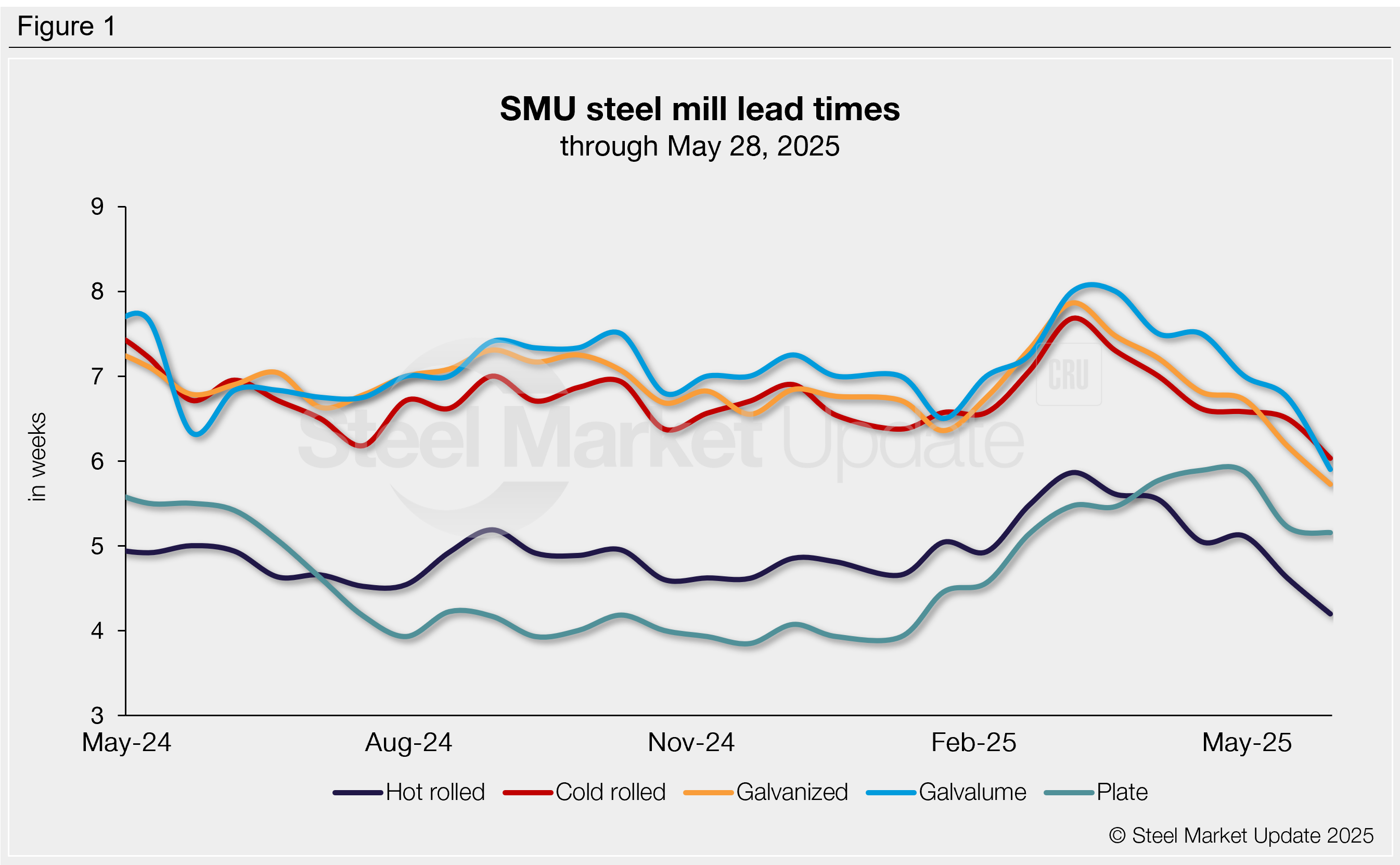

Mill lead times shrunk this week for all of the sheet products tracked by SMU and held steady on plate, according to buyers responding to our latest market survey.

Overall, average sheet production times are two weeks shorter than they were three months ago, now at the lowest levels we’ve recorded since late 2022. Plate times have trended down since early May, currently at a three-month low.

The average lead time for hot-rolled steel is now just over four weeks. Cold-rolled and coated products have eased to around six weeks, and plate is holding at just over five weeks.

Table 1 summarizes current lead times and recent changes by product (click to expand)

Compared to our May 14 market check, our coated product lead time ranges shifted lower this week:

- Galvanized: The shortest lead time recorded declined from five weeks to four, and the longest lead time dropped from eight weeks to seven.

- Galvalume: The shortest lead time fell from six weeks to five, while the longest lead time declined from eight weeks to seven.

Buyers predict stability

The majority of buyers (73%) expect lead times will remain stable over the next two months, up from 65% in mid-May. Of the remainder, 17% anticipate further contractions, down from 26%. Just 9% expect lead times to extend, similar to what we heard two weeks ago.

Here are some of the comments we collected:

“They can’t get too much shorter.”

“Flat, demand is weakening on our end.”

“Flat as supply is up and demand is down.”

“After falling in the next month, we will see a rebound.”

“Talking to my mill, many customers like me are doing their best to delay ordering given stock on hand and high reorder prices. I can’t pass on the steel price increases on my products.” [flat lead times]

“Contracting with the economic slowdown due to tariffs, coupled with increases in North American capacity.”

“Bigger guys are still bringing in imports and the inventories at SSCs and OEMs remain pretty solid. All of that is bad news for the domestics.” [contracting lead times]

Trends

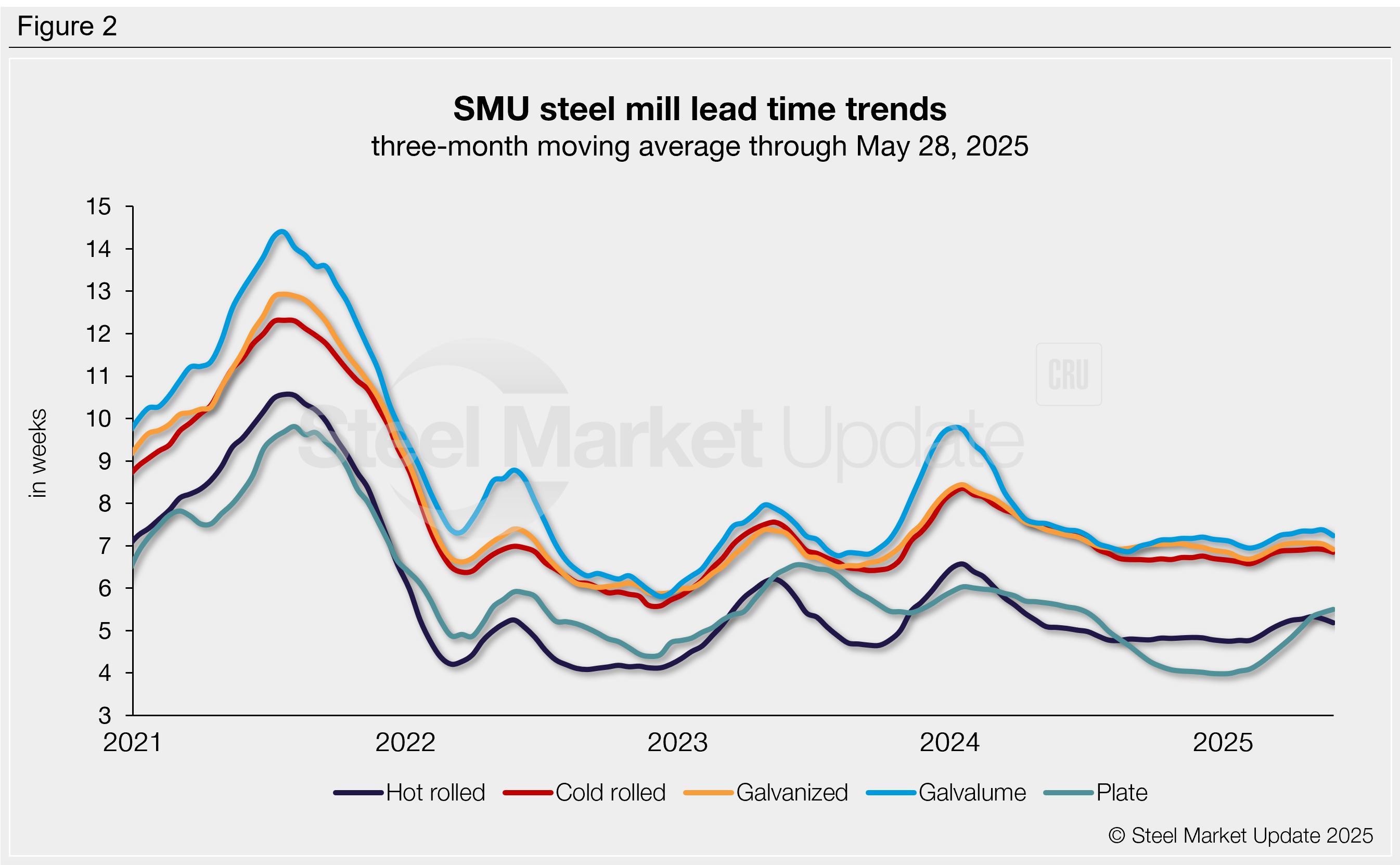

Lead times can be calculated on a three-month moving average (3MMA) to smooth out biweekly fluctuations and better highlight trends (Figure 2). All of our sheet 3MMAs declined this week for the second-consecutive survey, while plate moved slightly higher, as it has since the start of the year.

Across the last three months, the average lead times by product are as follows: hot rolled at 5.18 weeks, cold rolled at 6.85 weeks, galvanized at 6.91 weeks, Galvalume at 7.24 weeks, and plate at 5.50 weeks.

Note: These lead times are based on the average from manufacturers and steel service centers participating in this week’s SMU market trends analysis survey. SMU measures lead times as the time it takes from when an order is placed with the mill to when it is processed and ready for shipping, not including delivery time to the buyer. Our lead times do not predict what any individual may get from any specific mill supplier. Consult your mill rep for actual lead times. To see an interactive history of our steel mill lead times data, visit our website. If you’d like to participate in our survey, contact us at info@steelmarketupdate.com.