Analysis

June 9, 2025

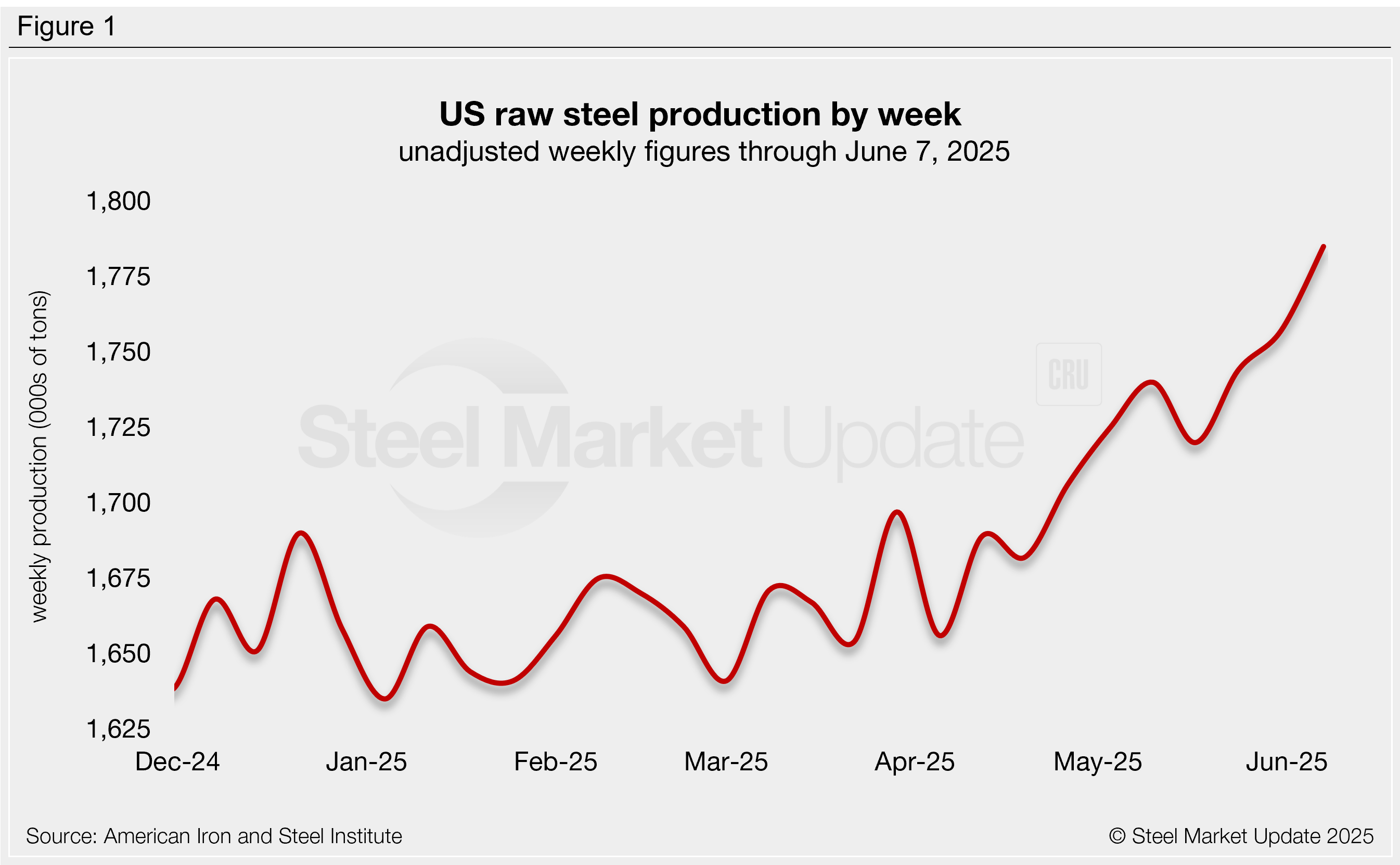

AISI: Raw steel production climbs to three-year high

Written by Brett Linton

Domestic steel mills are ramping up production, according to the American Iron and Steel Institute (AISI), with output rising to a three-year high last week.

US mills produced an estimated 1,785,000 short tons (st) of raw steel for the week ending June 7, a 28,000-st (or 1.6%) increase from the prior week (Figure 1). This represents the highest unadjusted weekly production figure since May 2022. Mill output has trended higher since April. It has also increased in six of the last seven weeks.

Last week’s production was 5.9% above the year-to-date (YTD) average of 1,686,000 st per week and 4.8% higher than the same week of 2024.

The mill capability utilization rate was 79.5% last week, up from 78.2% the previous week and up from 76.7% one year ago. This is the highest rate recorded since September 2024.

YTD production stands at 38,072,000 st with a capability utilization rate of 75.5%. After a slower first quarter than 2024, 2025 output is catching up. It is now just 93,000 st (0.2%) below the same period of last year.

Raw production increased week over week (w/w) in four of the five AISI-defined regions:

- Northeast – 128,000 st (down 3,000 st w/w)

- Great Lakes – 535,000 st (up 3,000 st)

- Midwest – 252,000 st (up 17,000 st)

- South – 802,000 st (up 9,000 st)

- West – 68,000 st (up 2,000 st)

Editor’s note: The raw steel production tonnage provided in this report is estimated and should be used primarily to assess production trends. The graphic included in this report shows unadjusted weekly data. The monthly AISI “AIS 7” report is available by subscription and provides a more detailed summary of domestic steel production.