Analysis

July 29, 2025

SMU Price Ranges: Sheet prices tick lower, but floor remains high vs. '24

Written by David Schollaert & Michael Cowden

Sheet prices slipped again this week amid discounting from certain mills and ongoing concerns about demand.

But SMU’s price assessments remain ~$200 per short ton (st) higher than they were a year ago thanks in large part to tariffs raising the floor on prices.

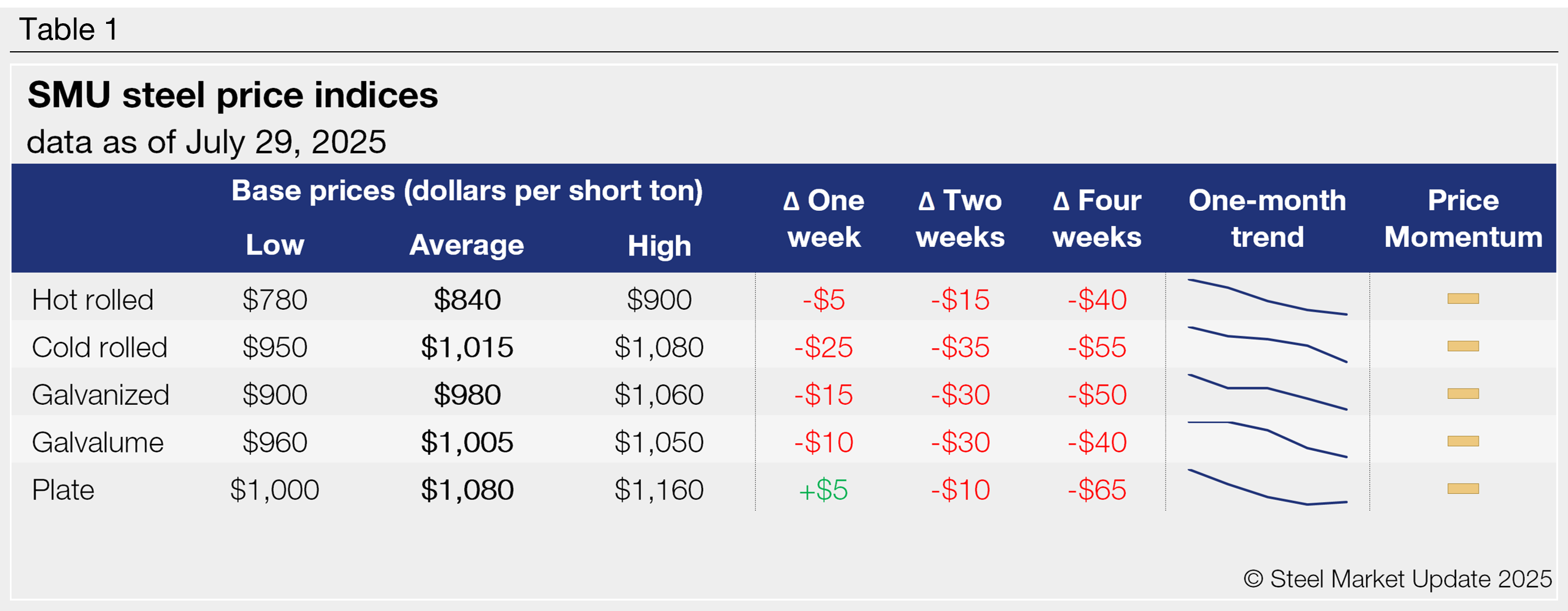

SMU’s hot-rolled coil price now stands at $840/st on average, down $5/st from last week.

The low end of our range is at $780/st. The high end of our range is at $900/st.

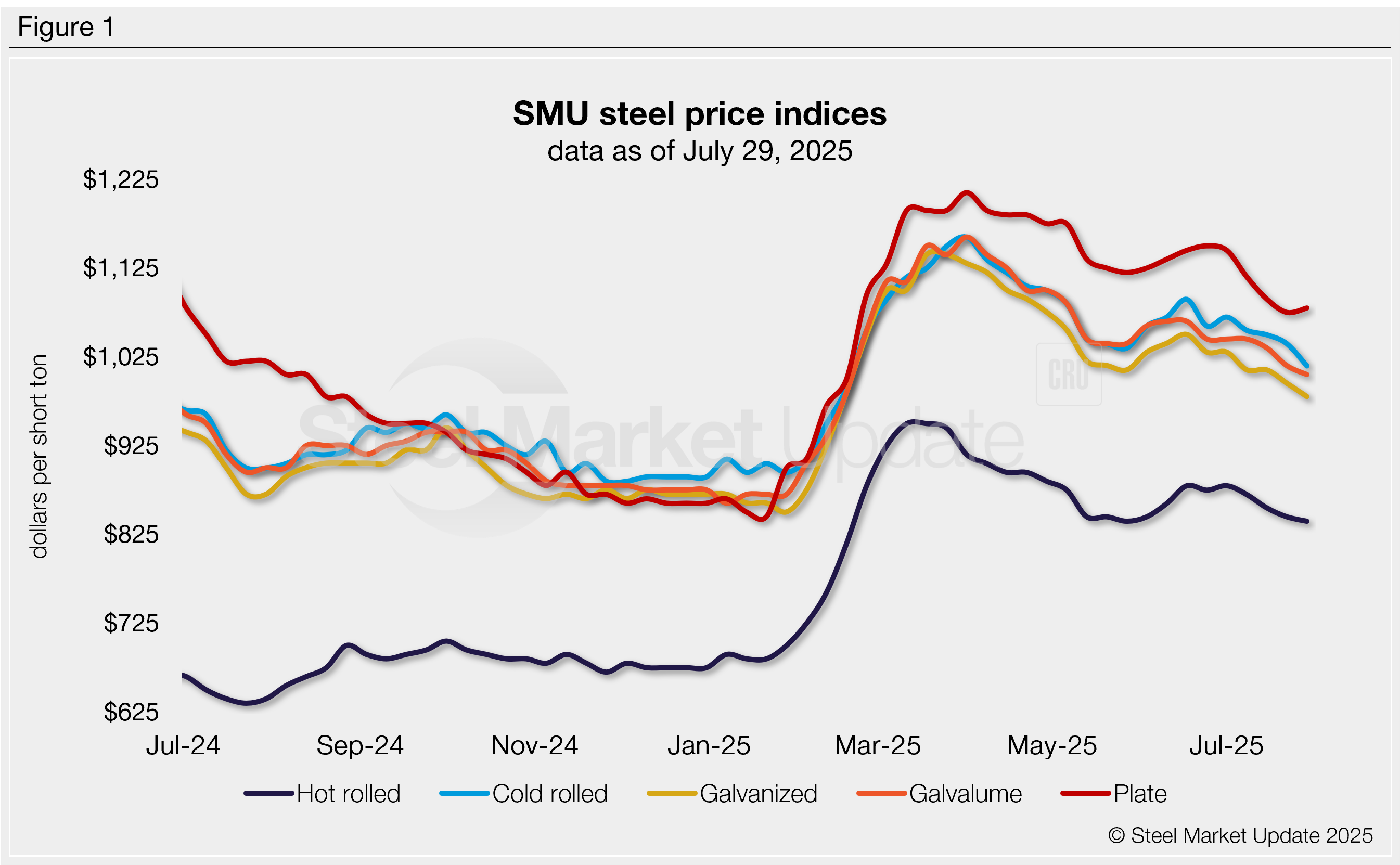

A year ago, SMU’s HR price stood at $640/st on average. Our low end was at $600/st, and our high end was at $680/st, according to our interactive pricing tool.

Why that range?

Nucor’s list price is $900/st, and some sources reported transactions at that level. Production from new capacity is closer to ~$800/st. And some mills in the Great Lakes area were in the mid/upper $700s/st as they looked to lower prices to bring in volume, market participants said.

CR and coated

It was a similar story with cold-rolled and coated products, where start-up tons and tons from certain mills were priced significantly lower than tons from other mills.

All told, SMU’s price for cold-rolled coil stands at $1,015/st on average, down $25/st from last week. Our galvanized price is at $980/st on average, $15/st lower than last week. And our Galvalume price is at $1,005/st on average, $10/st lower than past week.

Plate prices, meanwhile, were little changed at $1,080/st on average.

Our price momentum indicators remain at neutral until the market establishes a clear direction.

What they’re saying

It’s not uncommon for mills to discount this time of year as they seek to firm up orderbooks ahead of contract negotiations. Some market sources said prices should stabilize when lead times get into September, as inventories continue to move lower, and as mills’ fall maintenance outages approach.

And prices could move higher should demand improve. “Our customers are chewing through more steel in July then they expected. That’s a good sign. And I’m not seeing a lot of erosion,” one producer source said.

Another support could come from a 50% “reciprocal” tariff on Brazil, one that would also cover Brazilian raw materials – including pig iron. The tariff is currently slated to go into effect on Aug. 1. And higher pig iron prices would likely result in higher scrap prices in September.

But other sources said domestic mills might successfully lobby for a carve out for raw materials from Brazil. And some remain unconvinced that demand would improve enough in the fall for mills to pass along higher costs.

Case in point: A service center source said that his regular buyers continued to place orders but that volumes were off: “Your world is filled with 500-ton inquires and 100-ton orders.”

Refer to Table 1 (click to enlarge) for our latest price indices and trends.

Hot-rolled coil

The SMU price range is $780–900/st, averaging $840/st FOB mill, east of the Rockies. The lower end of our range is down $20/st week over week (w/w), while the top end is up $10/st. Our overall average is down $5/st w/w. Our price momentum indicator for hot-rolled steel remains at neutral, meaning we see no clear direction for prices over the next 30 days.

Hot-rolled lead times range from 3–6 weeks, averaging 4.4 weeks as of our July 24 market survey.

Cold-rolled coil

The SMU price range is $950–1,080/st, averaging $1,015/st FOB mill, east of the Rockies. The lower end of our range is down $50/st w/w, while the top end is unchanged. Our overall average is down $25/st w/w. Our price momentum indicator for cold-rolled remains at neutral, meaning we see no clear direction for prices over the next 30 days.

Cold-rolled lead times range from 5–8 weeks, averaging 6.3 weeks through our latest survey.

Galvanized coil

The SMU price range is $900–1,060/st, averaging $980/st FOB mill, east of the Rockies. The lower end of our range is down $30/st w/w, while the top end is unchanged. Our overall average is down $15 w/w. Our price momentum indicator for galvanized steel remains at neutral, meaning we see no clear direction for prices over the next 30 days.

Galvanized .060” G90 benchmark: SMU price range is $978–1,138/st, averaging $1,058/st FOB mill, east of the Rockies.

Galvanized lead times range from 5–8 weeks, averaging 6.1 weeks through our latest survey.

Galvalume coil

The SMU price range is $960–1,050/st, averaging $1,005/st FOB mill, east of the Rockies. The lower end of our range is down $10/st w/w, while the top end is down $10/st. Our overall average is down $10/st w/w. Our price momentum indicator for Galvalume steel remains at neutral, meaning we see no clear direction for prices over the next 30 days.

Galvalume .0142” AZ50, grade 80 benchmark: SMU price range is $1,228–1,318/st, averaging $1,273/st FOB mill, east of the Rockies.

Galvalume lead times range from 5–7 weeks, averaging 6.1 weeks through our latest survey.

Plate

The SMU price range is $1,000–1,160/st, averaging $1,080/st FOB mill. The lower end of our range is up $10/st w/w, while the top end is unchanged. Our overall average is up $5/st w/w. Our price momentum indicator for plate remains at neutral, meaning we see no clear direction for prices over the next 30 days.

Plate lead times range from 3–8 weeks, averaging 5.3 weeks through our latest survey.

SMU note: The graphic above shows a history of our hot rolled, cold rolled, galvanized, Galvalume, and plate prices. This data is also available on our website with our interactive pricing tool. If you need help navigating the site or logging in, contact us at info@steelmarketupdate.com.

David Schollaert

Read more from David Schollaert