Analysis

August 21, 2025

Final Thoughts

Written by Michael Cowden

With SMU Steel Summit starting in just a few days, I decided to go back and do a quick check on where things stand now compared to the week before Summit last year.

In some respects, there are some similarities. Last year, election-related uncertainty kept buyers on the sidelines. This year, it’s tariff-related uncertainty.

In other respects, there is nothing in common. Section 232 tariffs of 50% on all imported steel and tariffs on raw materials too? I don’t think that was on anyone’s bingo card in August 2024.

And yet, prices aren’t as far apart as you might think. SMU’s hot-rolled (HR) coil price stands at $805 per short ton (st) on average now. That’s up 19% (or $130/st) from $675/st this time last year, according to our pricing records. (I wonder where we’d be without a 50% tariff?)

You might have noticed that we adjusted our price momentum indicators to lower from neutral earlier this week. We almost did earlier this summer as well. But the potential of 50% tariffs on Brazilian pig iron gave us pause.

Why did we do it this week? To answer that, I’ll share with you a preliminary taste of the full survey results that we’ll be releasing to our premium members on Friday. (Editor’s note: Proprietary data like this is a good reason to upgrade from executive to premium. Contact SMU Senior Account Executive Luis Corona at luis.corona@crugroup.com if you’d like to.)

For starters, most mills remain willing to negotiate lower prices, according to the steel buyers we survey. And there has been little movement in lead times, despite them now being solidly into September and bumping up against fall maintenance outages.

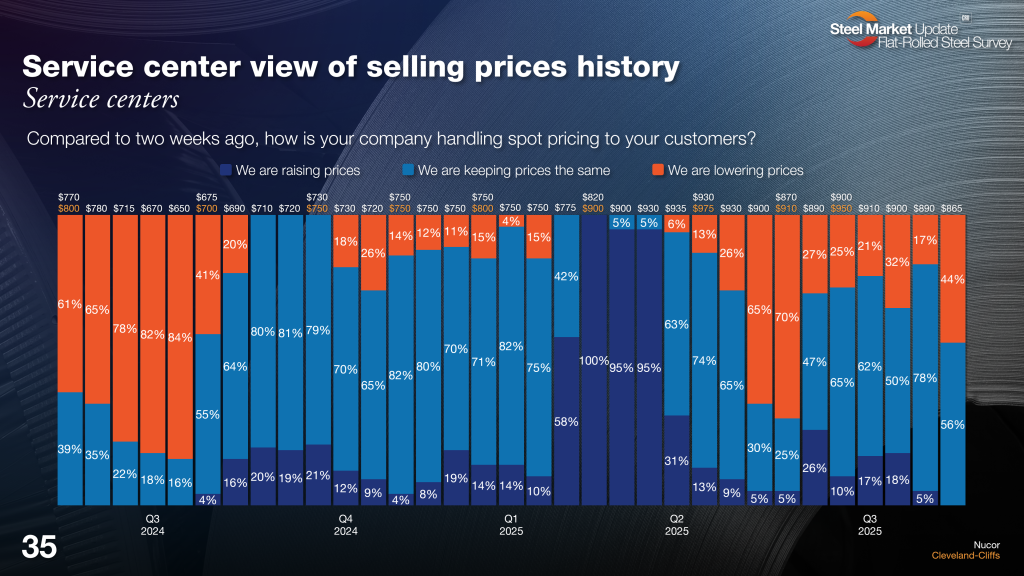

Also, it’s not just mills that are cutting prices. Nearly 45% of respondents to this week’s survey say service centers are lowering prices too. (Note that you can click on all of the charts below to expand them. Also, the page number refers to where in the survey slide deck you’ll be able to find this data on Friday.)

That’s the highest number we’ve seen since before President Trump announced 50% Section 232 tariffs in May.

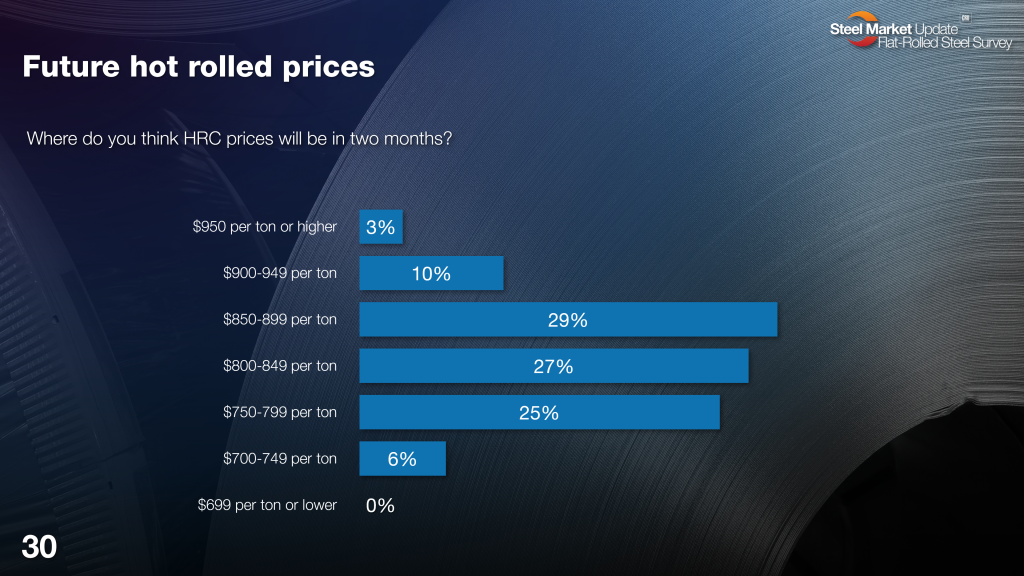

What’s more, expectations of where the market will bottom continue to tick lower:

Sure, most people (56%) think prices will still be in the $800s/st two months from now. That’s roughly where we are now or a little higher.

But a sizable minority (31%) think that prevailing spot prices will fall into the $700s/st. Rewind to earlier this summer, and the consensus was that prices in the $700s/st would be available only to large buyers – and probably only for a limited time.

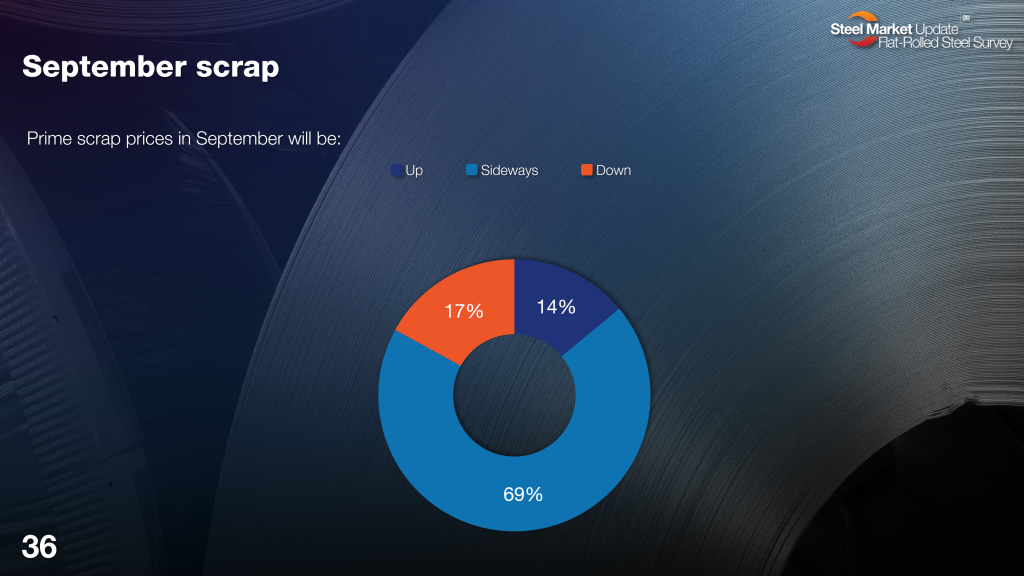

Also, with the threat of 50% tariffs on Brazilian pig iron gone, momentum is out of the scrap market. Most people think scrap prices will be flat or lower in September.

In short, among most buyers there is a sense that there is no urgency to buy now, especially when prices next week will be lower than prices this week – the textbook definition of deflation.

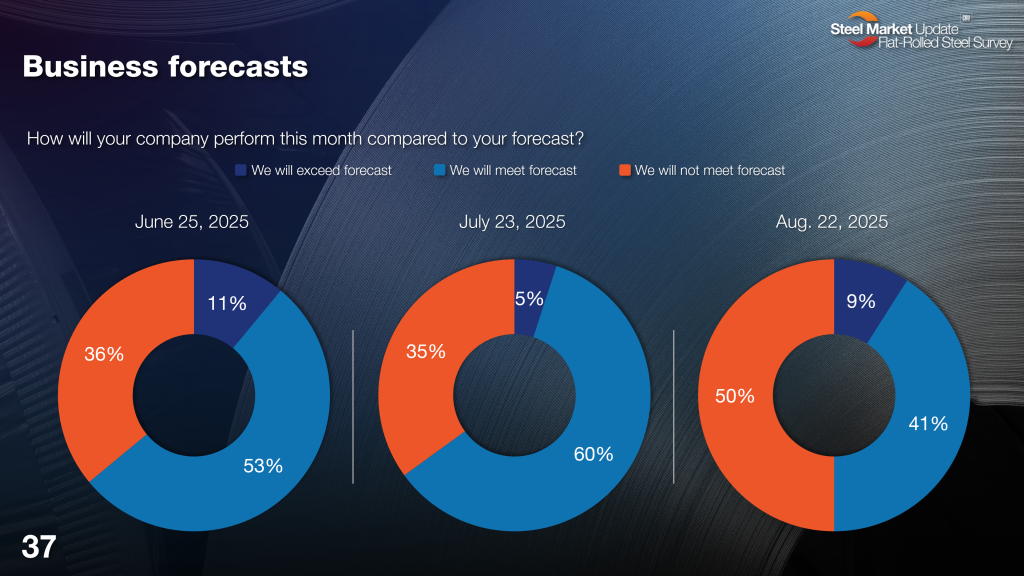

Meanwhile, we’ve seen a notable uptick in the number of people who tell us their companies won’t meet forecast this month:

Typically, when I present this slide, I say the good news is most people continue to say they’ll at least meet forecast, even if fewer people are exceeding it. That’s no longer the case.

Still, you could probably make a good case the market often gets aggressively bearish this time of year.

Last year, HR prices bounced around a bottom of approximately $675-700/st until Trump’s inauguration in 2025. And maybe we’ll see prices rattle around $800-850/st for the rest of the year.

But in past years we’ve often seen HR prices bottom in late August/early September and then recover in the fall. In 2023, for example, HR was at $725/st at the end of August. Tags then surged to $1,040/st, a gain of nearly 44%, by the end of the year.

That fall surge in 2023 had a lot to do with dynamics around a United Auto Workers (UAW) union strike against the “Big Three” automakers. And I’m not suggesting anything of that magnitude is about to happen again.

Still, some of our data hints at the potential for prices to improve later this year.

We’ve heard anecdotal evidence of foreign steel “selling through” the 50% S232 tariff. And there was an uptick in flat-rolled imports last month, according to government data. But my guess is that was more the last gasp of material arriving at the 25% tariff than any indication of a rebound in imports.

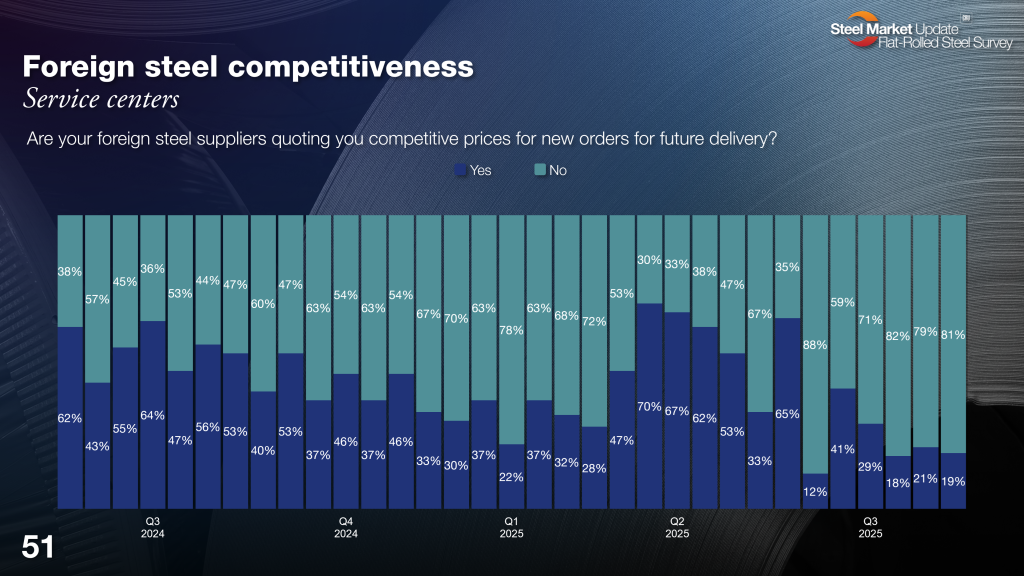

Why do I say that? Look at the chart below:

About 80% of service centers respondents have been telling us for the last six weeks (each bar represents two weeks) that imports are not competitive. Assuming our data leads government figures on imports, I’d be surprised to see import licenses tick higher in the fall.

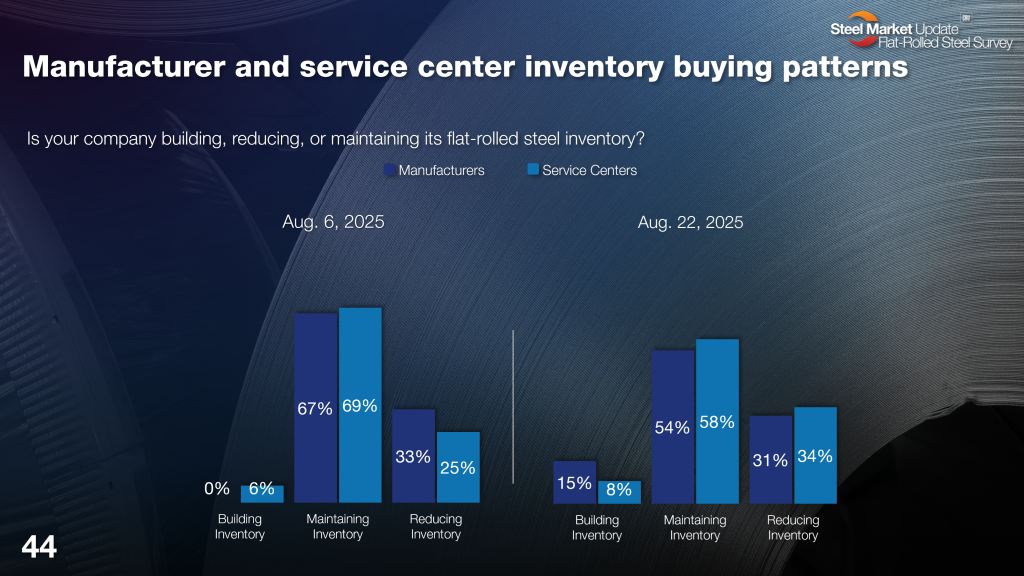

Here’s another piece of SMU proprietary survey data I find interesting. Approximately 15% of manufacturers tell us that they’re building inventory:

Sure, most are maintaining or even reducing inventories. And I don’t want to call a trend reversal base on one survey alone.

But maybe, just maybe, some service centers and manufacturers are looking past the short-term gloom and seeing a light at the end of the tunnel in Q4 that isn’t an oncoming train.

I think the question is whether that light is a restock and the price volatility we often see around those or whether it’s stronger demand as we get closer to 2026.

Steel Summit is almost here!

I’ll be keen to hear how our speakers at Steel Summit see demand shaping up. Because solid demand can make this tariff-rattled market a lot more palatable.

And maybe this is an indication in its own right: We expect more than 1,500 people to attend Steel Summit again this year – potentially breaking a new attendance record despite a tough market. (You can see the list of attendees here.)

Haven’t registered yet? It’s not too late to join us. You can see the full agenda here and register to attend here.

Also, if you’re the last-minute type – there are always a few dozen of you – we also take walk-in registrations.

I look forward to seeing so many of you next week at the Georgia International Convention Center in Atlanta. And, in the meantime, thanks for your continued support of SMU. We really do appreciate it.