Analysis

August 21, 2025

SMU Survey: Buyers report little change in sheet and plate lead times

Written by Brett Linton

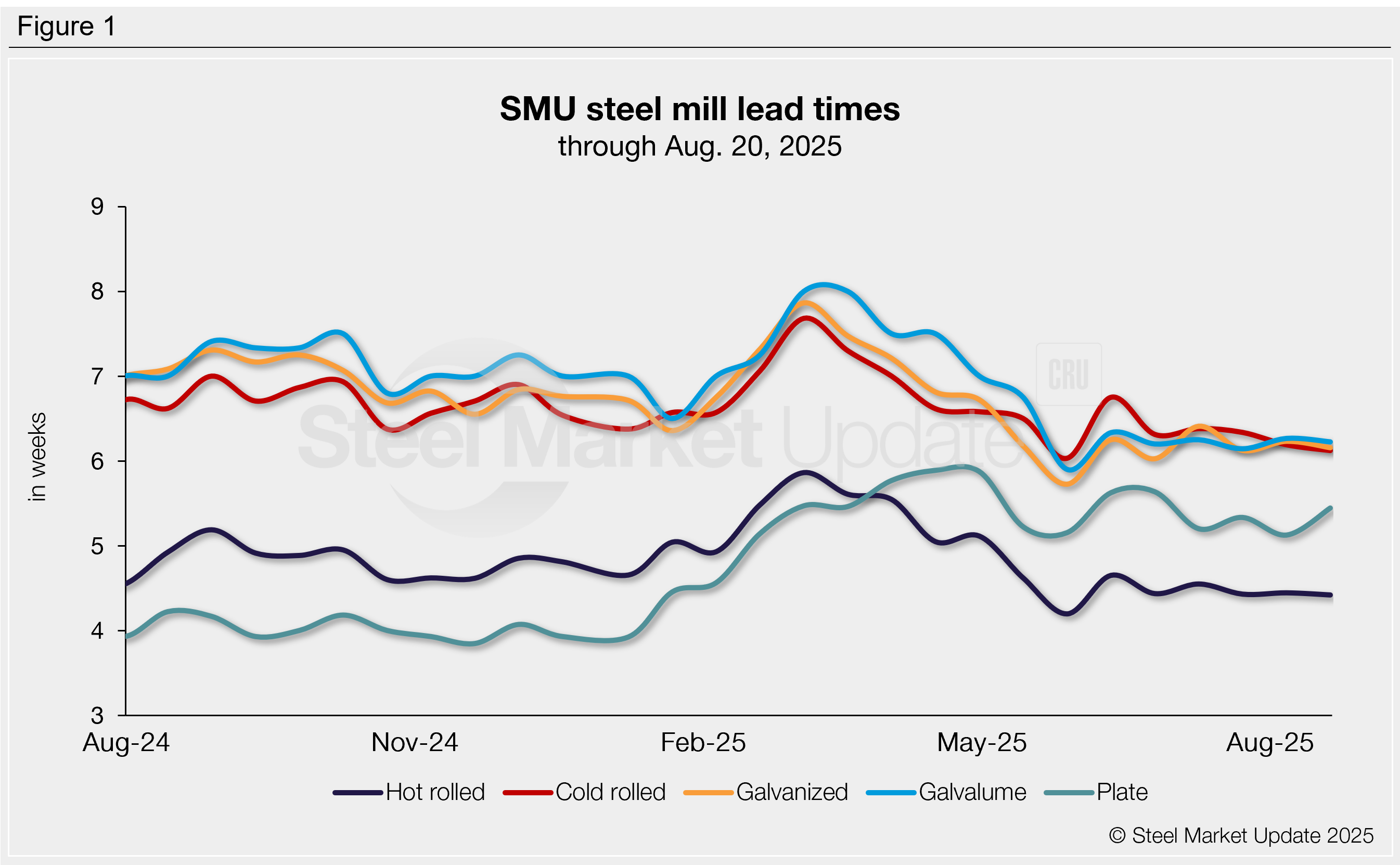

According to steel buyers responding to our latest market survey, sheet and plate lead times held steady again this week, a soft-sideways trend we’ve seen since May. Production times for sheet products remain just above multi-year lows, while plate lead times edged up slightly.

For three months now, sheet lead times have hovered within a few days of those multi-year lows. Plate lead times have been roughly one week longer than the lower levels seen from this time last year through early 2025.

The average lead time for hot-rolled coil remains just under four and a half weeks. Cold-rolled and coated products are all in the lower six-week range. Plate is just under five and a half weeks.

Table 1 summarizes current lead times and recent changes by product (click to expand).

Compared to our previous market check, all five of our lead time ranges shifted this week:

- The longest hot rolled lead time considered in our range declined from seven weeks to six.

- The shortest cold rolled lead time considered decreased from five weeks to four, while the longest extended from eight weeks to nine.

- The longest galvanized lead time considered rose from eight weeks to nine.

- The shortest Galvalume lead time considered declined from five weeks to four.

- The shortest plate lead time considered in our range decreased from four weeks to three.

Buyers predict more stability

Over half of buyers (62%) anticipate lead times will hold steady over the next two months, down from 71% two weeks ago. Among the rest, 28% believe lead times will extend (up from 21%), and the remaining 10% expect further contractions (up from 7%).

Here are some of the comments we collected:

“Domestic lead times are already short, and we think they’ll only contract more from here.”

“Can’t get much shorter than now, but I doubt without outages they will extend much.”

“I think lead times are so short that there’s more room to increase than decrease, and eventually I expect demand to pick up.”

“They will extend due to seasonal maintenance outages and an uptick in demand toward late Q4.”

“I think come November, order book lead times will begin to extend with low import volume incoming.”

“They are just starting to extend, flat to up until then, assuming we have a rate drop.”

“I see a turnaround starting about October.”

Trends

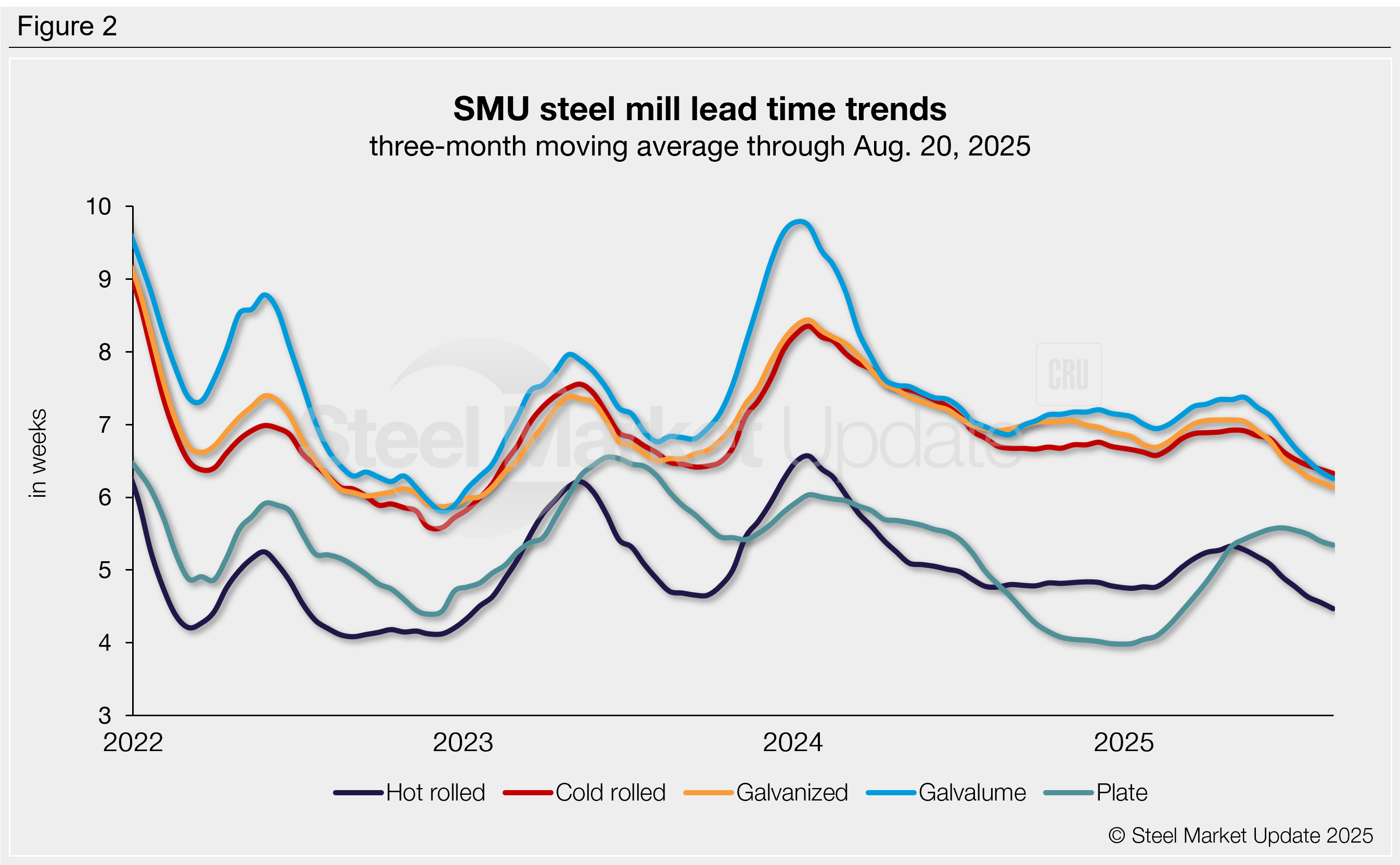

Lead times can be calculated on a three-month moving average (3MMA) basis to highlight broader trends (Figure 2). All four of the sheet product 3MMAs declined for the eighth survey in a row, and plate declined for the fourth.

Average lead times by product across the last three months were: hot rolled at 4.5 weeks, cold rolled at 6.3 weeks, galvanized at 6.1 weeks, Galvalume at 6.3 weeks, and plate at 5.3 weeks.

Note: These lead times are based on the average from manufacturers and steel service centers participating in this week’s SMU market trends analysis survey. SMU measures lead times as the time it takes from when an order is placed with the mill to when it is processed and ready for shipping, not including delivery time to the buyer. Our lead times do not predict what any individual may get from any specific mill supplier. Consult your mill rep for actual lead times. To see an interactive history of our steel mill lead times data, visit our website. If you’d like to participate in our survey, contact us at info@steelmarketupdate.com.