Market Data

September 23, 2025

SMU Price Ranges: Sheet and plate flat or down as hopes of rebound meet 'blah' demand

Written by Brett Linton & Michael Cowden

Sheet and plate prices were flat or lower this week as less discounting from domestic mills was offset by few signs of an anticipated rebound in demand.

HR and CR

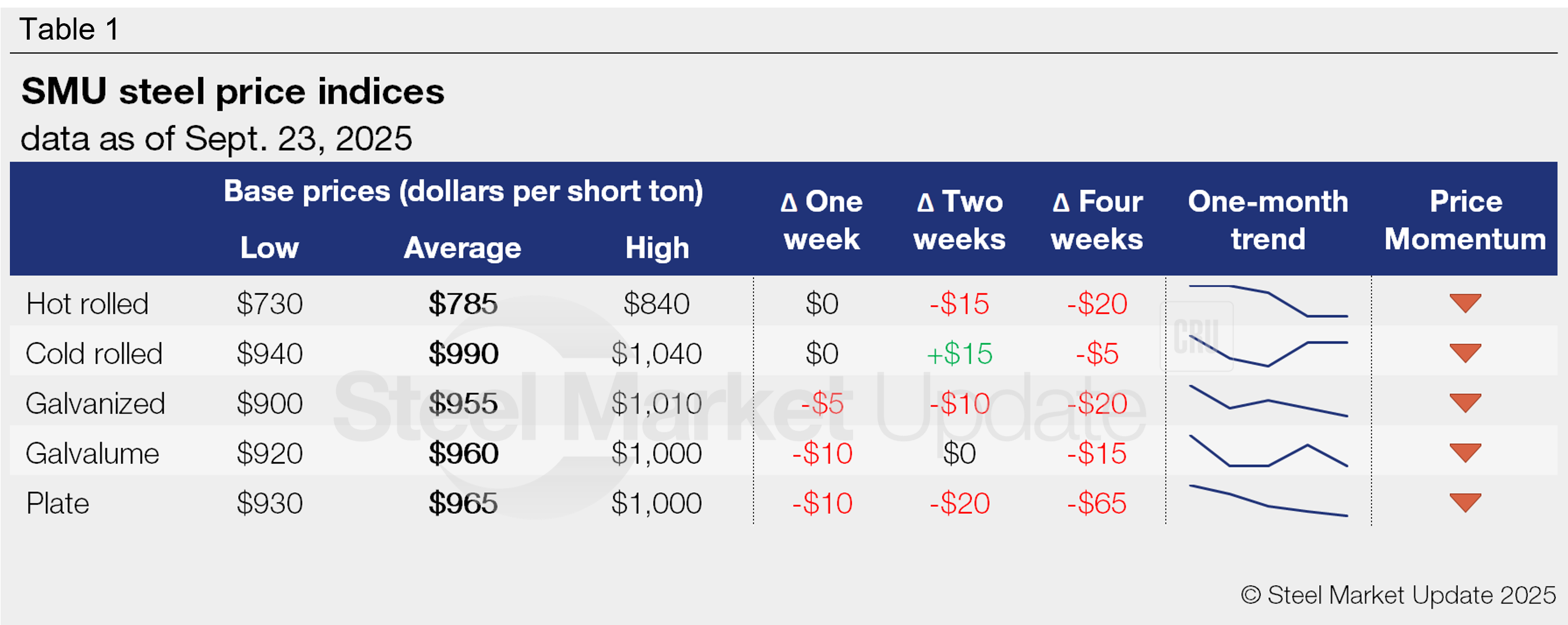

SMU’s hot-rolled coil price was unchanged from last week at $785 per short ton (st) on average. Our cold-rolled coil price was also flat week over week at $990/st on average.

On the hot-rolled side, the low end or our range increased to $730/st, up from $720/st last week. The modest uptick came as Canadian producers that had been offering material in the low $700s/st told customers they would halt or scale back such offers in November and December – and perhaps into 2026.

Such prices had been inclusive freight and Section 232 tariffs of 50%, which suggested an fob mill price in the mid-$400s/st – something that had created grumbling among US mills about potential dumping.

The Canadian offers had influenced the low end of US prices. But even with Canadian pricing likely having less impact going forward, certain US mills continued to offer HR in the mid/low $700s for larger buyers – in some cases because they still have October tons available and in other instances because automotive bookings might have come in lower than forecast.

A similar dynamic played out in the cold-rolled coil.

Coated and plate

On the coated side, SMU’s base price for galvanized product stands at $955/st on average, down $5/st from a week ago. And our Galvalume base price is at $960/st on average, $10/st lower than last week.

The declines come as US mills have struggled to maintain the $200/st spread between HR and coated base prices that had characterized much of the post-pandemic market. That $200/st spread has compressed amid increased domestic capacity and lackluster demand.

Plate also slipped $10/st vs. last week and now stands at $965/st on average.

Market commentary

Market participants generally said they had seen an uptick in inquiries. But most said they hadn’t seen orders rise in tandem. And service center sources expressed frustrations that their competitors continued to lower prices to protect market share – and said they had little choice but to do the same in a weak market.

Industry sources remain optimistic that prices should improve in Q4 and into 2026 on lower imports, lower inventories, and mill outages. But several said they had expected to see that uptick to occur by now – and that they’re growing increasingly concerned about demand.

What steel buyers are saying

“I think we’re closer to a firmer bottom. There are at least less bad actors willing to take low numbers.”

“It’s just blah. We were hoping for an uptick. And we’re just not seeing it. But it’s not awful. It’s just kind of mediocre.”

“Demand remains very muted. But the mills seem to have hit their bottom. Less import is coming in. Inventories are getting low. And outages are coming up – so the mills are in the driver’s seat. We might even see an increase.”

“Everyone is asking for pricing because they want to see where the numbers are. But I don’t see too many purchase orders being written. I’m looking for something to happen to make some excitement in the marketplace. But I don’t know. … I’m just not seeing it.”

SMU’s price momentum indicator remains at lower on both sheet and plate, signaling prices are expected ease in the short term.

Refer to Table 1 (click to enlarge) for our latest price indices and trends.

Hot-rolled coil

The SMU price range is $730–840/st, averaging $785/st FOB mill, east of the Rockies. The lower end of our range is up $10/st w/w, while the top end is down $10/st. Our overall average is unchanged w/w. Our price momentum indicator for hot-rolled steel remains at lower, meaning we expect prices to decline over the next 30 days.

Hot-rolled lead times range from 3–6 weeks, averaging 4.6 weeks as of our Sept. 18 market survey.

Cold-rolled coil

The SMU price range is $940–1,040/st, averaging $990/st FOB mill, east of the Rockies. The lower end of our range is up $20/st w/w, while the top end is down $20/st. Our overall average is unchanged w/w. Our price momentum indicator for cold-rolled remains lower, meaning we expect prices to decline over the next 30 days.

Cold-rolled lead times range from 5–8 weeks, averaging 6.4 weeks through our latest survey.

Galvanized coil

The SMU price range is $900–1,010/st, averaging $955/st FOB mill, east of the Rockies. The lower end of our range is unchanged w/w, while the top end is down $10/st. Our overall average is down $5/st w/w. Our price momentum indicator for galvanized steel remains lower, meaning we expect prices to decline over the next 30 days

Galvanized .060” G90 benchmark: SMU price range is $978–1,088/st, averaging $1,033/st FOB mill, east of the Rockies.

Galvanized lead times range from 5–8 weeks, averaging 6.4 weeks through our latest survey.

Galvalume coil

The SMU price range is $920–1,000/st, averaging $960/st FOB mill, east of the Rockies. The lower end of our range is unchanged w/w, while the top end is down $20/st. Our overall average is down $10/st w/w. Our price momentum indicator for Galvalume steel remains lower, meaning we expect prices to decline over the next 30 days.

Galvalume .0142” AZ50, grade 80 benchmark: SMU price range is $1,274–1,354/st, averaging $1,314/st FOB mill, east of the Rockies.

Galvalume lead times range from 5–8 weeks, averaging 6.9 weeks through our latest survey.

Plate

The SMU price range is $930–1,000/st, averaging $965/st FOB mill. The lower end of our range is down $20/st w/w, while the top end is unchanged. Our overall average is down $10/st w/w. Our price momentum indicator for plate remains lower, meaning we expect prices to decline over the next 30 days.

Plate lead times range from 3–7 weeks, averaging 5.1 weeks through our latest survey.

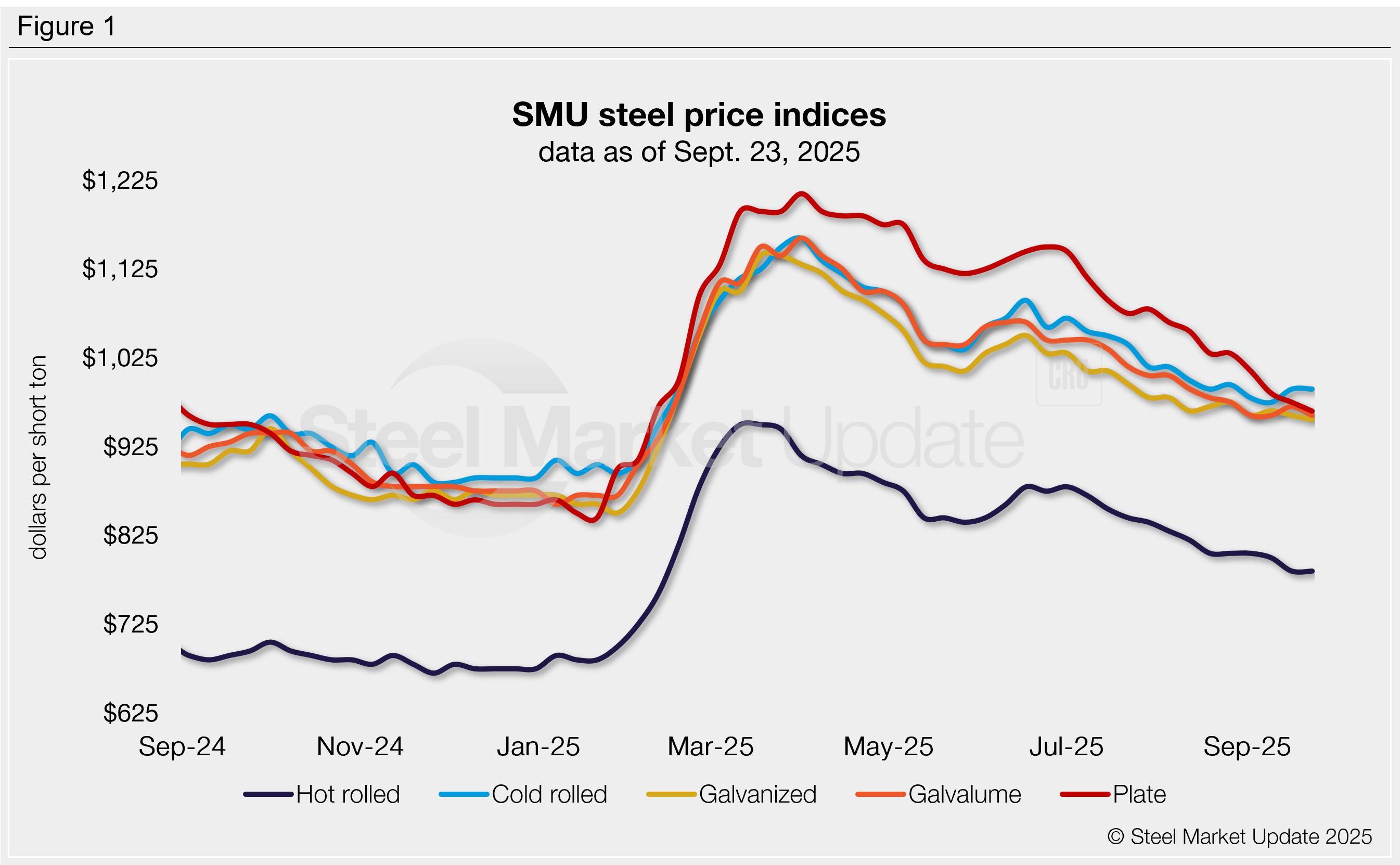

SMU note: The graphic above shows a history of our hot rolled, cold rolled, galvanized, Galvalume, and plate prices. This data is also available on our website with our interactive pricing tool. If you need help navigating the site or logging in, contact us at info@steelmarketupdate.com.

Brett Linton

Read more from Brett Linton