Analysis

October 15, 2025

September service center shipments and inventories report

Written by Estelle Tran

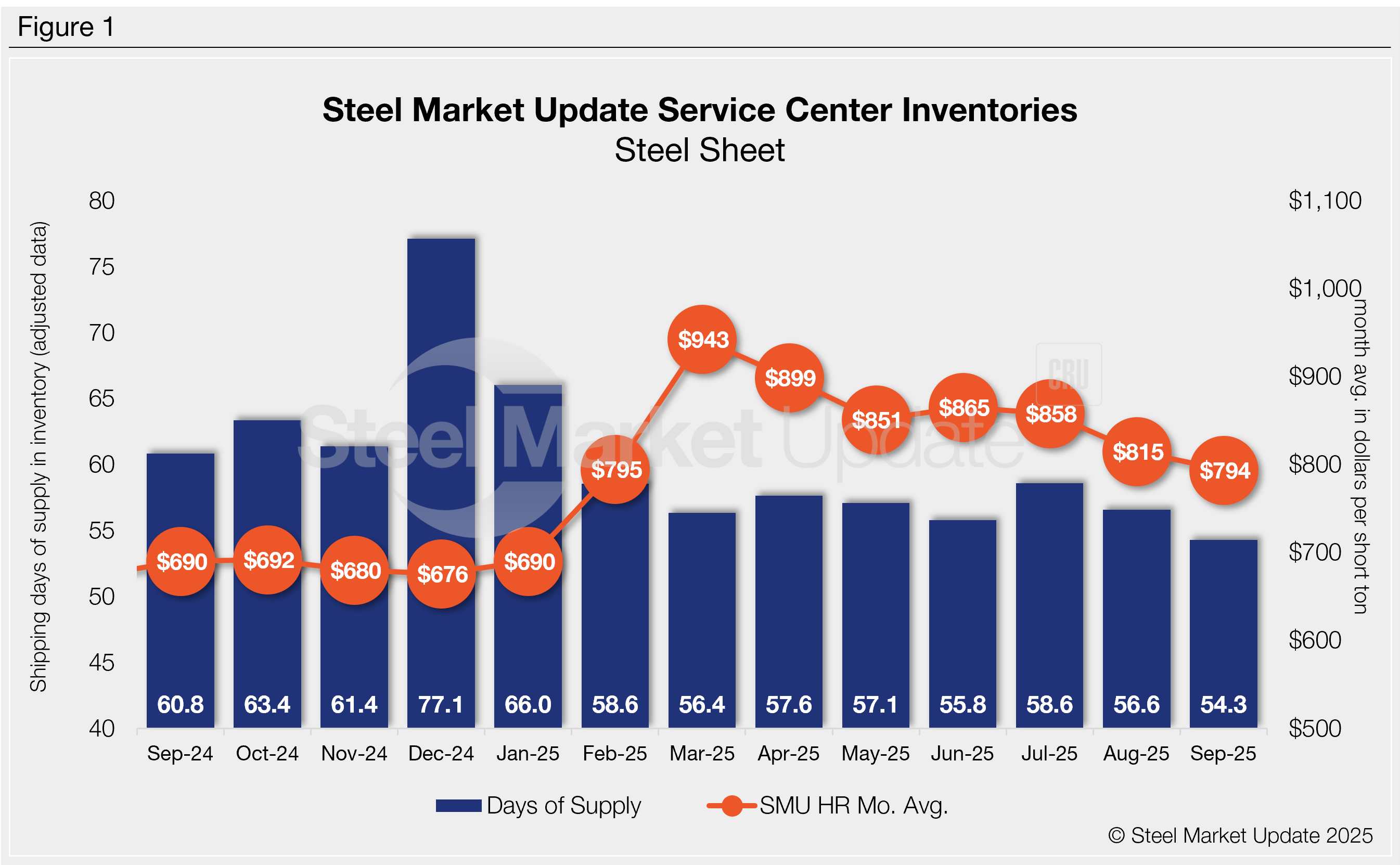

Flat rolled = 54.3 shipping days of supply

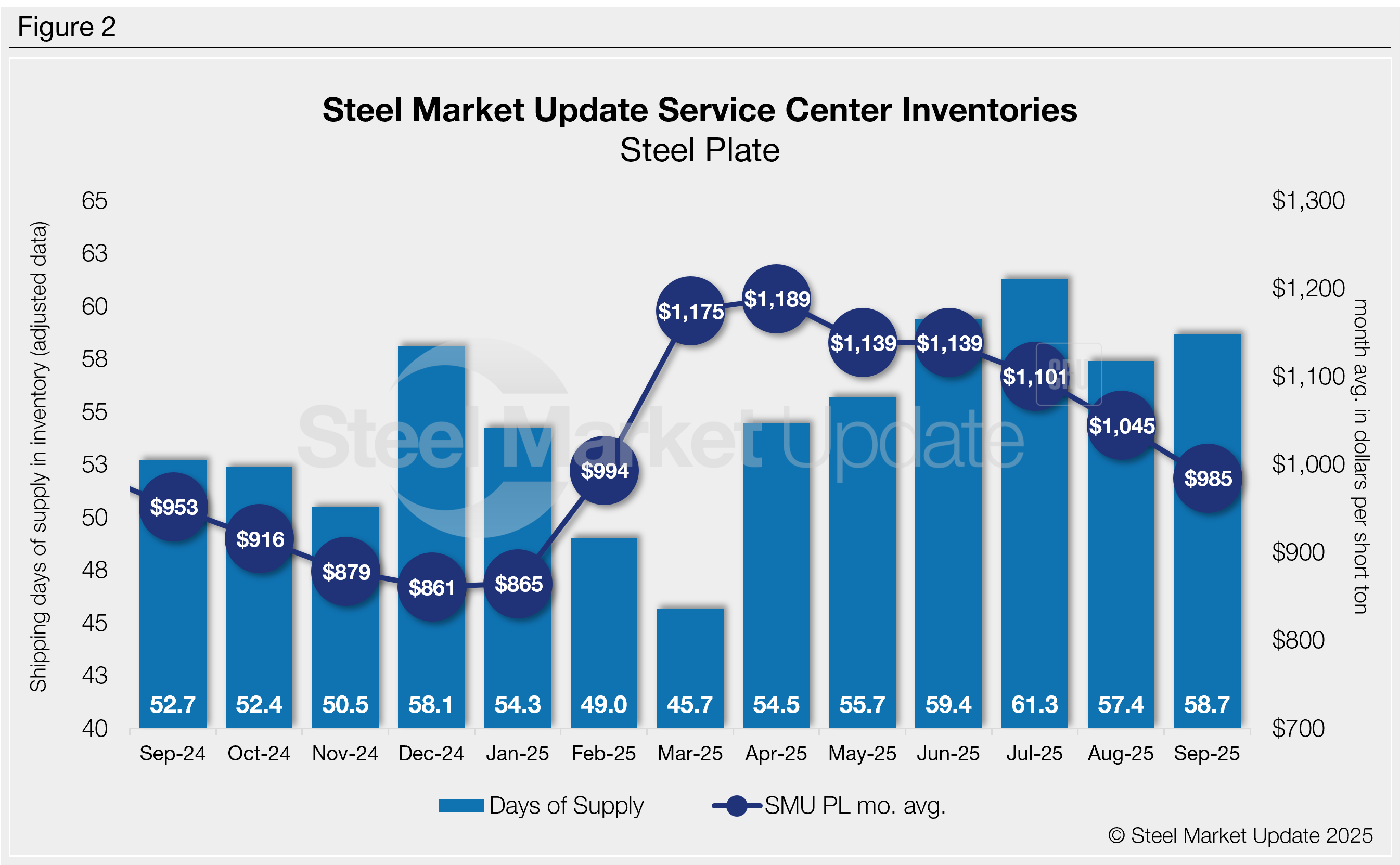

Plate = 58.7 shipping days of supply

Flat rolled

US service centers flat-rolled steel supply edged lower for the second consecutive month, reaching 54.3 shipping days of supply on an adjusted basis at the end of September, according to SMU data. Flat roll supply is down from 56.6 shipping days in August and 60.8 shipping days in September 2024.

Flat roll inventories represented 2.59 months of supply in September, down from 2.7 months in August and 3.04 months in September of last year. The m/m drop in inventories has helped to support prices, though demand remains subdued.

Shipments in September slowed by 0.4% m/m. Despite the moderate shipment levels, the reduction in inventories put service center supply in balance with demand.

The latest SMU survey, published Oct. 3, found 58% of service centers were releasing less steel compared to one year ago, while 26% were releasing the same amount of steel. With tepid demand and relatively short lead times that have only recently started to extend, service centers have been cautious about placing new orders.

At the end of September, service centers’ shipping days of supply on order was the lowest level captured since March 2020. The latest SMU survey showed hot-rolled coil lead times at 4.74 weeks, up from 4.45 weeks a month ago.

Additional domestic capacity has helped to keep lead times short, though buying interest has also been limited. According to the latest SMU survey, 64% of service centers were maintaining inventory, while 23% were reducing inventory and 13% were building inventory.

The drop in flat roll supply and low level of material on order could result in October inventories falling too low. However, if demand continues to disappoint, inventories should remain in balance. The lack of material on order could be a sign that fall demand still has not picked up – a concerning sign heading into the slower shipping months of November and December. Also, the data could indicate that the recent flurry of opportunistic, large-volume deals was not as substantial as perceived.

Plate

US service center plate inventories edged higher in September, though shipments picked up, according to SMU data. At the end of September, service centers held 58.7 shipping days of supply, up from 57.4 in August. Plate supply in September represented 2.79 months of supply, up from 2.73 months in August.

September plate supply is significantly higher than year-ago levels, when service centers carried 52.7 days of supply or 2.64 months of supply. Though the latest inventory levels are slightly elevated, they are not overly high given the expectation of stable shipments through November.

Material on order fell further in September, and the shipping days of supply on order reached the lowest level since March 2020. Service centers do not need to carry as much inventory because of additional domestic capacity. Plate mill lead times remain short at 5.15 weeks, according to the latest SMU survey.

Service center demand has not picked up materially after the summer, though market contacts have noted that more project work has gone out to bid. This may pick up even more as mills push through price increases and the market starts to look toward next year. While inventories are more than sufficient to meet current demand, service centers may need to increase their orders for Q1, given the low level of material on order at the end of September.