Analysis

October 17, 2025

CRU: Soft demand weighs on sheet imports into the US

Written by Brett Reed & Diego Giangreco

This news item was first published by CRU. To learn about CRU’s global commodities research and analysis services, visit www.crugroup.com.

US domestic sheet prices have remained rangebound in recent weeks as supply tightness met weak demand. Demand for steel produced in the US increased among some Mexican industrial buyers seeking to avoid the 50% steel tariffs when re-exporting those products back to the US. Meanwhile, tariffs continued to limit imports of long steel products into the US, supporting higher domestic prices for some products.

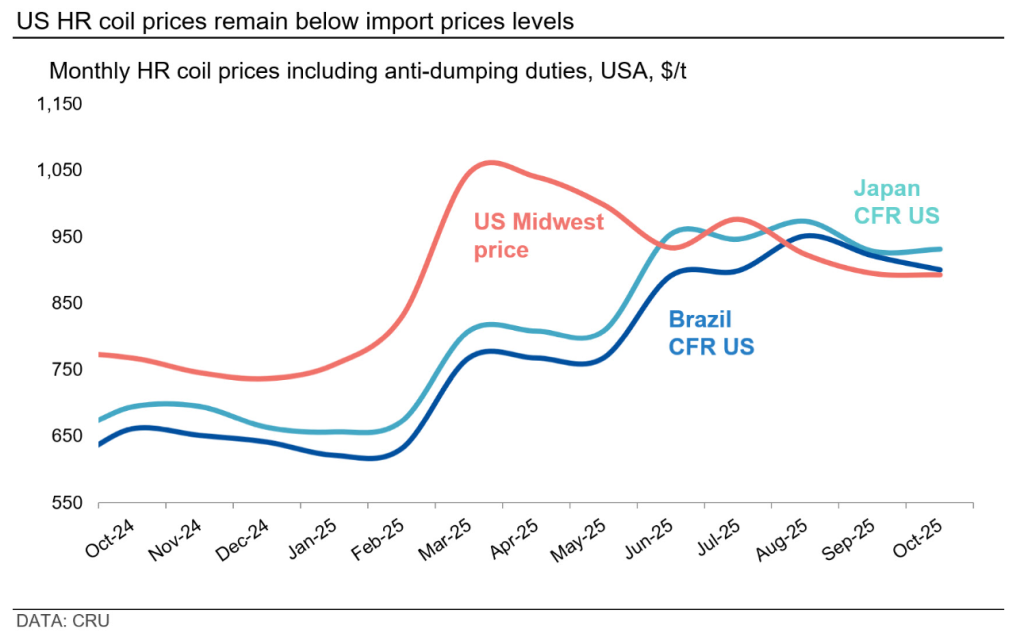

US HR coil prices gain stability, but demand remains weak

US domestic HR coil prices have gained stability in recent weeks, supported by temporary supply tightness due to scheduled maintenance outages. We had been expecting sheet prices to rise incrementally due to these supply issues; however, weak demand and the ramp-up of new domestic capacity have kept pressure on sheet prices. This environment of weak demand has come alongside falling levels of flat-rolled imports.

US sheet prices remained below landed import prices from key markets (see chart). Although aggressive import offers from Canada and Vietnam continued, US buyers prioritized maintaining lean inventories amid soft demand and the slower holiday season.

As for long products, US import volumes fell 49% y/y in September, according to US Department of Commerce census and license data. Rebar import licenses dropped to 9,500 metric tons, down 73% m/m and 75% y/y. Wire rod import licenses fell to 29,000 mt, down 73% m/m and 58% y/y. Tariffs have kept upward pressure on domestic prices for HC wire rod and tyre cord, which have limited domestic production and require imports to meet demand. There has been an increase in domestic rebar production, replacing a portion of lost import volumes while also limiting price gains.

In Mexico, the government continues to work to reduce non-compliant imports, prompting buyers to opt for domestic supply over imports. Some industrial buyers are importing steel from the US to produce goods and avoid the 50% steel tariffs when re-exporting those products back to the US. As a result, sheet imports into Mexico for January-July 2025 increased slightly by 1.2% y/y, with volumes from the US rising while those from other origins declined.

Brazilian slab export prices remain stable m/m

Brazilian slab export prices remained stable m/m in October at $485/mt FOB Brazil, as downward pressure continued due to competition from low-priced Asian offers. In terms of trade, export volumes decreased by 1.7% m/m in September but were up by 13% y/y. Export volumes for the January-September period are up by 10% y/y. The main export markets were the US and Mexico, which accounted for 85% of total exports, while the remaining volumes went to Poland and Argentina. ArcelorMittal Mexico had an incident in its DRI production in late August, which impacted its slab production, and as a result, the company might need to source imported slab to partially offset the shortfall.

Please contact CRU if you’d like to know more about analysis and consulting services.