Analysis

November 2, 2025

Final Thoughts

Written by Michael Cowden

Most steel buyers think steel prices will continue to rise into 2026. But they don’t see the kind of big gains that have characterized past market upturns, according to the results of SMU’s latest steel market survey.

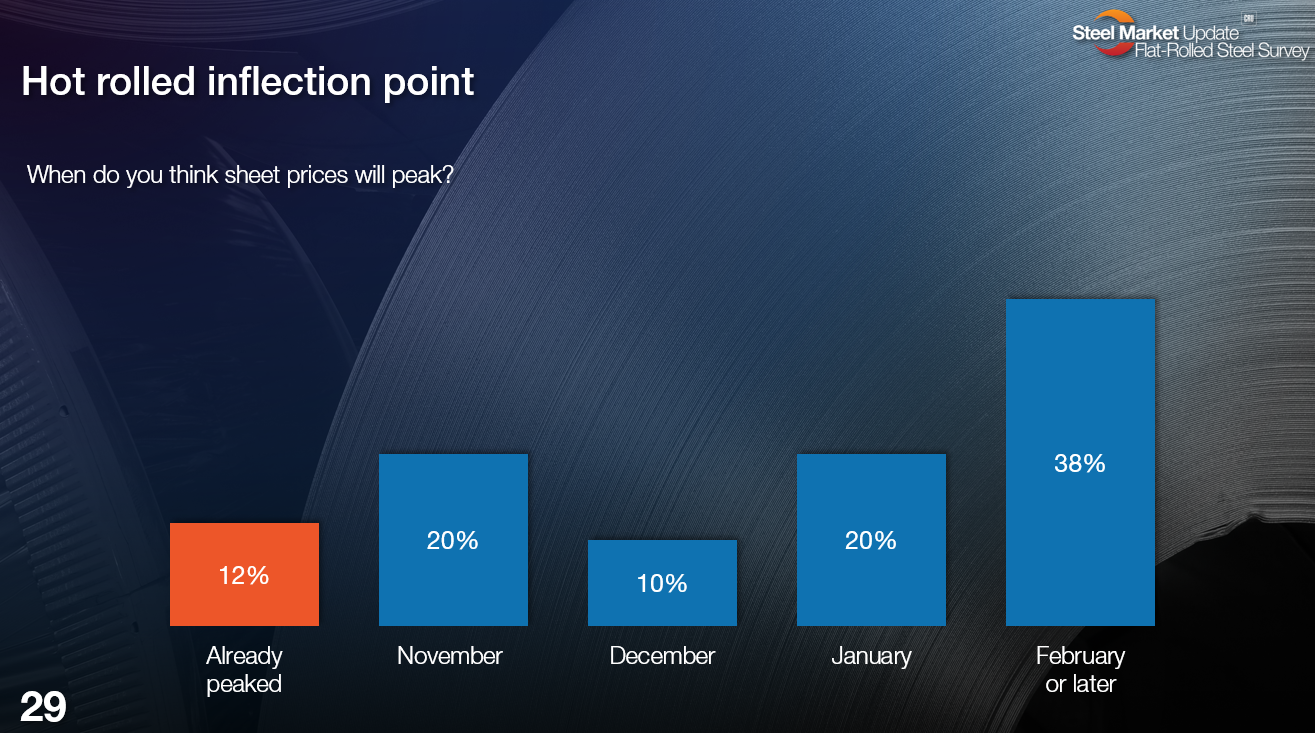

When will prices peak?

Let’s start with when people think sheet prices will peak. (Editor’s note: You can expand the graphs below by clicking on them. The page numbers correspond to the full survey slide deck. Our premium subscribers can access that deck here.)

As you can see, most people (58% of survey respondents) think sheet prices won’t peak until Q1. But a significant minority think that prices have already peaked (12%), will peak later this month (20%), or in December (10%).

Below is what some of them had to say:

Already peaked

“We would disagree with the ‘sheet prices appear to have turned’ narrative. We don’t see these hikes sticking. The upside is extremely limited. And demand is just awful.”

November

“Demand is not there, and neither are raw material prices – namely, scrap.”

“Even with demand picking up lately, I still don’t see enough demand to support any significant price increases.”

“Mills are trying to get one more raise prior to year end. But demand is not there to support it.”

“Dead cat bounce, and not much bounce.”

“Tariff impact is affecting pricing, but demand is low.”

December

“The market is very weak. And there are some cheap numbers floating out there with mills.”

January

“Short-term demand and inventory restocking will cool by mid-January.”

“New Year’s optimism.”

“It would seem like mill outages and increased contract buying can keep prices elevated into the New Year, before buyers are able to challenge again.”

February

“We have just bottomed. I think there is a little runway for some upward movement as we move through year-end.”

“Domestic steel demand increases will drive scrap and prices higher for a multi-month period.”

“If the push by mills is starting now, I expect a 90-day mini-cycle that will run out of steam by late Jan/early Feb.”

“Seems to be the way the cycle runs.”

“They will go up for a while due to service center restocking and end user restocking.”

“They will start to rise steadily in December, after contracts are wrapped up.”

“Demand is not there until then.”

“Bottom out towards Nov./Dec. Then increase attempts. And then depends on market response in January 2026. That will determine the peak.”

One thing you’ll note from the quotes above is this: Most people don’t see a big upswing in prices. There is a lot of talk about the timing of a restock or of a mini-cycle. But many note that demand remains weak, despite talk of a data center/AI-driven boom.

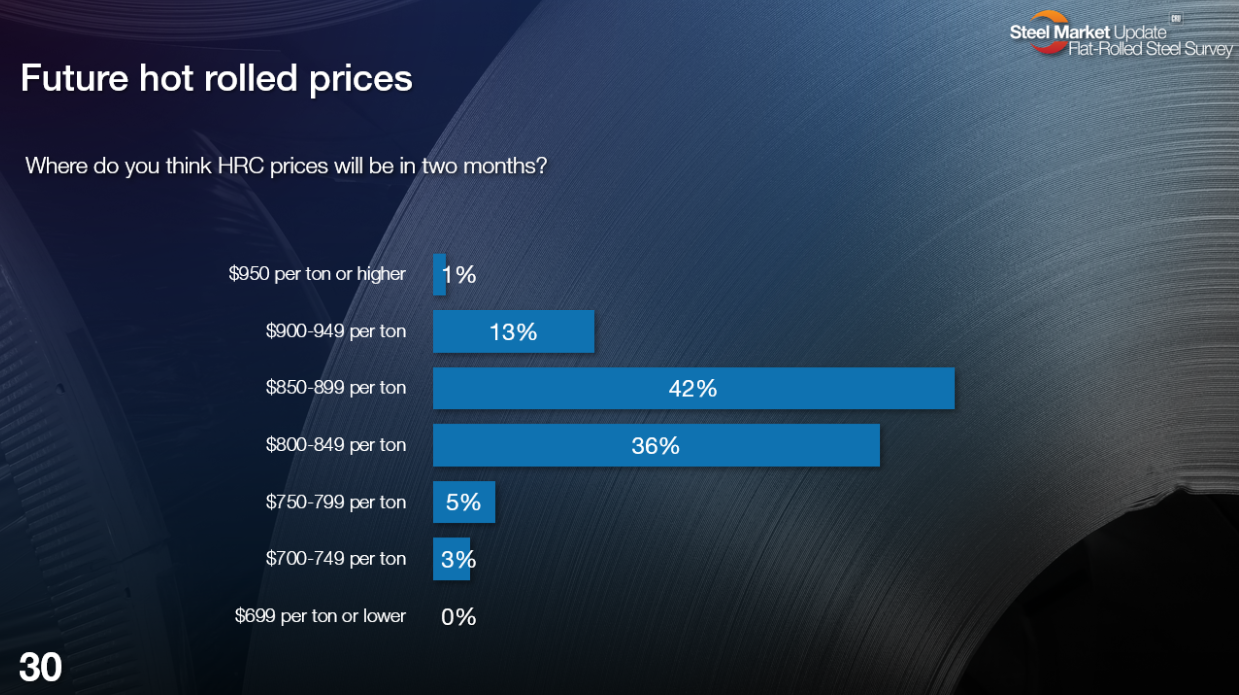

Where will HR prices be to start 2026?

The chart below shows where people think hot-rolled coil prices will be in two months – so at the start of 2026. (Note that SMU’s HR price currently stands at $820/st on average. We will update prices on Tuesday.)

Most people (78%) see HR prices beginning the year in the $800s/st. Only a few (14%) see HR prices breaking into the $900s/st. And even fewer (8%) see prices falling into the $700s/st again.

Here is what survey respondents had to say:

$700-749

“Auto slowdown coming.”

“We are anticipating prices actually fall over the next few months. As you can see, we are pretty bearish in our macro forecasts.”

$750-799

“This administration can’t stop setting out rakes and then stepping on them. That bleeds into everything else – whether Canada, China, or a government shutdown. Where is the positive news that will inspire confidence and feed growth?”

“It goes up every January. But the economy is too weak for it to be there long.”

$800-849

“Several reasons that the mills will push through increases: They can, prices have been stagnant for too long, planned outages, and scrap will tick up in December.”

“Scrap is cheap. Maybe things will pick up due to tariffs on Canada and Algoma being out of the US. But business is not robust enough.”

“Too much capacity/not enough demand to support much higher prices.”

“The market remains conservative within the current uncertain environment.”

“High capacity. Low demand. Cheap scrap.”

“Demand is still not there to support supply.”

“Still not enough volume to entice an increase.”

“No demand.”

“Mill shutdowns.”

$850-899

“The latest tariffs on Canada that are being threatened will further strain imports and create more strength in the US.”

“Tariff impact is affecting pricing, and mills are slowing production.”

“In line with recent cycles.”

“Futures.”

“There is political influence on steel as a commodity.”

“Low inventories.”

“Outages.”

“My hunch.”

$900-949

“Restocking and a short-term demand bump.”

“It will go up. $100-200/ ton. Why? No imports.”

“Could be higher. Prices tend to overcorrect, particularly on the way up. My forecast is tempered by modest to weak demand.”

$950 or higher

Well, it turns out the folks who think we’re going to $950/st or higher aren’t telling us why they think so.

Why so modest?

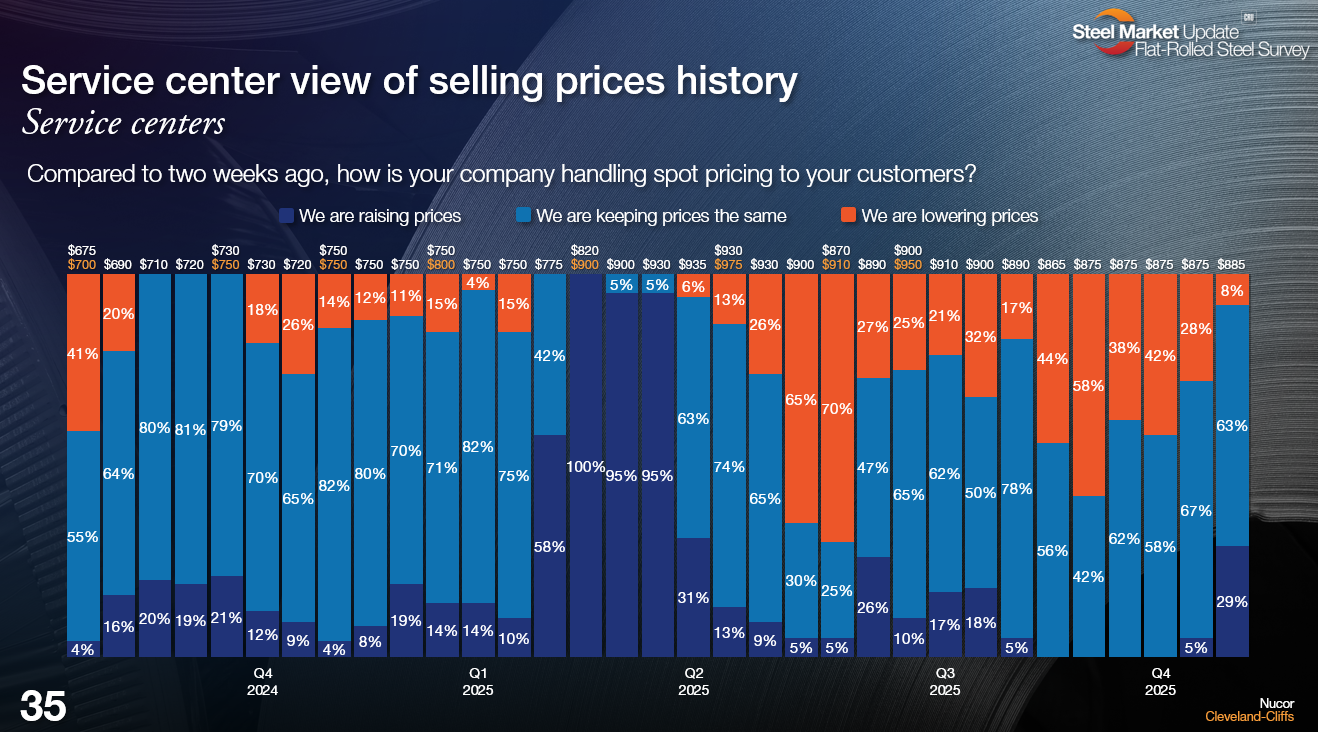

That people anticipate HR prices in the $800/st range probably comes as no surprise. As we noted last week, we’ve seen lead times inch up at the same time mills have become slightly less willing to negotiate lower prices – as one would expect after a round of price increases. Meanwhile, sentiment rose too.

Perhaps more importantly, the increases appear to be gaining hold along the supply chain in a way we haven’t seen since June, shortly after President Trump’s doubling of Section 232 tariffs went into effect.

The chart above is notable because it represents a clear shift from just a few weeks ago, before mills announced price increases. A significant number (29%) of service centers are raising prices along with mills, most (63%) are at least maintaining prices, and only a few (8%) continue to reduce prices.

That might not seem notable. But it’s actually the strongest reading we’ve seen for this data series since Q1, when the market soared higher as companies bought ahead of widely anticipated tariffs. It’s also a huge shift from the summer, when at times nearly 60% of service centers told us they were lowering prices.

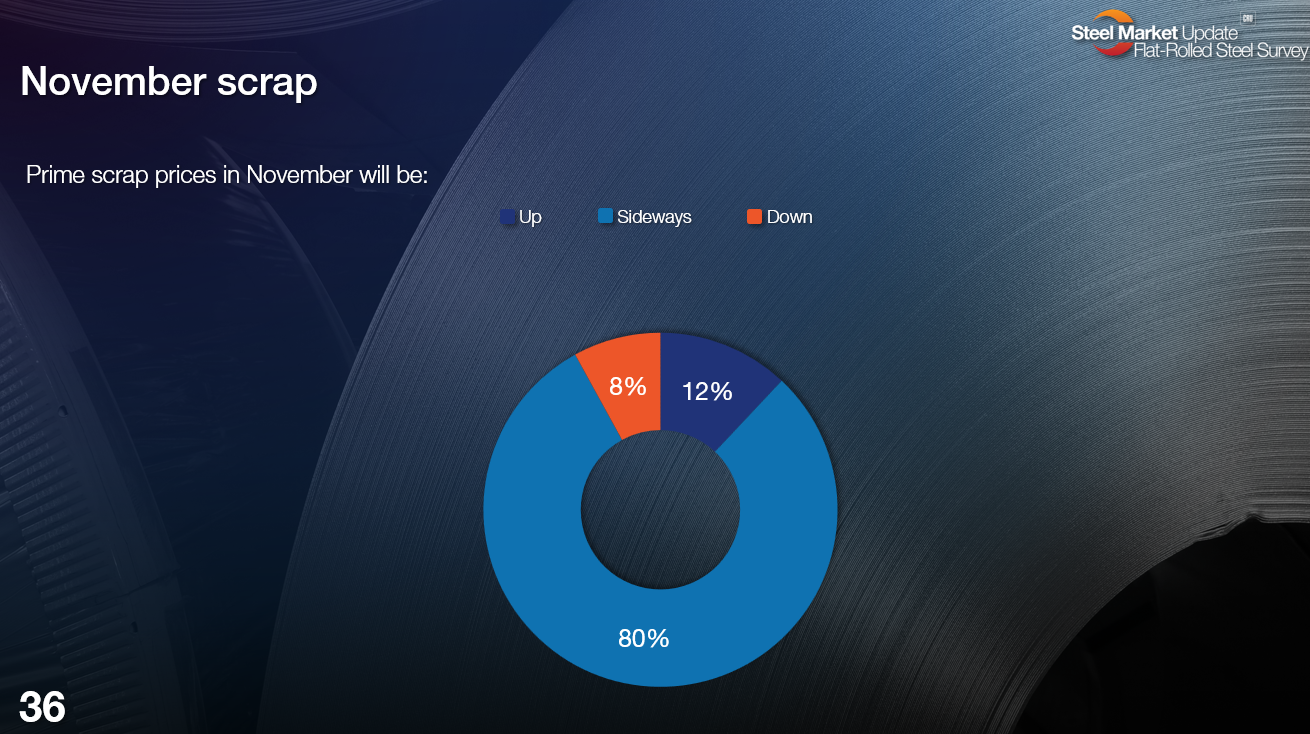

Why do so few people see prices getting into the $900s/st, a number even some typically bearish analysts have predicted?

It might be because most survey respondents (80%) think that prime scrap prices will be flat next month.

That’s not a surprise. And it’s in line with our reporting that scrap will probably be flat in November. But we’ve also noted that scrap typically rises in December and January. And so scrap prices should in theory provide support to higher prices late this year and into early 2026.

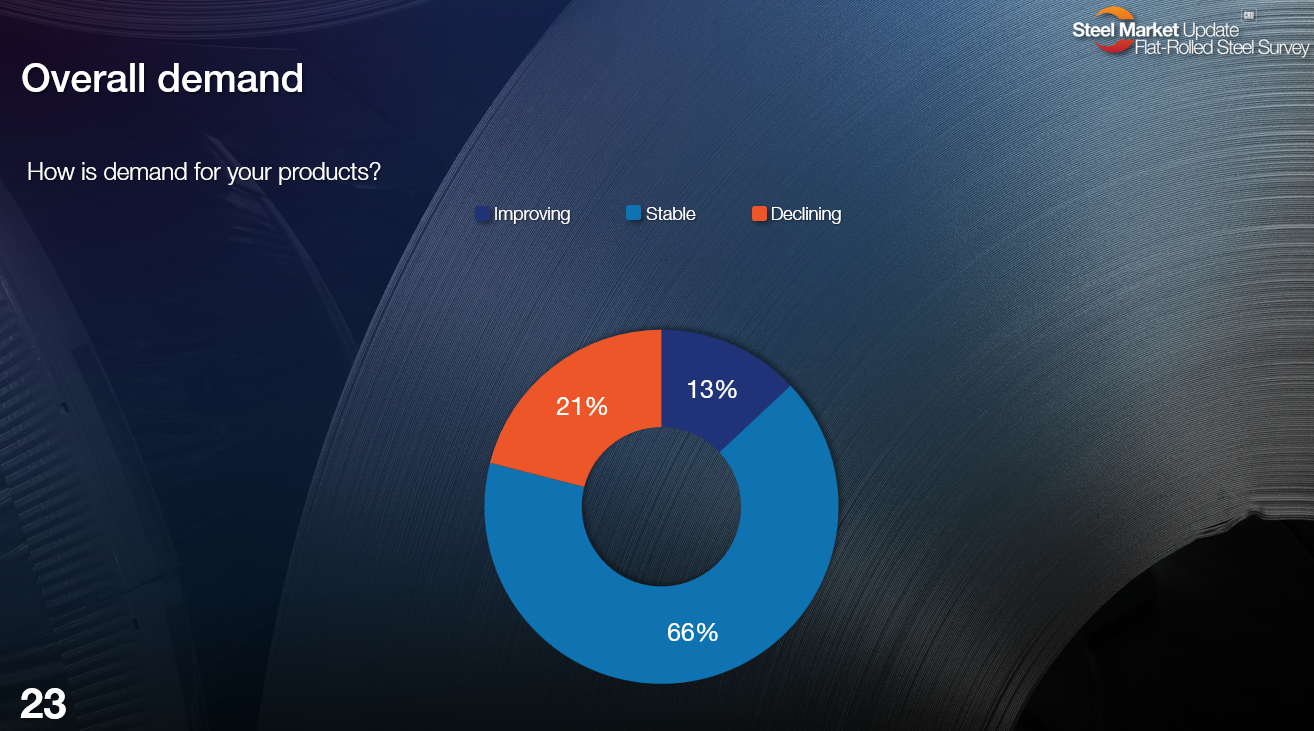

I think the bigger issue is that we haven’t seen any notable shifts in demand.

Approximately two-thirds of survey respondents say demand is stable. Only a few (13%) say it’s improving. And a significant minority (21%) say demand continues to decline. That read is in line with what we’ve seen since Q2, when Liberation Day in early April and subsequent Section 232s unleashed waves of confusion into the market.

In short, while both mills and service centers are trying to adjust prices higher, there is little evidence of things changing on the demand side of the equation. Meanwhile, too many companies

One of the survey respondents above noted that he didn’t buy a narrative, pushed by some mills and larger buyers, about prices rising. A key part of that narrative is that lead times are into (or at least close to) 2026.

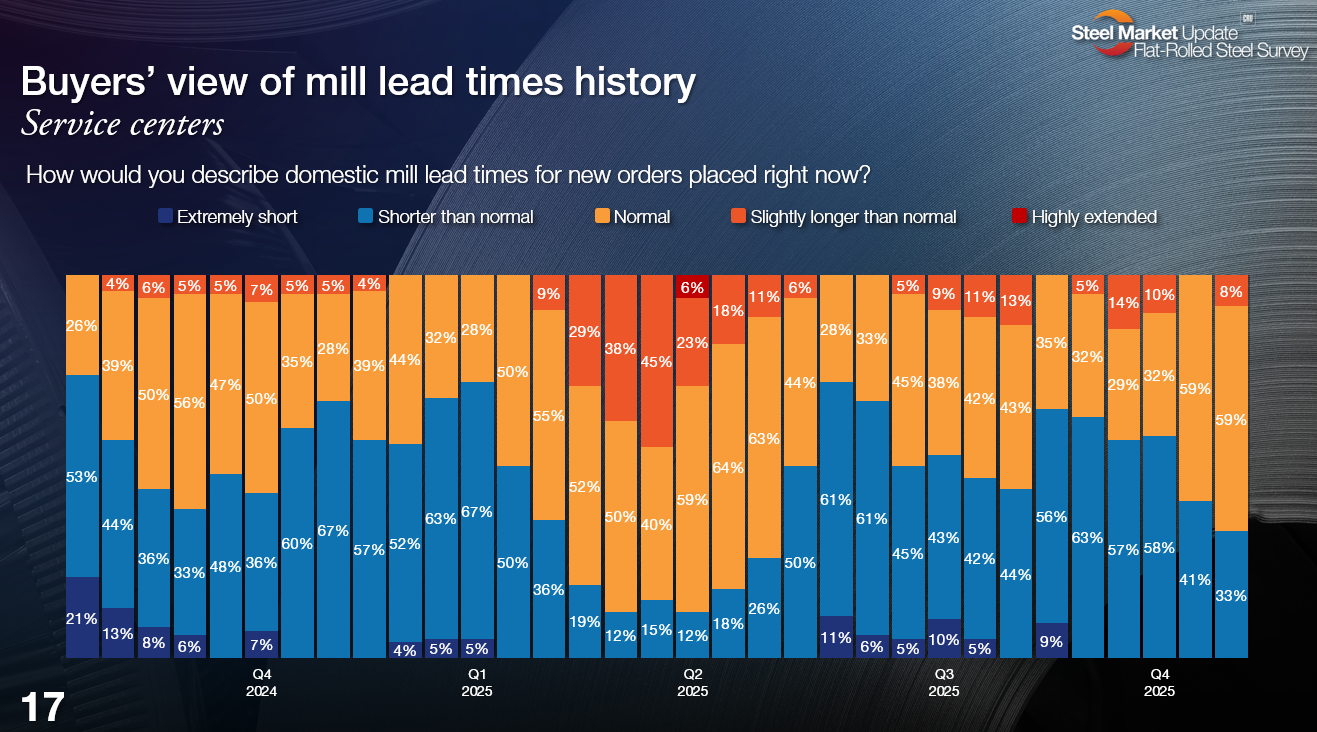

But most of the people we survey aren’t seeing evidence of that.

In fact, the main change, as far as our survey respondents see it, is that lead times gone from shorter than normal (blue bars) to normal (yellow bars). The chart above shows the results from service center respondents. Manufacturer respondents noted a similar trend.

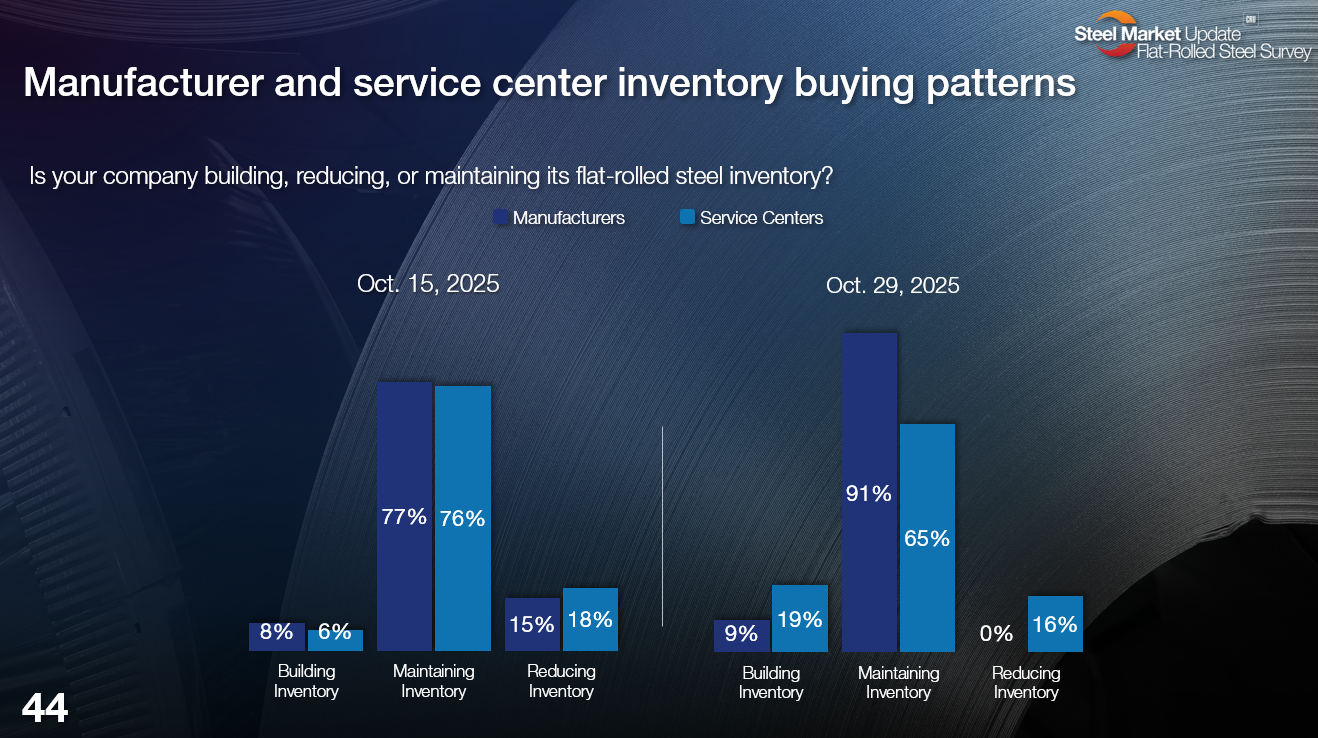

Maybe that could change? Some of our data indicates that a restock might be close.

Over the last month, for example, we’ve seen more manufacturers shift from reducing inventories to maintaining them. And we’ve seen a modest shift in service center behavior as well. Sure, most are still maintaining inventories. But more are building them now than was the case in early/mid-October.

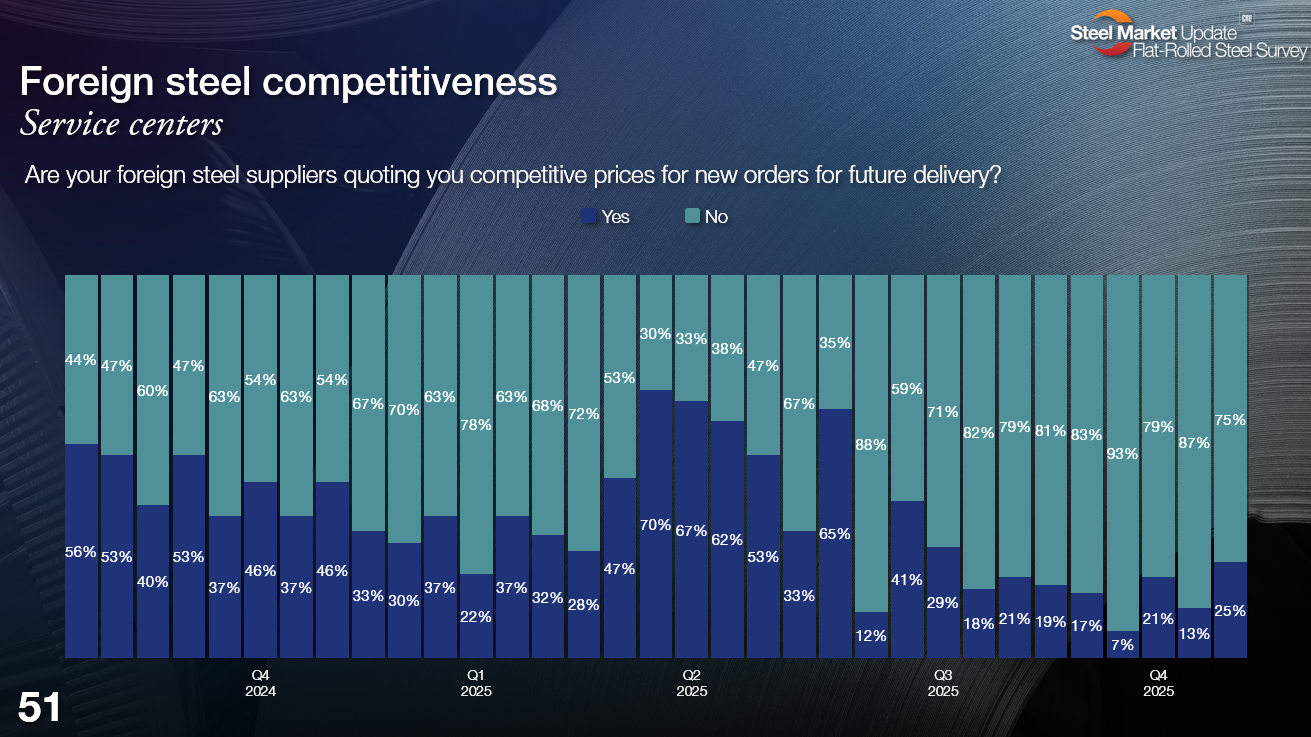

And while we don’t have government import data (because of the federal government shutdown), most survey participants continue to say that imports are not competitive.

That’s a trend we’ve seen since Q3 and the doubling of tariffs to 50% in June. Since then, I’m assuming that the import pipeline has run a lot drier. The question is probably less about new imports arrivals and more about how much material that was brought in earlier this year remains in inventory and contributing to an overhang. And, of course, the biggest question remains whether and when demand might improve.

Make your voice heard!

Does what we’re reporting from our survey match what you’re seeing in the market? Or do you see it differently? Let us know at info@steelmarketupdate.com. Also, if you’d like to make your voice heard, consider contributing to our survey. Ping us at the same email address, and we’ll get you signed up.

And to all of you who already participate, thanks for your input – we truly appreciate it.

Introducing a new, improved SMU website

I hope you’ve seen the notices we’ve been running about a new, improved SMU website coming to you on Monday morning. If you haven’t check out the article and FAQ here.

We’ll shift from the current site to the new one from approximately 4 am ET to 8 am ET on Monday. So, please excuse our dust then. And we hope you’ll find the new site a little more intuitive, a little easier to navigate, and, well, a little prettier than the old one.

Remember, too, that your login won’t change. Your subscription won’t change. And most of your bookmarks should continue to work. If you do run into trouble, just give us a shout at smu@crugroup.com. We’d be happy to hear your feedback.