Analysis

November 17, 2025

October service center shipments and inventories report

Written by David Schollaert

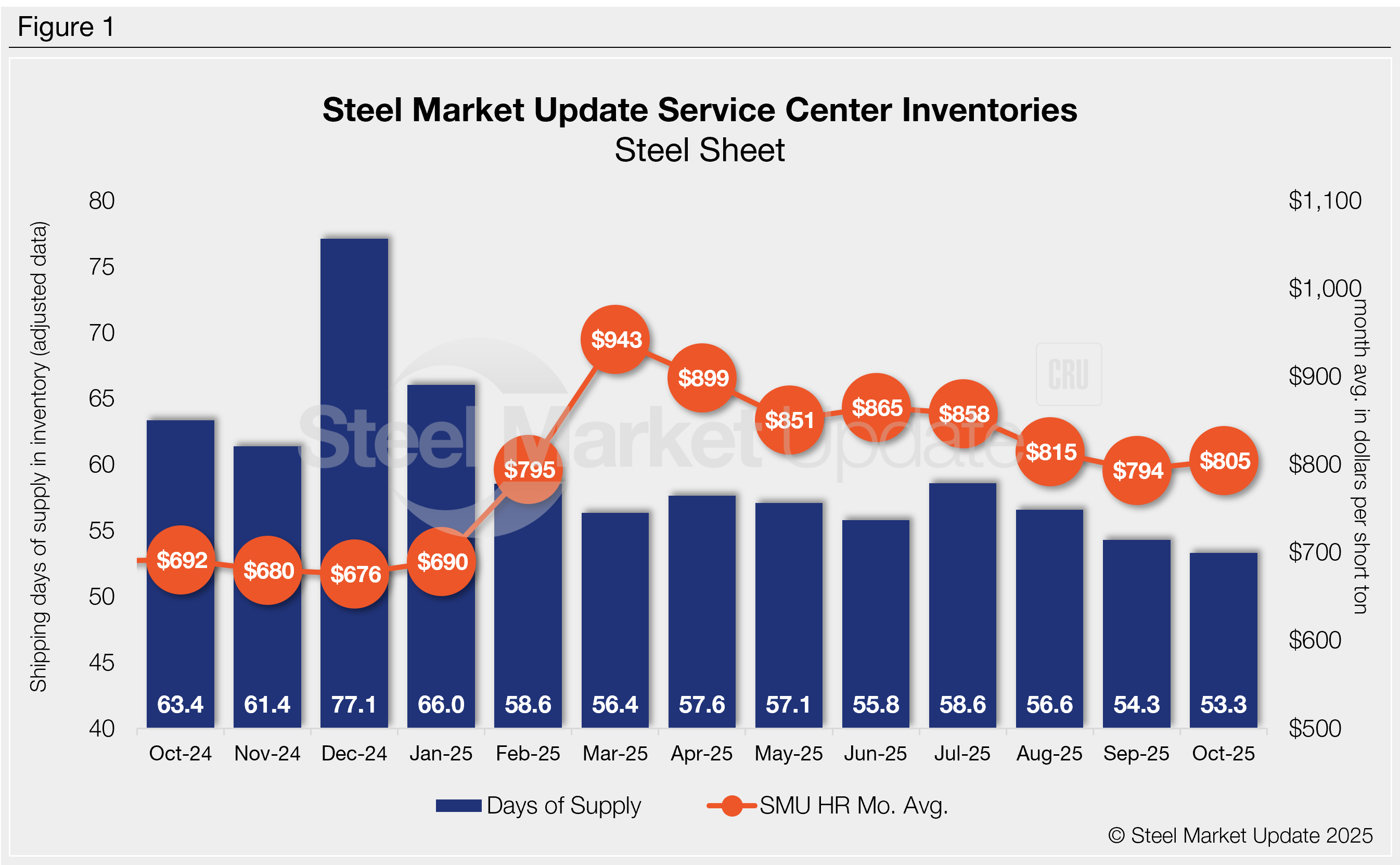

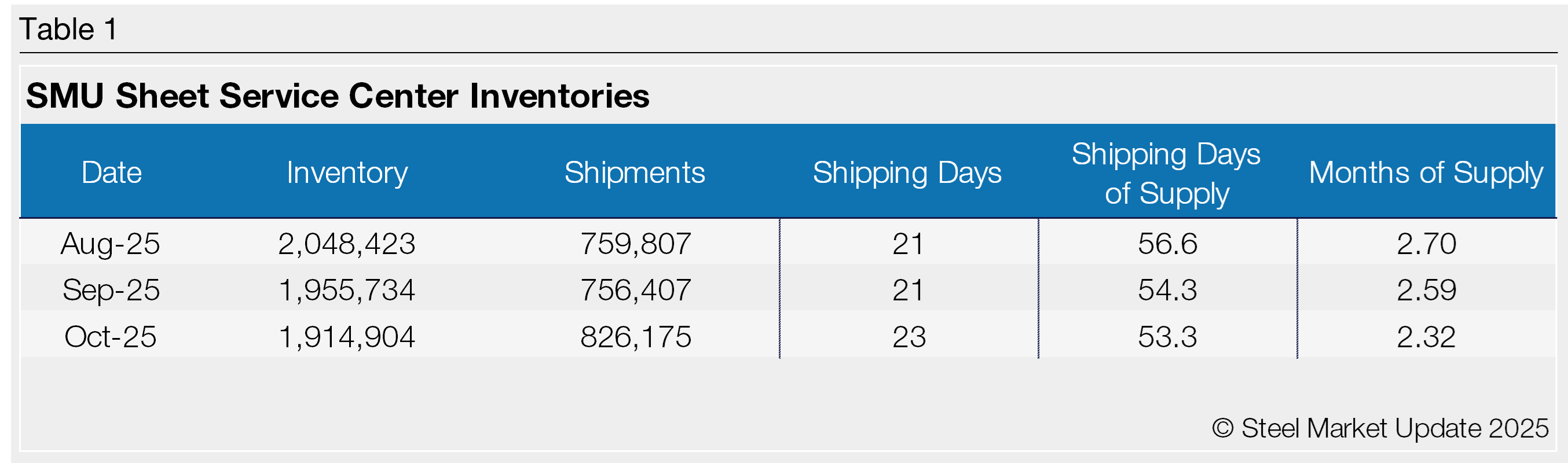

Flat rolled = 53.3 shipping days of supply

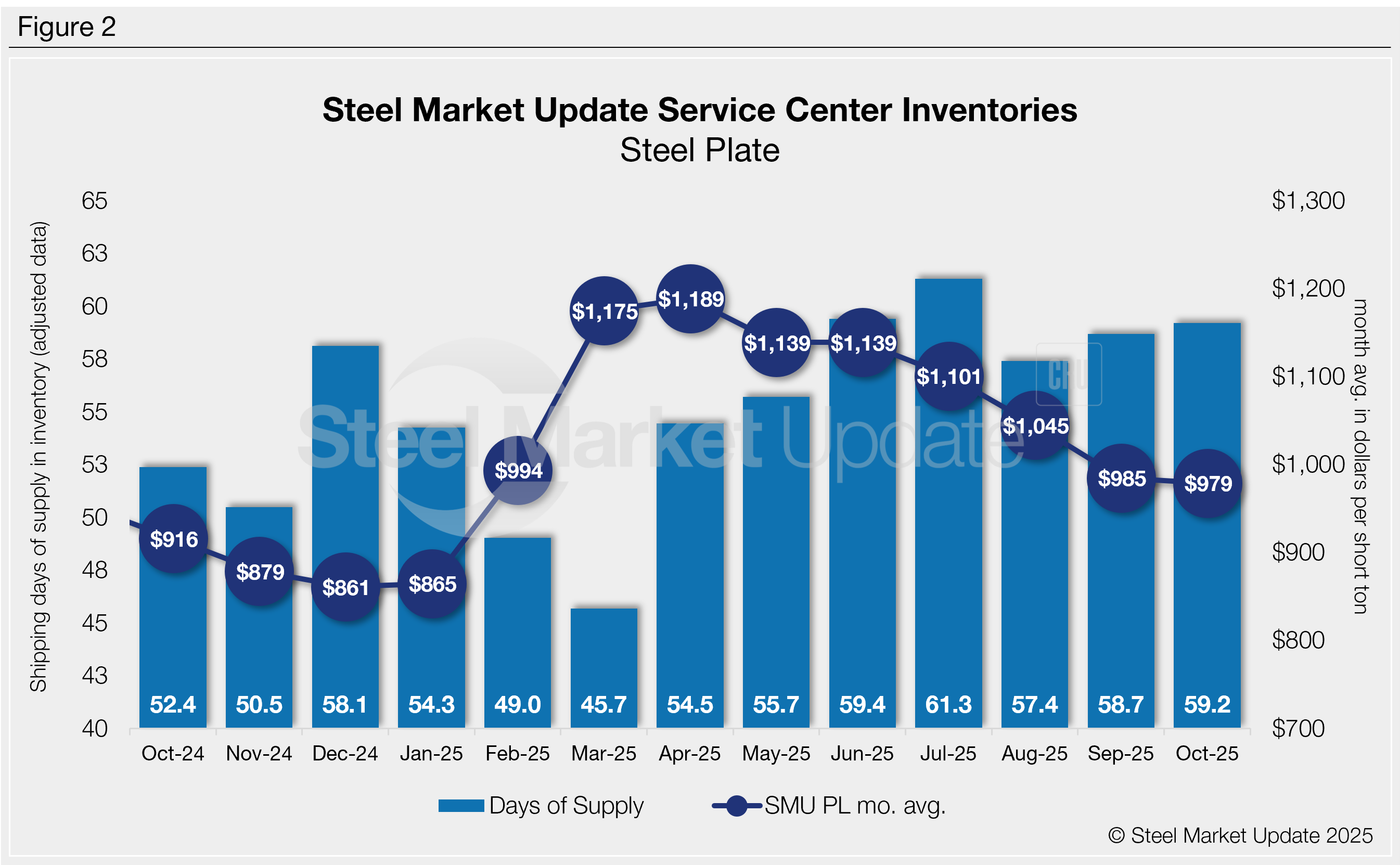

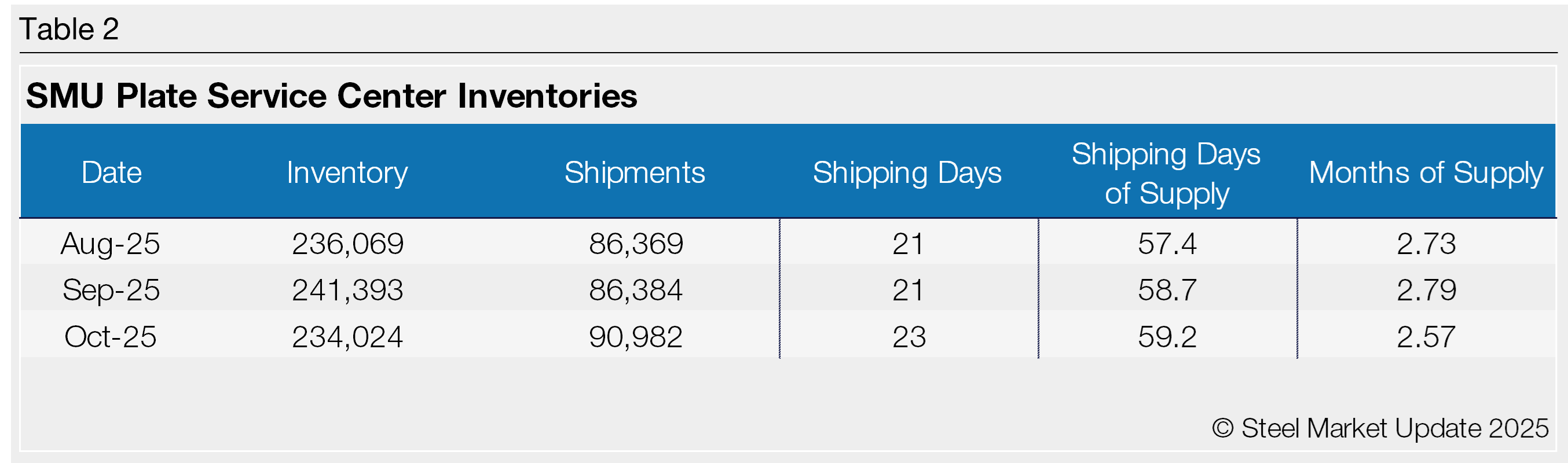

Plate = 59.2 shipping days of supply

Flat rolled

US service centers’ flat-rolled steel supply edged lower for the third straight month, reaching 53.3 shipping days of supply on an adjusted basis at the end of October, according to SMU data. Flat roll supply is down from a most recent high of 58.6 in July and 63.4 shipping days in October 2024.

Flat roll inventories represented 2.32 months of supply in October, down from 2.59 months of supply in September and 2.75 months in October of last year. The month-on-month (m/m) drop in inventories has helped to support prices, though demand remains subdued.

Shipments in October improved by 9.2% m/m. While a boost in shipment levels was seen vs. September, it was supported by a bump in shipping days and bottoming out in prices. The move kept service center supply in balance with demand.

The latest SMU survey, published Nov. 14, found 45% of service centers were releasing less steel compared to one year ago, while 45% were releasing the same amount of steel. Just 10% reported they were releasing more vs. last year. While demand has seen a marginal improvement, near-bottom pricing may have supported a boost in buying and thus a jump of more than 19% m/m in on-order volumes.

At the end of October, service centers’ shipping days of supply on order hit the highest level year-to-date, and a shift from September’s near five-year low. The latest SMU survey showed hot-rolled coil lead times at 5.30 weeks, up from 4.71 weeks a month ago, and the highest reading since early April.

The shift corresponds well with SMU’s latest survey, which saw 30% of service centers building inventory and the remaining 70% maintaining inventory. Service centers didn’t report any inventory reduction efforts in the latest survey results.

The drop in flat roll supply and the strong rebound of material on order might align with concerns that inventories were falling too low, though today, inventories appear balanced.

But will a nearly 20% boost in intake volume and material on order coincide with an increase in downstream buying or lead to a holiday overhang? The increase could come at the same time seasonal demand slows, creating excessive inventory at service centers from November to January.

Plate

US service center plate inventories edged higher for a second consecutive month in October, even as shipments picked up, according to SMU data. At the end of October, service centers held 59.2 shipping days of supply, up from 58.7 in September. Plate supply in October represented 2.57 months of supply, down from 2.79 months in September.

October plate supply is noticeably higher than year-ago levels, when service centers carried 52.4 days of supply or 2.28 months of supply. Though the latest inventory levels are slightly elevated, they are not overly high given the expectation of stable shipments through the end of the year.

Material on order rose nearly 6% in October, boosted by a bump in shipping days of supply on order. At the end of October, service centers had more shipping days of supply on order, m/m and y/y. Service centers do not need to carry as much inventory because of additional domestic capacity. Plate mill lead times remain short at 4.73 weeks, according to the latest SMU survey.

Service center demand has not picked up materially after the summer, though market contacts have noted that more project work has gone out to bid, and 2026 looks a bit promising.

Mills have been pushing through price increases as the market starts to look toward next year, though increases are slow to stick. While inventories are more than sufficient to meet current demand, service centers appear to be adding orders ahead of Q1, supported by the increase in material on order at the end of October.