Analysis

December 9, 2025

Final Thoughts

Written by Ethan Bernard & Stephen Miller

Nearly a year has passed since we launched our scrap survey at SMU. In February, when the survey began, our prime grade price averaged $447.50 per gross ton (gt). For December, that price now stands at an average of $400/gt. But price is just one part of the story. Our scrap survey provides a wealth of information for those who want to make data-driven decisions for their business.

So, let’s peek into the data from this last survey of 2025. We’ll have respondent comments and insights from SMU’s own Stephen Miller, who brings over 40 years of experience to the table.

Of course, we’ll have to touch on this year’s major theme: tariffs. But tariffs or no tariffs, the industry will continue to chug along regardless. Now onto the survey! Where applicable, we’ve added the respondent comments. And the takeaways are Stephen’s analysis of the data.

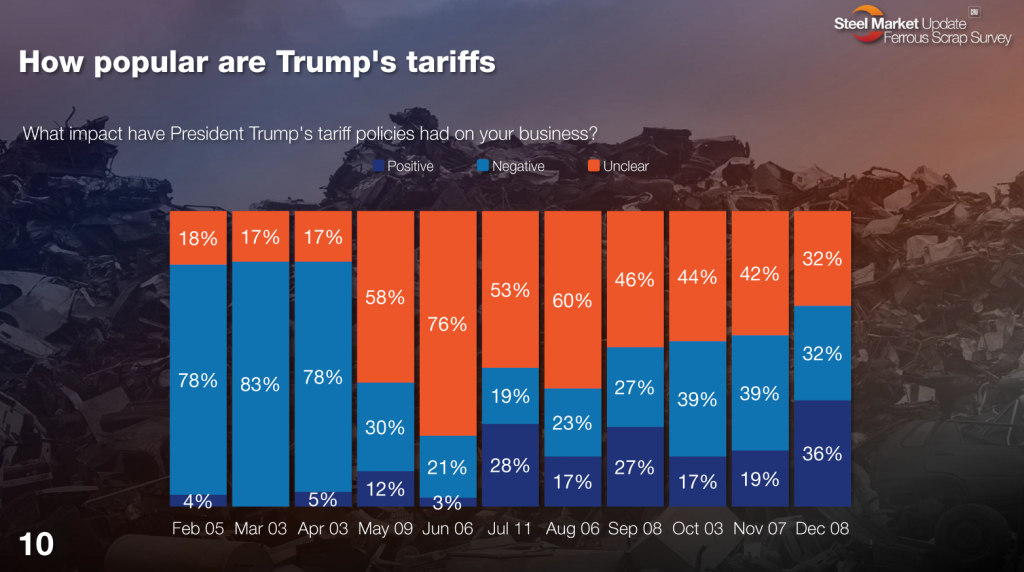

What impact have President Trump’s tariff policies had on your business?

Respondents say:

“Kept supply tight in the US.”

“New opportunities.”

“Having to absorb the tariffs.”

“Can’t figure out why they haven’t helped.”

“Pushing pricing and availability of certain grades more limited or cost increases.”

Takeaway:

As the year progressed, more respondents said they were unclear whether the tariffs are helping, and the yea and nay responses started to even out. This could be because steelmakers are predicting the tariffs will help the industry in 2026.

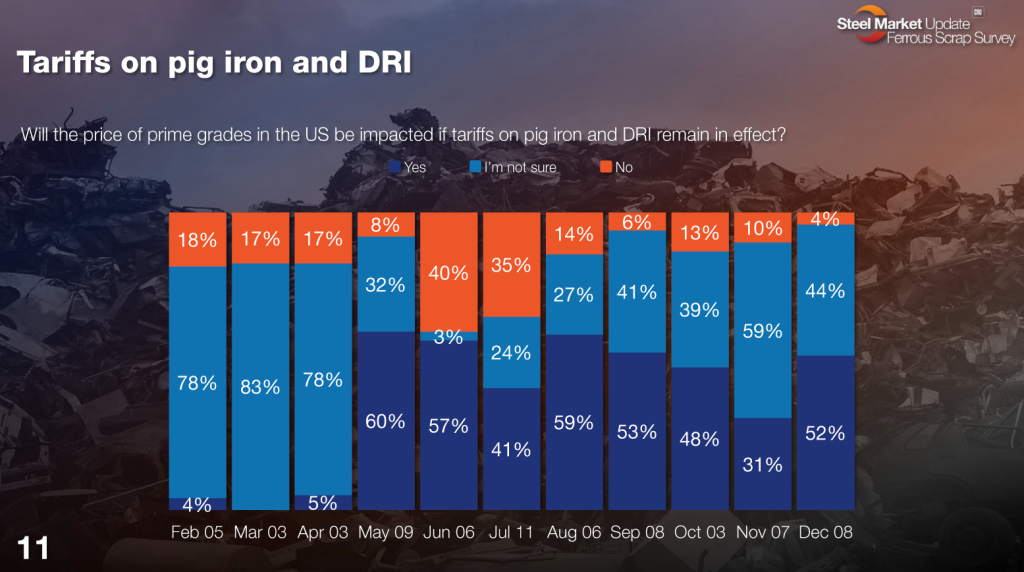

Will the price of prime grades in the US be impacted if tariffs on pig iron and DRI remain in effect?

Respondents say:

“Will force prices higher.”

“Better grades of steel demand, better grades of scrap.”

“Raw materials costs will increase overall prices of steel.”

Takeaway:

If DRI and pig iron were tariffed at any rate above 10%, it would create greater demand for prime-grade scrap and push prices higher. The December survey results indicate the trade agrees.

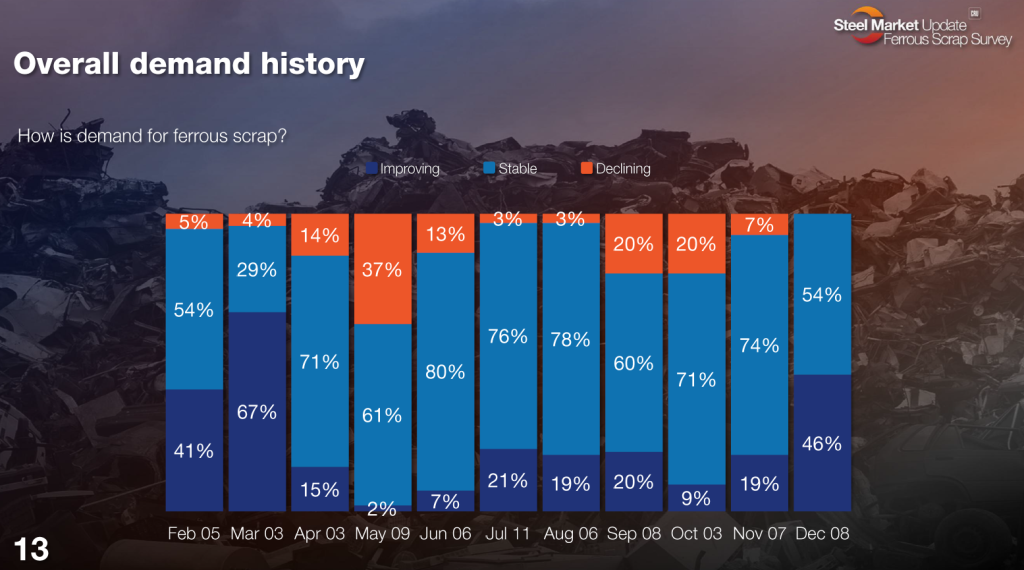

How is demand for ferrous scrap?

Respondents said in December:

“Seasonal movement… mills rebuilding inventories: scrap supply tight.”

“Flow has not changed.”

“Going sideways.”

“I believe demand is stable, but I also think that supply of several grades is diminishing.”

“Nothing significant has changed.”

Takeaway:

Over the last several months, the market has been supply-driven, with demand remaining relatively unchanged. Scrap flows began to taper off in October due to prices, and now, with the normal seasonal reduction in scrap collection and decreased industrial generation during the holiday months, supply will drive prices higher. Mills are projecting an increase in their business. If true, this will further aggravate the pricing situation.

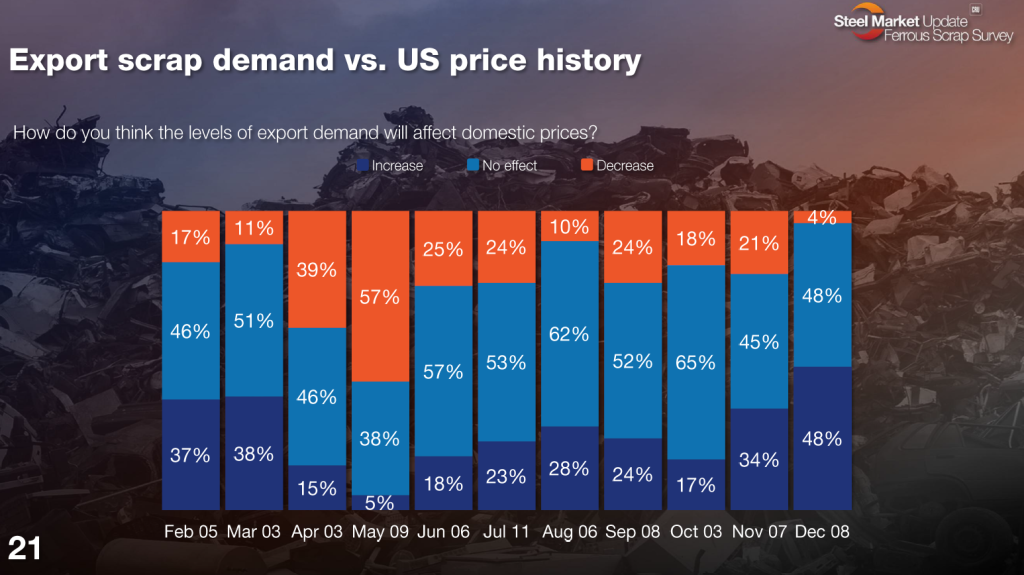

How do you think the levels of export demand will affect domestic prices?

Respondents weigh in:

“More activity in Turkey.”

“Long term could be bad if foreign sources start to develop other sources for scrap.”

“It is pretty much just emotional and it can be ignored.”

“Minimal.”

Takeaway:

Demand in Turkey can firm up pricing in the US for shredded and HMS, but only if they buy more than they have been buying this year. Demand for US scrap in other countries remains subdued.

What’s the big takeaway from this year?

The primary takeaway for 2025 was not much different from that in 2023 and 2024. Scrap prices spiked during the winter months, then fizzled out in the spring. They drifted lower or sideways until December. This shows little growth in scrap demand, as supply determines the price.

As for what’s in store for 2026, we’re not making any projections just yet. Still, next year promises to be an exciting year in scrap, and we’ll be reporting on it every step of the way.

We hope, for some of you, 2026 will be the year you decide to contribute to our scrap survey as it continues to grow. To sign up, you can contact SMU Deputy Editor-in-Chief David Schollaert at david@steelmarketupdate.com.

Ethan Bernard

Read more from Ethan Bernard