Analysis

December 11, 2025

HRC vs. prime scrap spread continues to widen in December

Written by Ethan Bernard & Stephen Miller

The spread between domestic hot-rolled coil and prime scrap prices widened for a third consecutive month in December, based on SMU’s most recent pricing data.

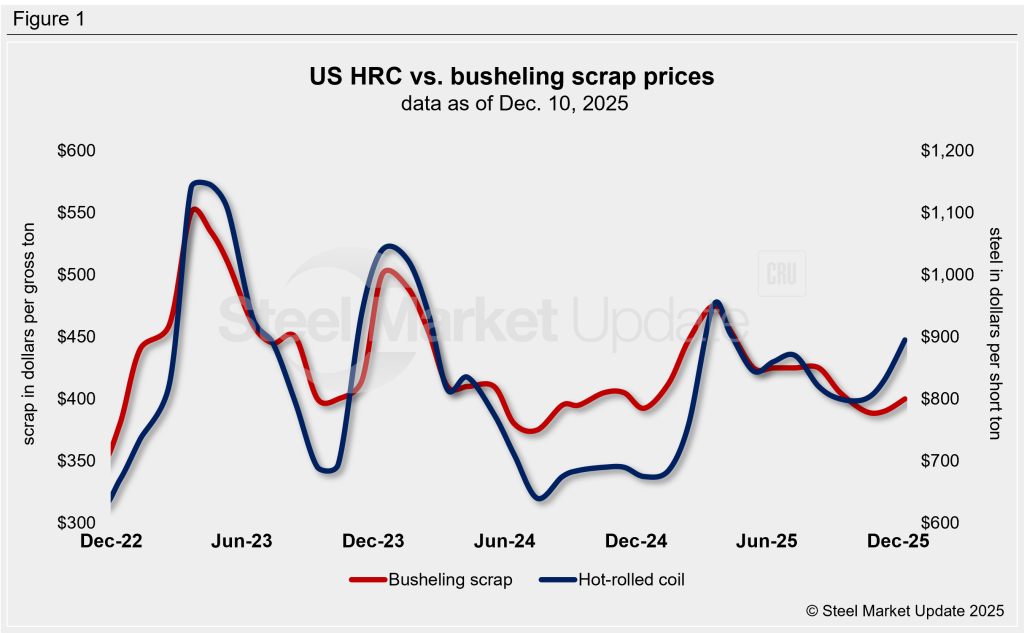

SMU’s average HRC price was $895 per short ton (st), FOB mill, east of the Rockies, as of Tuesday, Dec. 9. That’s even with the previous week and up $65/st from the prior month.

Meanwhile, busheling tags in December increased $10 month over month to an average of $400 per gross ton (gt).

Figure 1 shows price histories for each product.

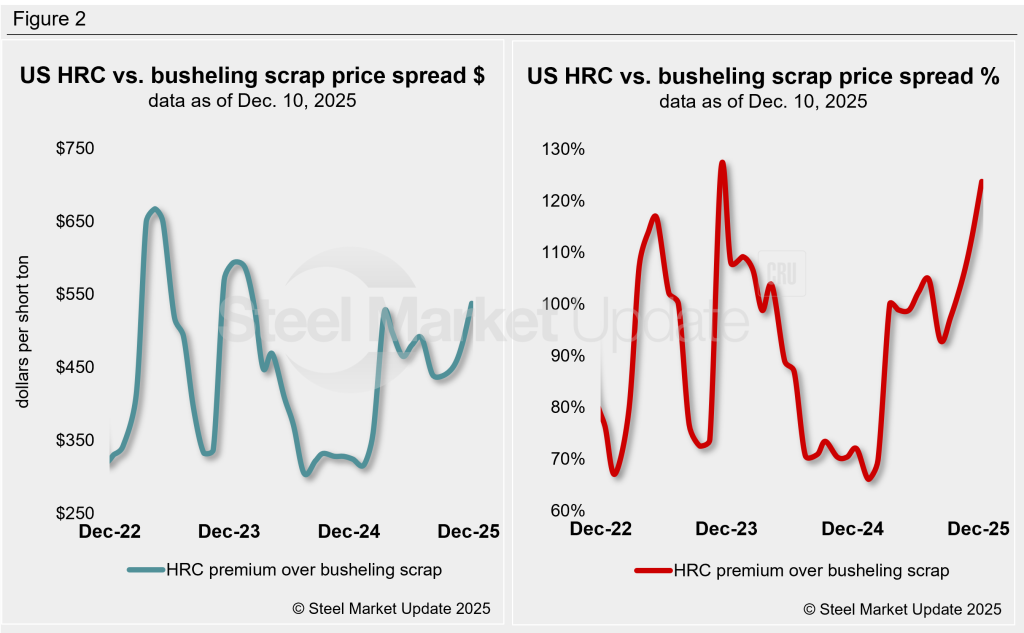

After converting scrap prices to dollars per short ton for an equal comparison, the differential between HRC and busheling scrap prices was $538/st as of Dec. 10. That’s a jump of $56/st from a month earlier. We have to go back to mid-January 2024 to find a wider spread when it stood at $588/st (Figure 2).

What’s going on?

US steelmakers raised #1 busheling by only $10/gt in December, despite other grades moving up $20/gt. As mentioned, HRC went up by $65/st ($73/gt) during the same period.

The scrap trade is expecting busheling prices to increase further in January. At this point, it’s hard to say how much. Predictions are $20-30/gt, with many saying these figures are conservative.

In January, it is also speculative to say by how much HRC prices could increase, if at all. However, unless they go up $20/gt, this spread should start to narrow or hold pat. In any case, the spread should remain very generous for EAF-based flat-rolled steel producers. Many believe they need increases in volume rather than price.

HRC premium as a percentage

The graph on the right-hand side of Figure 2 shows the spread relationship differently: We have graphed HRC’s premium over busheling scrap as a percentage. HRC prices now hold a 124% premium over prime scrap, up from 113% a month ago.

Ethan Bernard

Read more from Ethan Bernard