Analysis

December 15, 2025

November service center shipments and inventories report

Written by David Schollaert

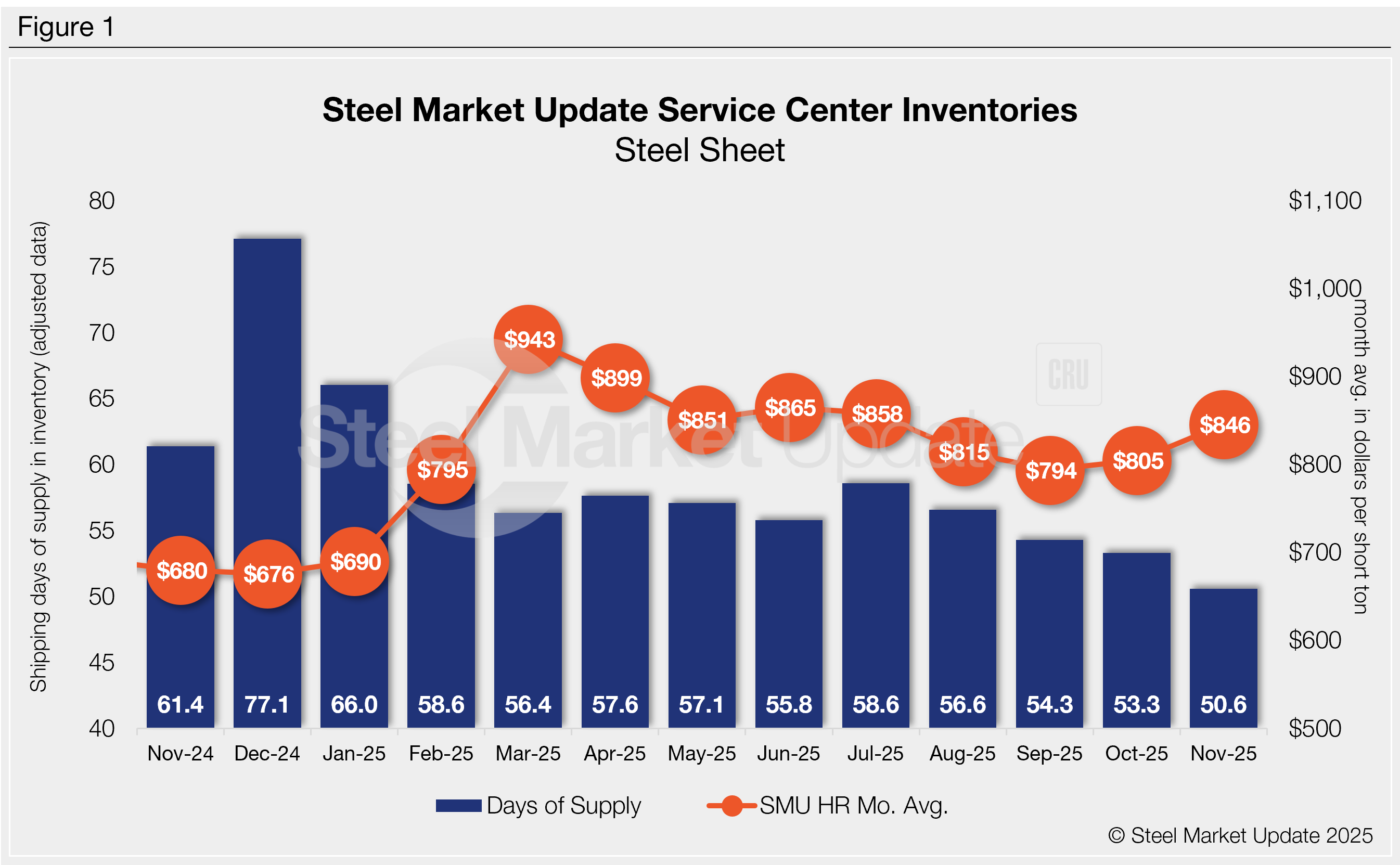

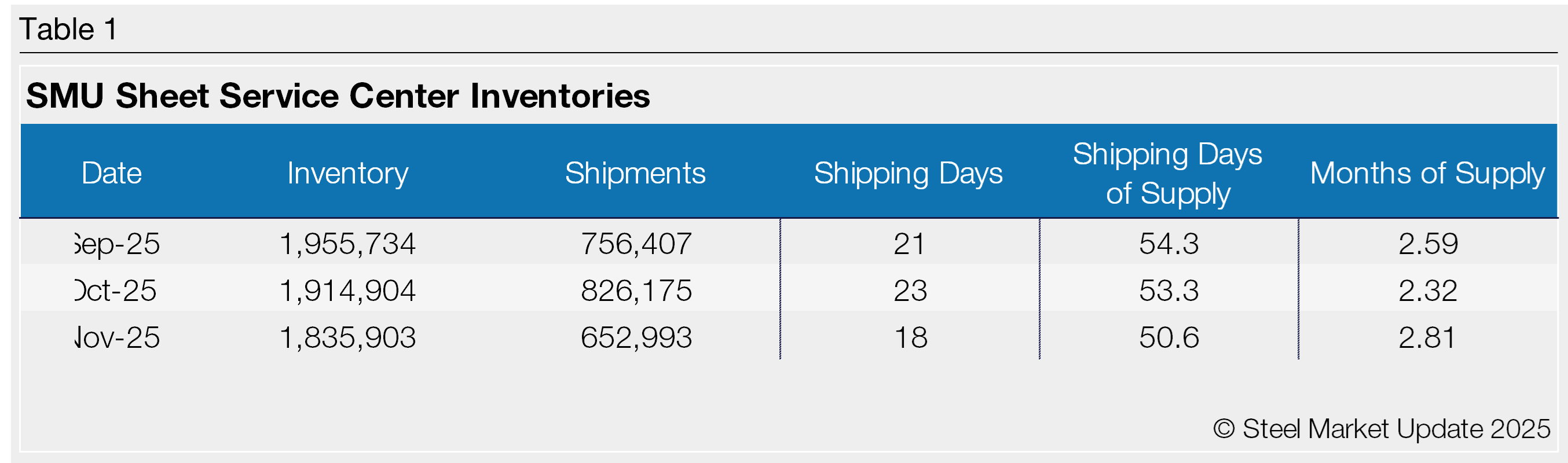

Flat rolled = 50.6 shipping days of supply

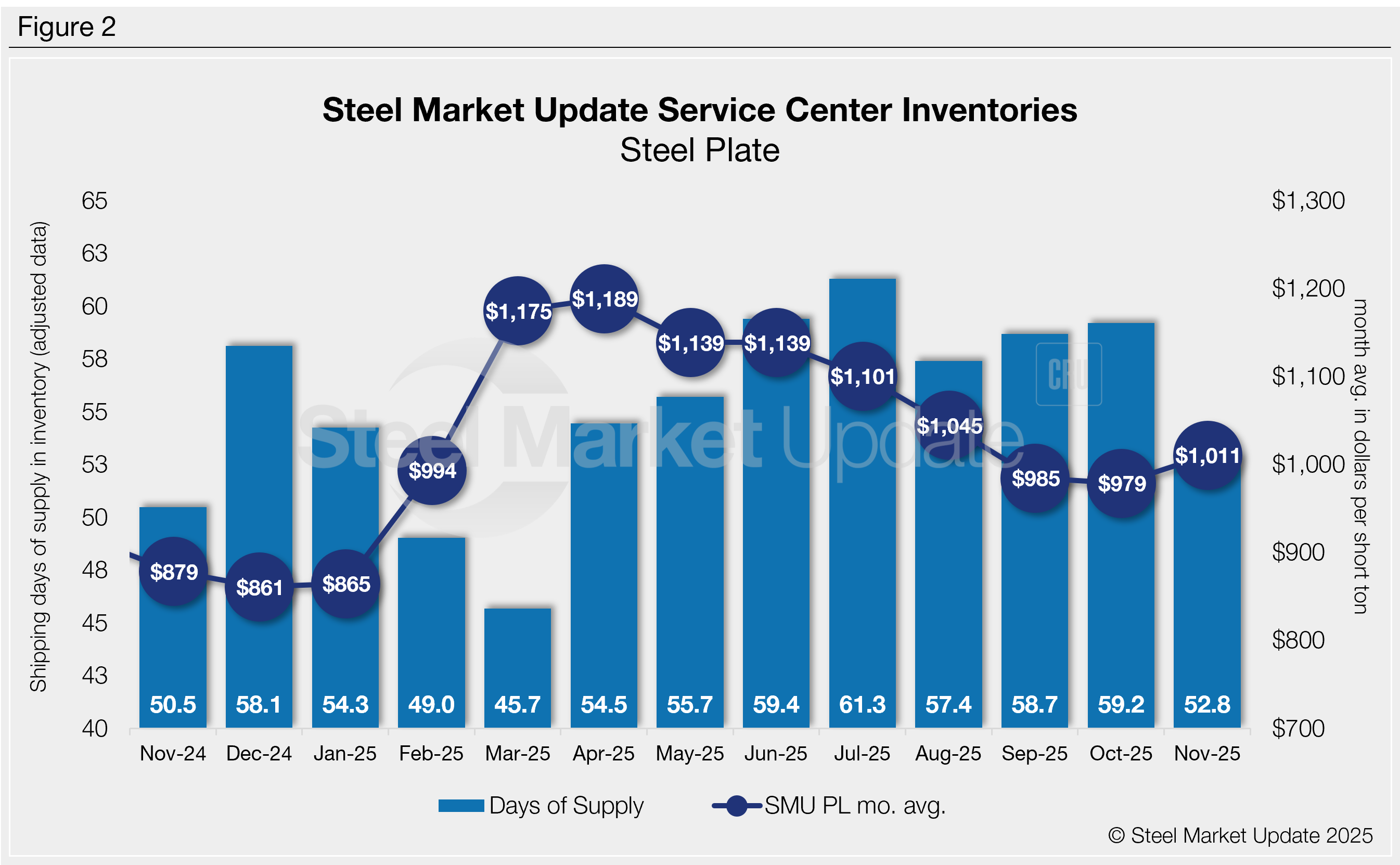

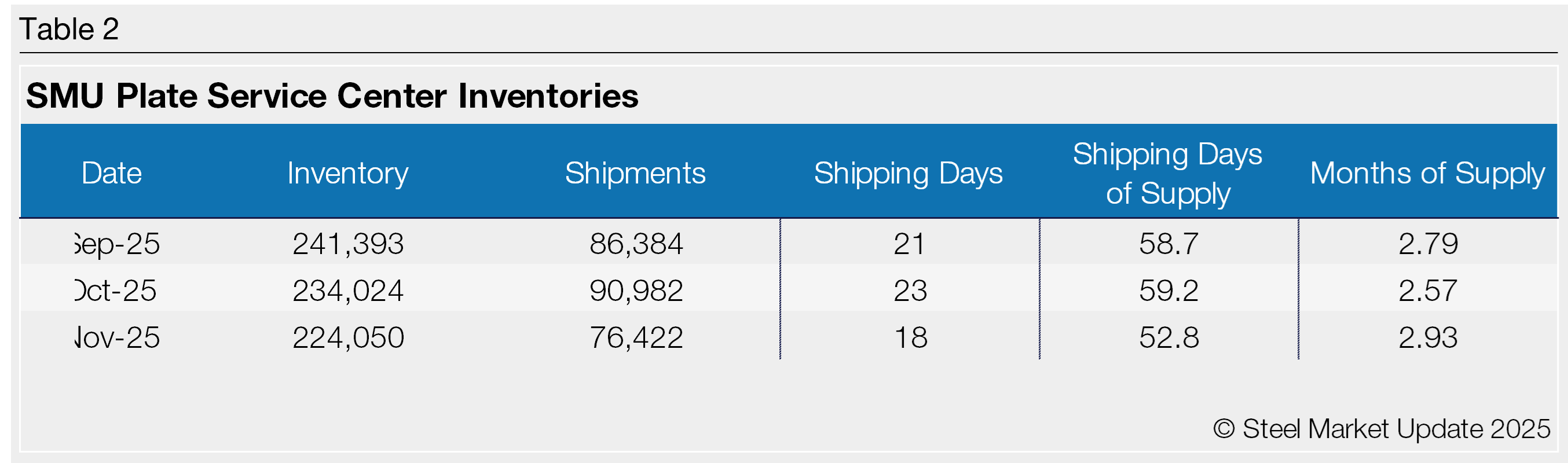

Plate = 52.8 shipping days of supply

Flat rolled

US service centers’ flat-rolled steel supply declined for the fourth straight month, reaching 50.6 shipping days of supply on an adjusted basis at the end of November, according to SMU data.

Flat roll supply is at its lowest level since May 2023, and down from a recent high of 58.6 in July and 61.4 shipping days in November 2024.

Flat roll inventories represented 2.81 months of supply in November, up from 2.32 months in October but still below 3.23 months in November of last year. The month-on-month (m/m) drop in inventories is a typical seasonal trend, though it is currently slightly sharper. The dynamic is likely the driver behind recent upticks in buying and support for higher prices.

Shipments in November were down 21% m/m. While a decline in shipment levels was seen vs. October, it was aided by fewer shipping days and an upward turn in prices. The move kept service center supply in balance with demand.

It’s worth noting that while overall shipping was down in November vs. October, the daily shipping rate was up m/m. With five fewer shipping days in November, seasonal dynamics are in full swing.

The latest SMU survey, published Dec. 12, found that still nearly 50% of service centers were releasing less steel compared to one year ago, while 36% were releasing the same amount of steel. Just 14% reported they were releasing more vs. last year. While demand has seen marginal improvement, pricing gains appear to keep spot buying primarily hand-to-mouth. Thus, it’s no surprise to see a decline of 1.6% m/m in on-order volumes.

At the end of November, service centers shipping days of supply on order were down 2.6% m/m, but still above September’s near five-year. The latest SMU survey showed hot-rolled coil lead times at 5.58 weeks, up from 5.30 weeks a month ago, and one of the highest readings since early Q2.

The result corresponds well with SMU’s November survey, which saw, on average, 16% of service centers building inventory. Seventy-five percent were maintaining, with the remaining 9% reducing inventory.

More recent survey results in December report a slight uptick in service centers reporting they are building inventories, likely aligning with the steady results from on-order inventory.

Plate

US service center plate inventories declined in November, supported by a 7.3% boost in the daily shipping rate, according to SMU data. At the end of November, service centers held 52.8 shipping days of supply, down from 59.2 in October. Plate supply in November represented 2.93 months of supply, up from 2.57 months in October.

November plate supply is higher than year-ago levels, when service centers carried 50.5 days of supply or 2.66 months of supply. Though the latest inventory levels are slightly elevated, they are not overly high given the expectation of stable shipments through the end of the year.

Material on order rose sharply in November, up nearly 18% m/m, boosted by a bump in shipping days of supply on order. At the end of November, service centers shipping days of supply on order was up 9.6% vs. October and from November 2024. Service centers do not need to carry as much inventory because of additional domestic capacity. Plate mill lead times remain normal at 5.33 weeks, up from 4.73 weeks a month ago, according to the latest SMU survey.

Service center demand has not picked up materially after the summer, though sources have noted an uptick in special projects, and remain rather bullish about their outlook for 2026.

Mills have been pushing through price increases as the market starts to look toward next year, though increases are slow to stick. While inventories are more than sufficient to meet current demand, service centers appear to be adding orders ahead of Q1, supported by a near 23% bump in the percentage of inventory on order.