Analysis

December 16, 2025

Final Thoughts

Written by Michael Cowden

Sheet prices mostly ticked higher again this week. And the reasons shouldn’t come as a big surprise to anyone who has been reading SMU lately.

Lead times have stabilized at higher levels. Mills are less willing to negotiate lower spot prices. And finished steel imports are at their lowest levels since 2009.

Meanwhile—as our premium subscribers already know—service centers’ sheet inventories, which have ticked lower since July, are now at their lowest point since May 2023. (Editor’s note: Contact Luis Corona at luis.corona@crugroup.com if you’re interested in upgrading from an executive subscription to a premium one.)

Where is the peak?

The next obvious questions are where and when prices might peak. Results from our last survey are helpful as you try to assess that.

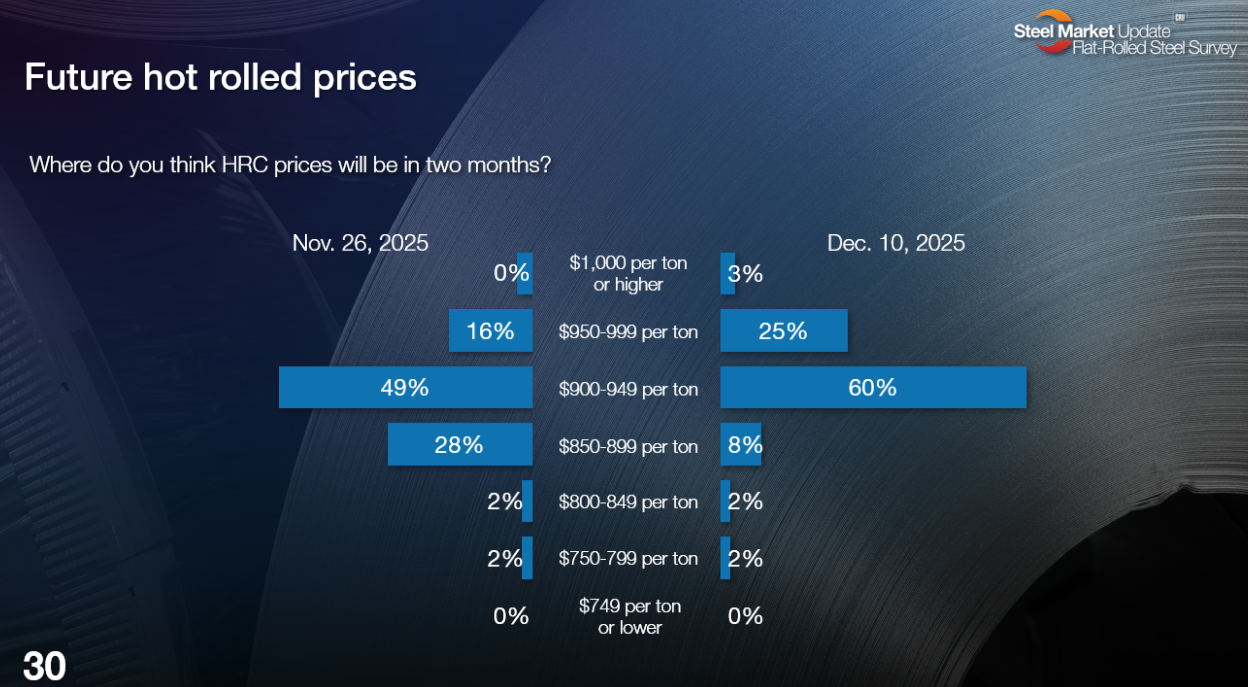

As you can see in the slide below, there is broad agreement among our survey respondents that hot-rolled coil prices in mid-February should be slightly higher than they are now. (Editor’s note: You can click on any of the graphics below to expand them. The page numbers correspond to where they are in our full survey results, which premium subscribers can find here.)

Sixty percent of respondents expect HR prices will be $900-949 per short ton (st) two months from now, up from 49% in late November. And 25% think HR prices could be at $950-900/st by mid-February, up from 16% a few weeks ago. The biggest change: Only 10% think HR prices will be in the $800s/st two months from now, down from 30% in late November.

Here is what some of those respondents had to say:

“It’s going to be a slow upward climb due to economic headwinds and demand that can’t seem to get its feet planted.”

“HR in the US is running tight due to few Imports.”

“That’s what my gut tells me.”

“We think demand is just too weak to support pricing at these levels. We think we’ll reverse back to where we were in October/November in Q1.”

“Prices are going up, but demand seems to be slowing.”

“Solid mill order books for the next two months.”

“Mills pushing the envelope.”

“Business is picking up, so the increases will keep coming.”

“Imports will limit the upside.”

“Slow rise in prices to a sustained level due to increasing domestic demand.”

Service centers are up too (mostly)

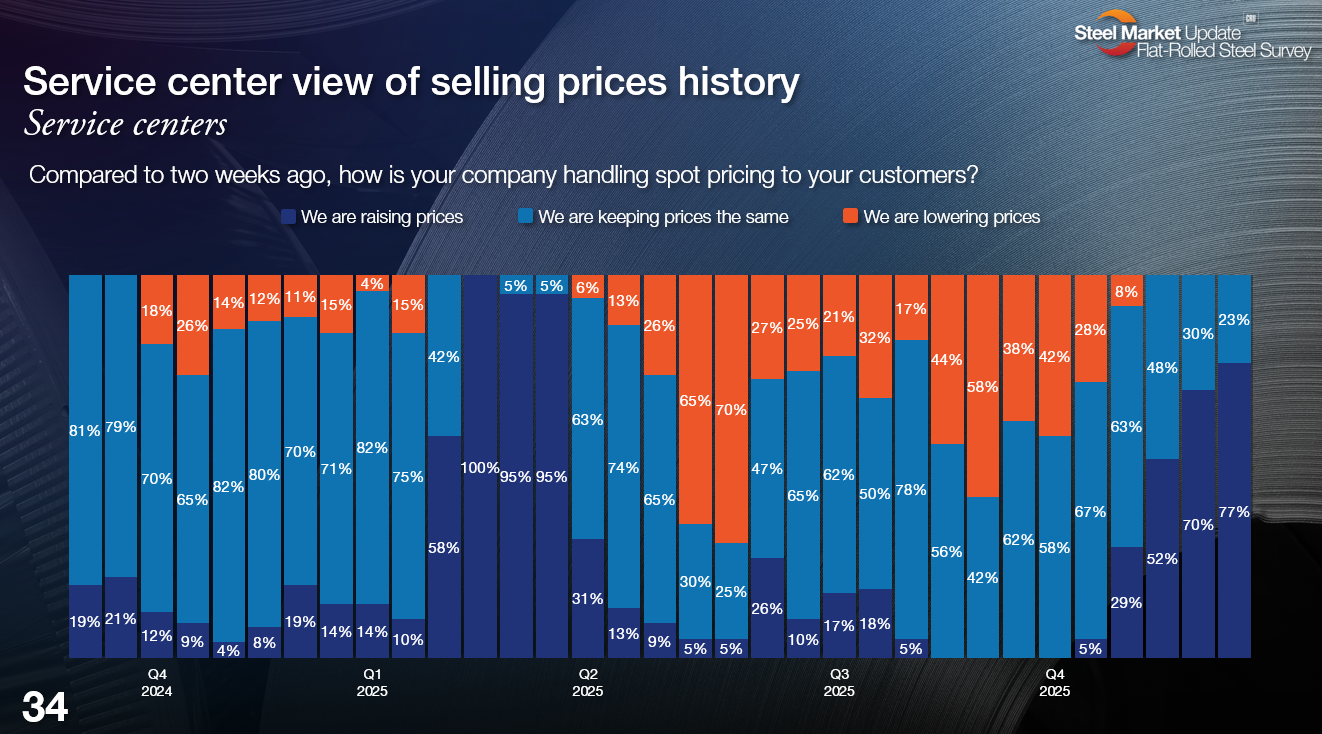

And, as I’ve noted in prior columns, service centers tell us that they’re raising prices along with mills:

Seventy-seven percent of service center respondents say they are increasing prices. That’s the highest level we’ve seen since Q1 – in the buying frenzy that followed Trump’s inauguration and the announcement of stricter Section 232 tariffs.

That said, we’ve also heard from some of you that while you’re raising prices – or at least holding the line – that some of your competitors aren’t.

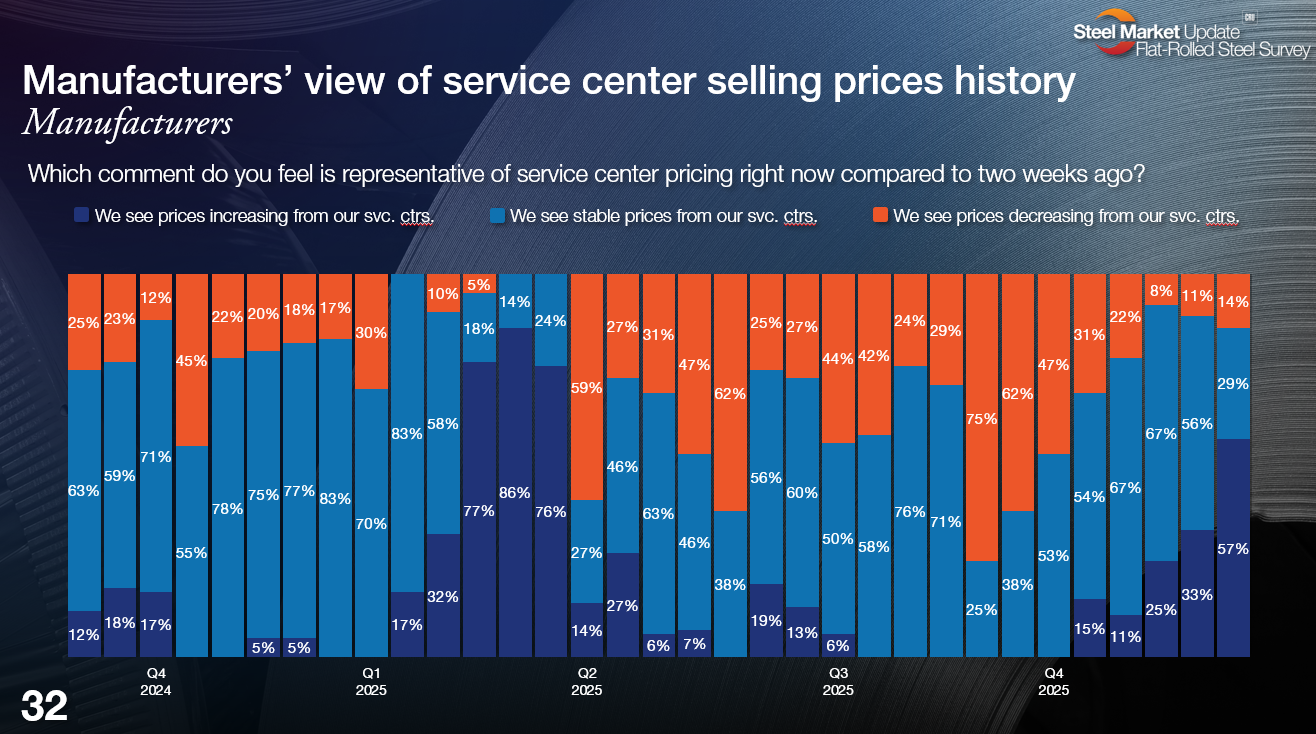

For what it’s worth, that’s why we ask manufacturers the same question: are service centers raising prices?

And while a majority of manufacturers (57%) also report back that service centers are raising prices, a minority (14%) say they’re seeing lower prices from their service center suppliers. That could indeed indicate that not everyone is selling at replacement cost.

When is the peak?

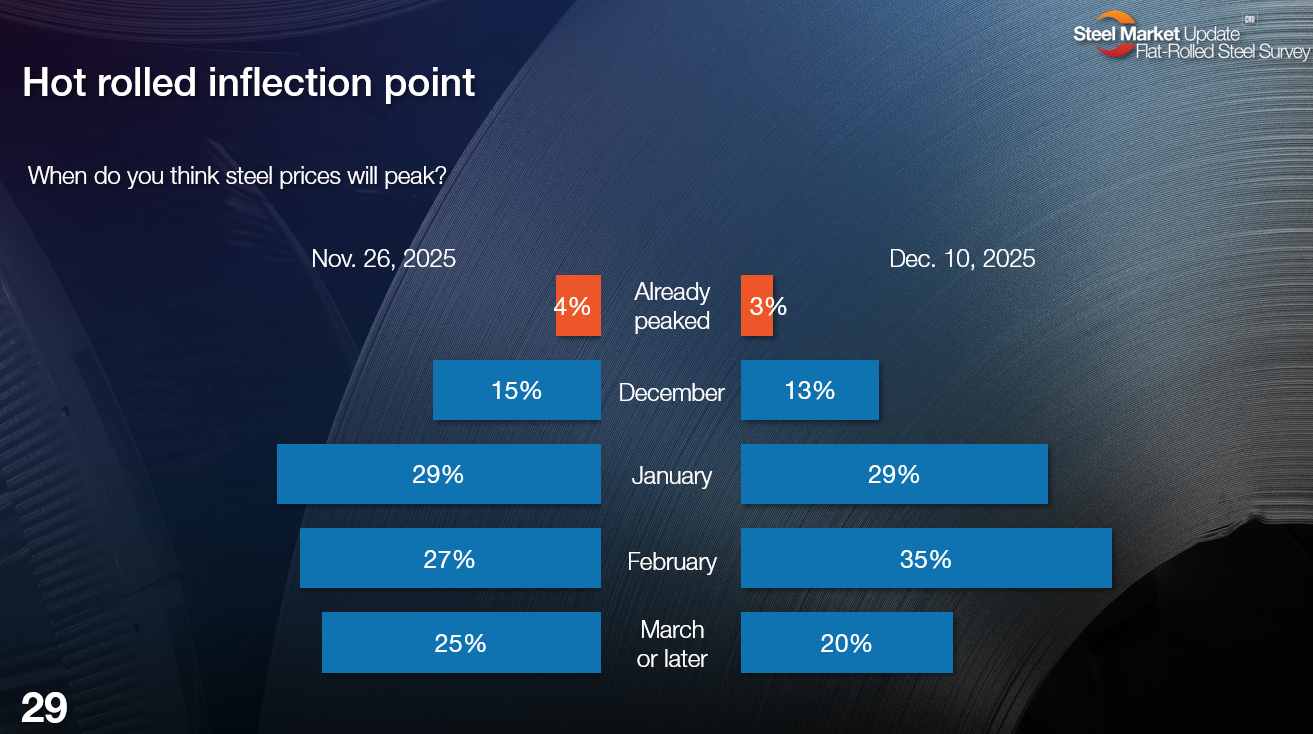

But if there is a broad consensus that HR prices will continue to move upward, even in the absence of strong demand, there is less consensus on how long the current rally will last.

Most people think the current rally has legs into next month (29%) or February (35%). And a significant minority (20%) thinks the gains could continue into March or later. That said, not everyone is bullish. Sixteen percent think prices have already peaked or will later this month.

Here is what some of those respondents had to say:

“The mills have a good strategy right now, but they can only hold out for so long. Unless demand increases, the buying flurry will be over.”

“Momentum is back, but not demand.”

“Producers will limit production and claim it’s demand to keep pushing prices up, until they get their hand slapped by government.”

“I feel early January the pricing momentum mills have will disappear due to poor demand. I hope I’m wrong.”

“Late January/early February. Could be extended with some outages, but I believe most buyers are exhausting December and January buys in order to avoid February purchases at the top of the perceived market.”

“The upward trend or rally has started. It will be bumpy until mid to late January and then run until April/May.”

“Will be a short-lived rally. Demand isn’t supporting it.”

“Supply-driven or not, this rally is real. We do have some major concerns that things will reverse course in January though. Just not enough demand.”

“This is a supply driven increase – not demand – so it won’t hold up as long without some improvement in sheet demand.”

“Seems like there is more room to increase in the next month or two, a lot of contract buying and lack of imports should keep prices solid into the new year.”

“Mills will use any 2026 demand growth to push prices higher, should peak in March.”

“Slow rise in prices to a sustained level due to increasing domestic demand.”

“By February, we should know how the balance of Q1 will look.”

“There’s a lot of meat left on that bone.”

“Tariff impacts, and demand is starting to increase.”

“Imports are still unattractive, so there is traction.”

You’ve probably noticed a lot of comments about demand in the quotes above. And that’s the one indicator that, unlike prices, hasn’t shown much upside to date:

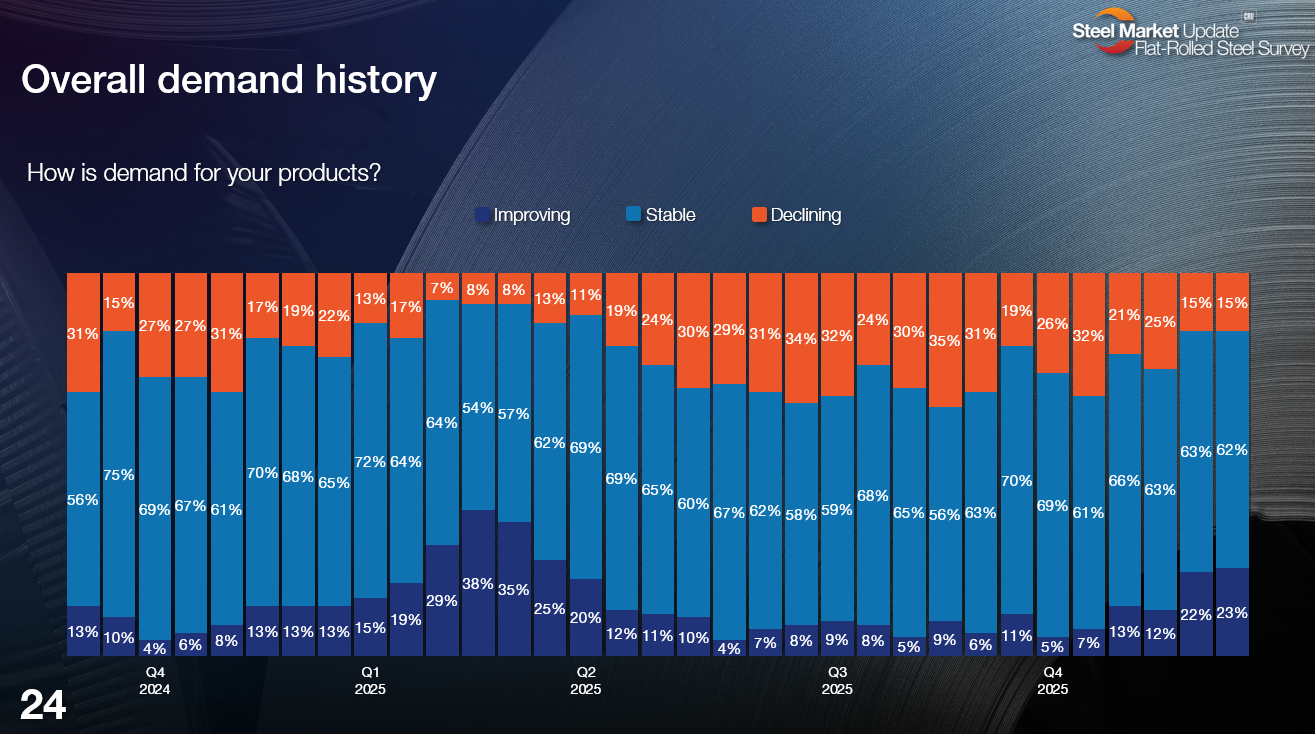

Twenty-three percent of respondents tell us demand is improving. That’s notable. It’s the highest reading we’ve seen since Q1. And we haven’t seen the percentage of people saying demand is improving outnumber those who say it’s declining (15%) since Q1 either.

Most tell us demand is stable (62%). That’s not a bad thing. But it does raise questions about the durability of a rally that, at least so far, appears mostly driven by more limited supply.

A word on tariffs

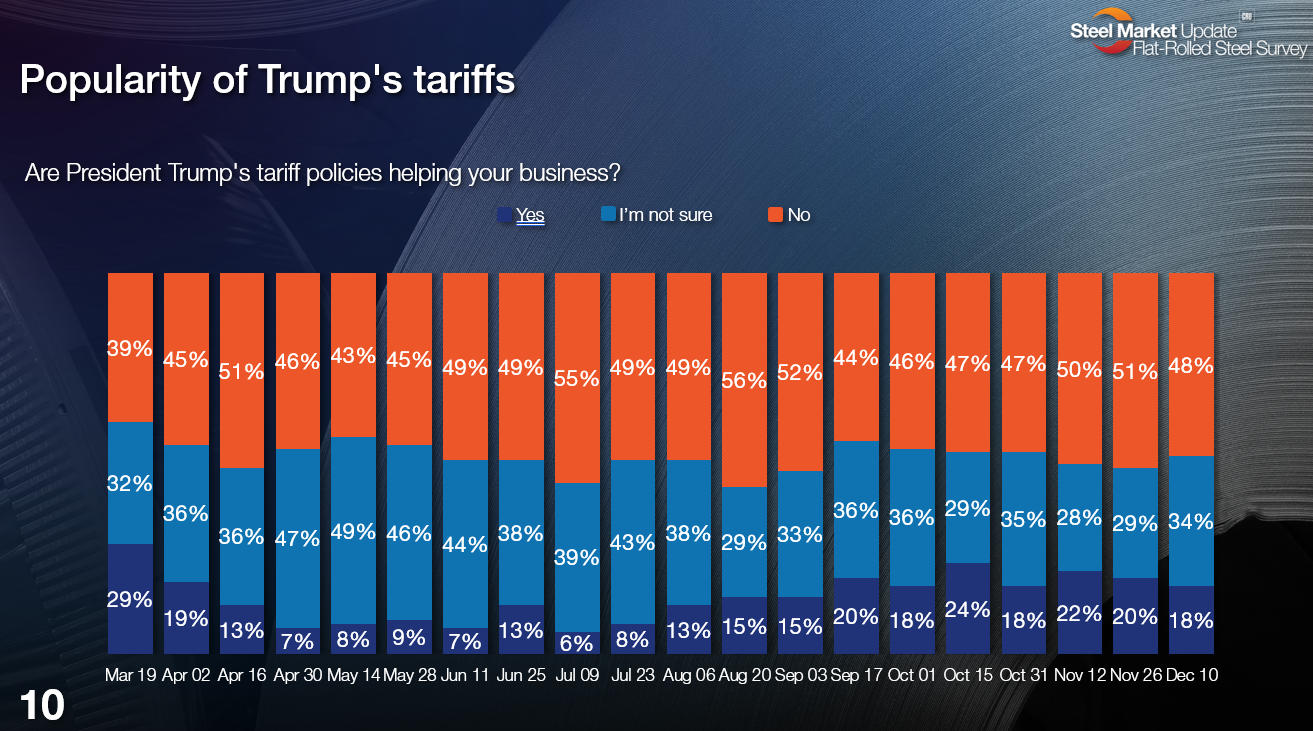

We’ve been asking people what they think of President Trump’s tariff policies since early March. We haven’t written about the matter much lately because, unlike most of the things we track, the numbers have been static:

In any given survey, approximately 20-25% say tariffs are helping their business. Another 30-35% say they’re not sure what impact tariffs are having. And 45-50% say tariffs are hurting business.

Here is what some of those respondents have to say:

“Short term, seems to have prolonged the pain. Everyone is pretty excited about the long-term effect. We are all hopeful that it will materialize.”

“They aren’t helping us yet, but I’m hopeful they will. I’ve been losing hope, though, every month since the end of the third quarter.”

“Helping support domestic prices amid tepid demand.”

“M&M requirements have caused havoc with our buying patterns, but they have allowed for OEM returns from Mexico.”

“We still think tariffs on Canadian and Mexican steel is crazy.”

“Tariffs have pushed domestic pricing up, but it is starting to show the cracks of long-term effects of over-inflated pricing.”

“Our business in Canada has almost halted.”

“Creates uncertainty.”

“Measurable increases to domestic mill order book due to onshoring.”

SMU Community Chat With Timna Tanners

Tariffs, sheet prices, and sheet price forecasts will be among the main subjects of a Community Chat on Wednesday, Dec. 17, at 11 a.m. ET with Wells Fargo Managing Director Timna Tanners.

In short, does “No steel TACO” trump “Sheet Storm”? Register here to find out. Remember to bring some good questions to the Q&A!