Market Data

January 6, 2026

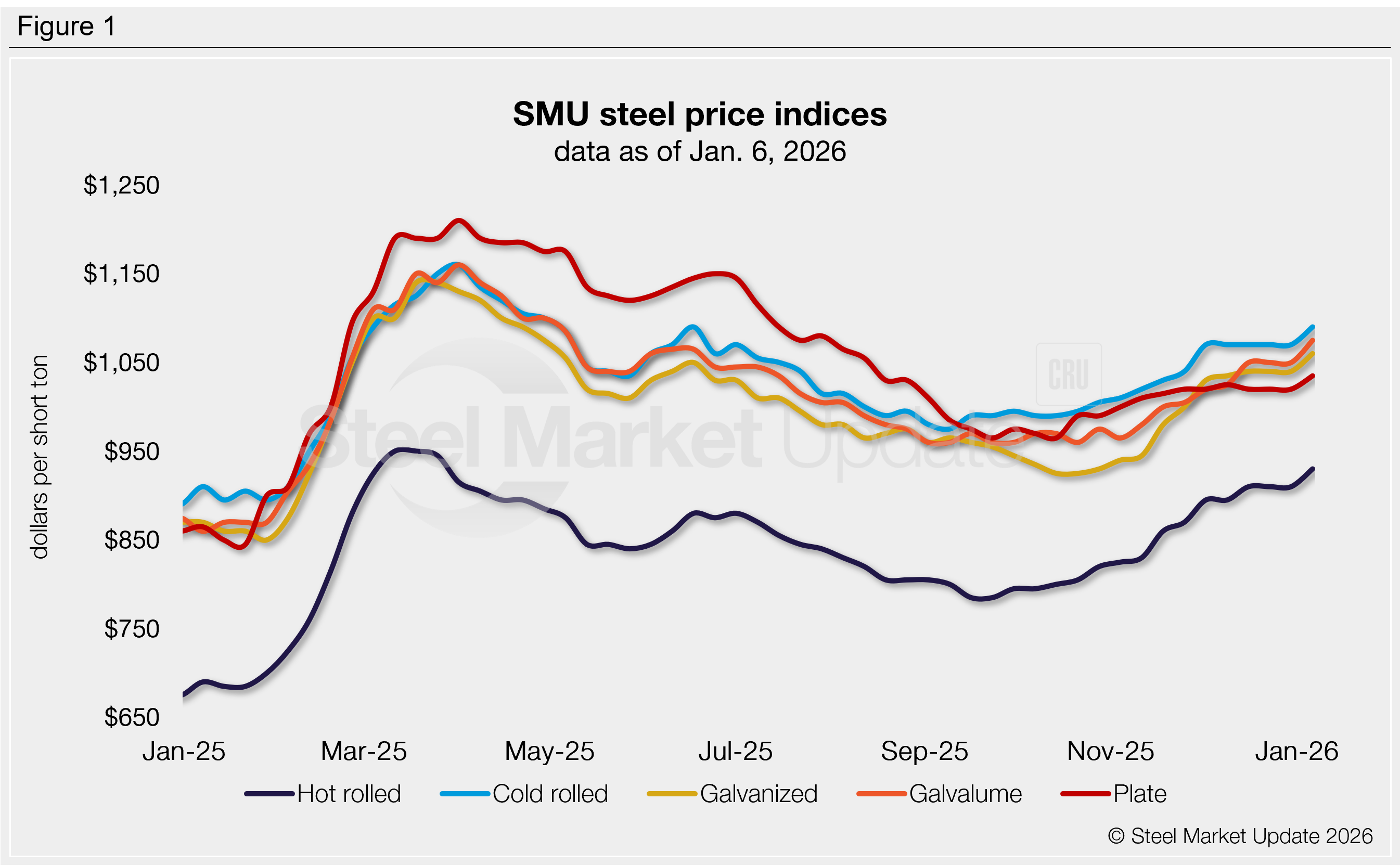

SMU Price Ranges: Sheet and plate prices continue to rise into 2026

Written by Brett Linton & Michael Cowden

Steel sheet and plate prices rose across the board to start the year on limited spot availability at some mills, expectations of higher scrap prices, and hopes of stronger demand in 2026.

SMU’s price assessment for hot-rolled coil now stands at $930 per short ton (st) on average, up $20/st from our prior assessment. Cold-rolled coil and galvanized base prices followed the same trend. Galvalume gained slightly more (up $25/st) and plate gained slightly less (up $15/st). The full details are below.

What they’re saying

Market participants debated whether the run-up in prices at the end of 2025 would continue to be mostly supply driven or whether increased demand could accelerate the trend. Some, for example, pointed toward the automotive sector pulling more steel than expected.

Several also said recent unplanned outages at certain domestic mills could help explain why prices are higher. But those outages don’t appear to have been as significant as initially rumored.

On a very basic level, the market expects scrap to settle higher in January. And EAF producers are likely trying to get ahead of that. (Some market participants griped that mills tend to keep prices flat when scrap goes down.)

Meanwhile, lead times for spot tons at several mills appear to have extended. (SMU will update its lead times on Thursday.) One domestic mill, for example, posted that all its facilities were closed for spot orders. Another said lead times for HR were into mid-February. And a third said it didn’t have HR availability until early March.

As far as buying patterns go, one industry source said he expects consumers will try to max out their CRU-linked contracts in January because they assume that February contract prices will be higher. He suggested that a rush of such buying in January might be followed by a quiet February.

But another industry source said certain US mills – sensing they have a strong hand to start the year – weren’t letting buyers max out of their contracts and instead were holding them at their average tonnage from the year prior. That could function to extend the rally.

Some sources noted that imports at ~$850-860/st delivered to Houston from mills in Asia might be competitive. But they also said they didn’t expect any significant import arrivals until the spring given longer import lead times.

Merger mania

While sources generally agreed it was too early to make sweeping predictions about demand, one thing is clear: a wave of dealmaking across the steel supply chain could reshape the landscape of the US industry in the months ahead.

That consensus comes after SDI confirmed it had made an offer with SGH for BlueScope Steel. That announcement follows the Ryerson-OIympic merger, (which is expected to close this quarter), Worthington’s play for Klöckner, and a potential deal between Cleveland-Cliffs and POSCO (even if details might be scarce at the moment).

Momentum

SMU’s price momentum indicator remains at higher for both sheet and plate products, signaling we expect prices to continue rising from here.

Refer to Table 1 (click to enlarge) for our latest price indices and trends.

Hot-rolled coil: $900–960/st, averaging $930/st

The lower end of our range is up $10/st week over week (w/w), while the top end is up $30/st w/w. Our overall average is up $20/st w/w.

Hot-rolled lead times range from 4–9 weeks, averaging 5.6 weeks as of our Dec. 11 market survey. We will publish updated lead times on Thursday.

Cold-rolled coil: $1,060–1,120/st, averaging $1,090/st

Our entire range is up $20/st w/w.

Cold-rolled lead times range from 5–10 weeks, averaging 7.1 weeks through our latest survey.

Galvanized coil: $1,020–1,100/st, averaging $1,060/st

The lower end of our range is up $40/st w/w, while the top end is unchanged. Our overall average is up $20/st w/w.

Galvanized .060” G90 benchmark: SMU price range is $1,098–1,178/st, averaging $1,138/st FOB mill, east of the Rockies.

Galvanized lead times range from 5-10 weeks, averaging 7.1 weeks through our latest survey.

Galvalume coil: $1,050–1,100/st, averaging $1,075/st

The lower end of our range is up $50/st w/w, while the top end is unchanged. Our overall average is up $25/st w/w.

Galvalume .0142” AZ50, grade 80 benchmark: SMU price range is $1,404–1,454/st, averaging $1,429/st FOB mill, east of the Rockies.

Galvalume lead times range from 5–10 weeks, averaging 7.3 weeks through our latest survey.

Plate: $990–1,080/st, averaging $1,035/st

The lower end of our range is up $10/st w/w, while the top end is up $20/st w/w. Our overall average is up $15/st w/w.

Plate lead times range from 4–7 weeks, averaging 5.3 weeks through our latest survey.

Brett Linton

Read more from Brett Linton