Analysis

January 27, 2026

Final Thoughts

Written by Ethan Bernard

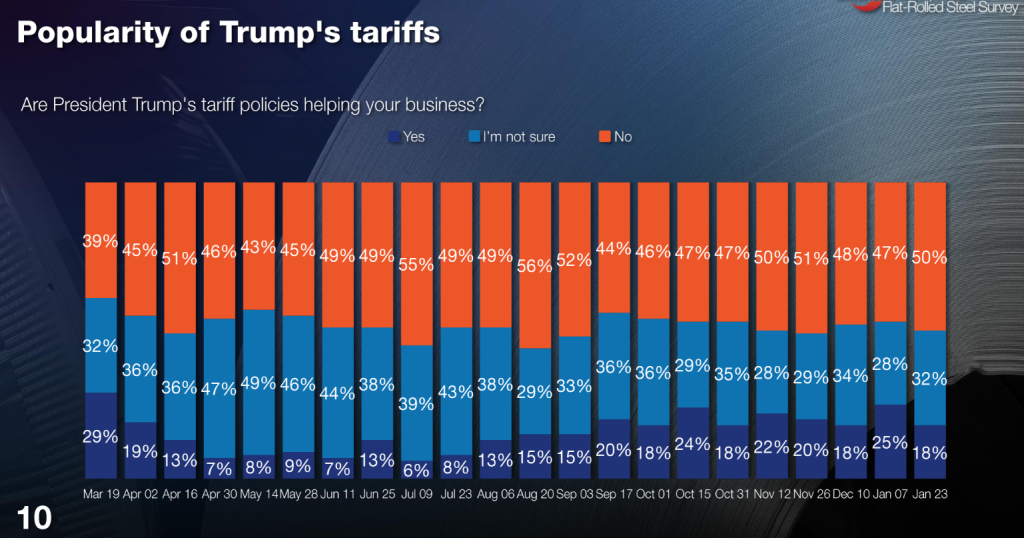

The popularity of President Trump’s tariffs has stayed relatively stable across SMU’s survey results over the last year. In fact, between October 2025 and this month, that favorability has ranged between 46% and 51%, currently standing at 50%. But when opinion remains so split after a policy was implemented a year earlier, what does that say about the policy?

According to our latest survey results, many think the outlook is murky.

On tariffs, this comment seemed to illustrate the point pretty well:

“Nobody is confident on what will happen long term, and large OEMs want certainty to make large-scale long-term investments.”

Certainty? That notion seems to have gone out of date around 2019.

To underline that point, President Trump has threatened tariffs over the last few weeks on South Korea, Canada, the EU (over Greenland), and countries that deal with Iran. None to date have officially been put in place via an executive order or a notice in the Federal Register. But we’ve already learned that, when it comes to tariffs, things could change at any minute.

One common theme in survey comments is that US trade with Canada has been heavily impacted due to tariffs. And that raises the stakes in upcoming USMCA negotiations. It’s beginning to feel a lot more like a Cold War summit than the meeting of an allied trading bloc.

In any case, what we CAN say with certainty is companies continue to do business, despite economic headwinds, cloudy outlooks, or the actual snowstorms that took place this weekend.

HRC prices?

And we all know getting down to business means talking about prices. We have seen SMU’s HRC prices trending up since the end of September. SMU’s current HRC price stands at $960 per short ton on average as of Tuesday, up $15 week over week.

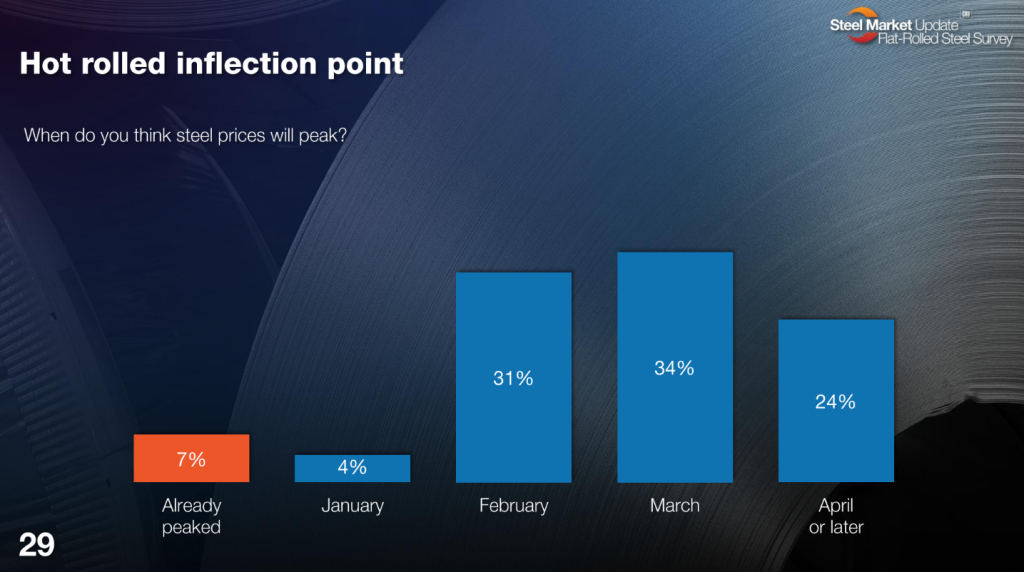

When do survey participants see HRC prices peaking? Well, it appears a clear majority view prices coming back down by the end of the first quarter. Our most recent results show 65% of respondents think prices will most likely top out in either February or March.

Demand still remains a question mark. While opinions vary, it’s hard to find anyone saying it’s great. Still, MANY respondents commented that the tariffs have made an impact.

So, let’s take a look at the actual survey and participant responses to get a wider picture. (If you’d like to participate in our surveys, contact david.schollaert@crugroup.com.)

Are President Trump’s tariff policies helping your business?

“Hurt on the buy side, help on the sell side.”

“Raising costs.”

“We need import steel back in the market. The domestic mills have all of the control now.”

“Keeping domestic mills competitive.”

“They are making costs higher and hurting domestic manufacturing.”

“Still in a variable state.”

“Here in the Pacific Northwest, we historically have had a robust cross border steel trade, from at least the Canada to US direction that’s completely stopped for now.”

“It is impossible for us to sell our customers in Canada in this market.”

“Limited imports driving domestic sourcing, but overall economy could be better.”

“I can’t pass through any increases owing to tariffs. Nature of the business I’m in.”

“It’s Trump’s tariffs that have caused this price spike, so we have these policies to thank for better margins currently. But I think these policies have slowed consumption/demand.”

When do you think steel prices will peak?

“If prices are raised too high, then there are opportunities for imports.”

“Mills are struggling to get caught up. Carry-over doesn’t seem to be slowing, demand typically picks up going into the spring, which will further exaggerate mill lead times.”

“Prices are going to go up for some time.”

“Import pressure despite tariffs.”

“I believe inventories are low and there is very little foreign coming in.”

“I can only imagine what this economy would be doing without all the self-inflicted headwinds.”

“I believe there isn’t enough true demand to keep prices elevated beyond Q1.”

“Too much uncertainty short term for a reverse in pricing. Exports out for short term, lets domestic mills keep pricing artificially higher than warranted.”

“Demand is they key factor. Inventory levels are better than what some are reporting.”

“We have to be getting to the top, $1,000/ton HRC is ridiculous.”

“I just can’t see prices going much higher until demand picks up.”

“Tariffs continue to put domestic sourcing in the driver’s seat. It’s not about demand, it’s about opportunity.”

“I think companies in Mexico will wait until the new USMCA is done to make decisions.”

“Tariff implications and demand have increased vs. supply.”

Where do you think HRC prices will be in two months?

“Ensure that prices are low enough to prevent imports, margins are good at this point.”

“Over the last six months we have only seen slight upticks in pricing. Nothing is indicating that this will change. Slow and Steady.

“Prices have room to increase.”

“Slow market gains.”

“Demand is not there in my opinion.”

“Scrap up.”

“I think the mills will attempt as many monthly increases as will be tolerated by customers.”

“Peak over $950 and then start drifting back down.”

“I think price increases will stall out, hit a peak, and eventually retreat downward.”

“Supply constraints with domestic outages and limited imports (especially Canada essentially out of market).”

“I feel demand is starting to pick up and there is more room from increases.”