Market Data

January 27, 2026

SMU Price Ranges: Sheet continues mostly upward, plate holds as sources assess impact of severe cold

Written by Brett Linton & Michael Cowden

Sheet prices mostly continued their uneven but steady march higher this week, according to SMU’s latest check of the market.

Market participants continued to debate whether the gains were driven primarily by demand or by limited supplies.

With lead times pushing into March, more attention has turned to spring outages. Some sources said they could be more significant than those in the fall – especially should U.S. Steel undertake the board-approved reline of the No. 14 blast furnace at is Gary Works then.

Another topic of discussion: To what extent might cold weather and natural gas disruptions impact production.

AZZ Inc., for example, confirmed scattered outages across Texas and the Southeast. And market sources told SMU that several steel mills had lost some production days not only because of the severe weather but also because icy roads had made it difficult for staff to get to work, especially in areas not accustomed to snow and ice.

We were not aware of any major outages. And it was not immediately clear if a collection of smaller outages or limited production days would be enough to impact steel prices and lead times.

The consensus: the severe weather could cause more problems the longer it lasts.

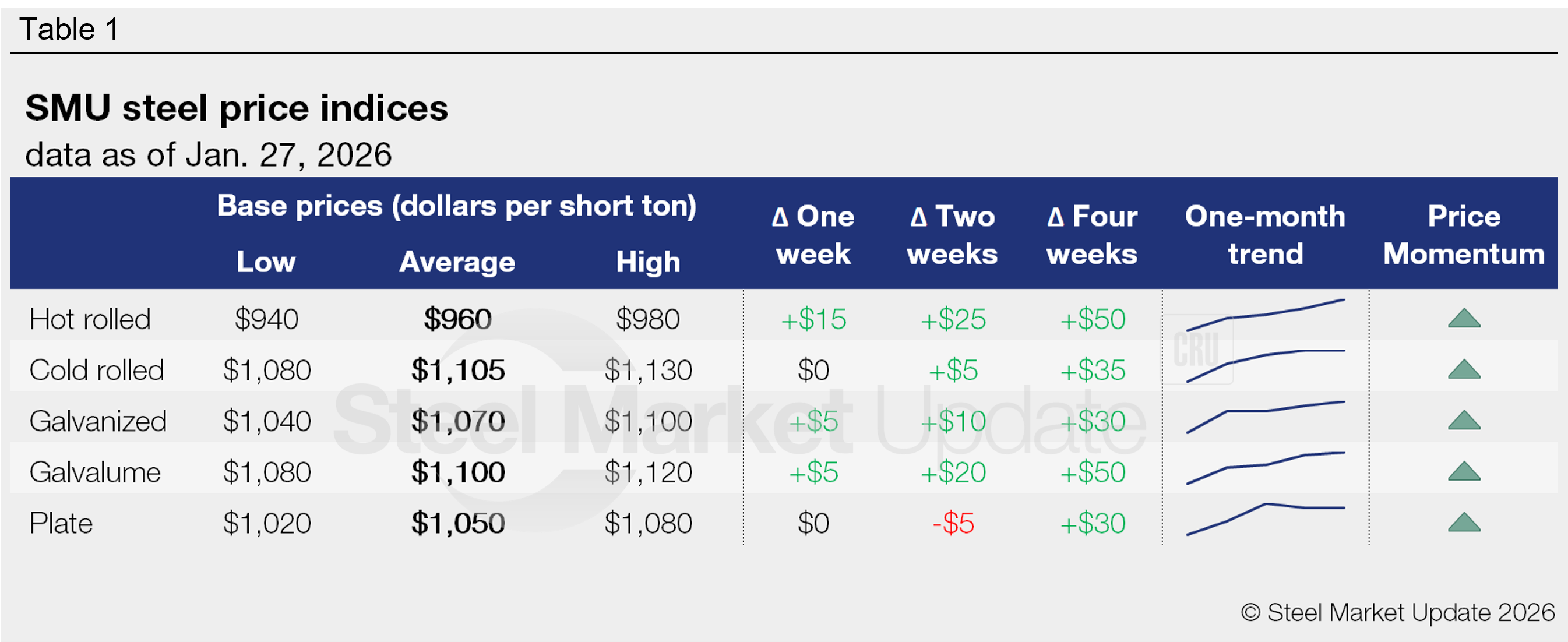

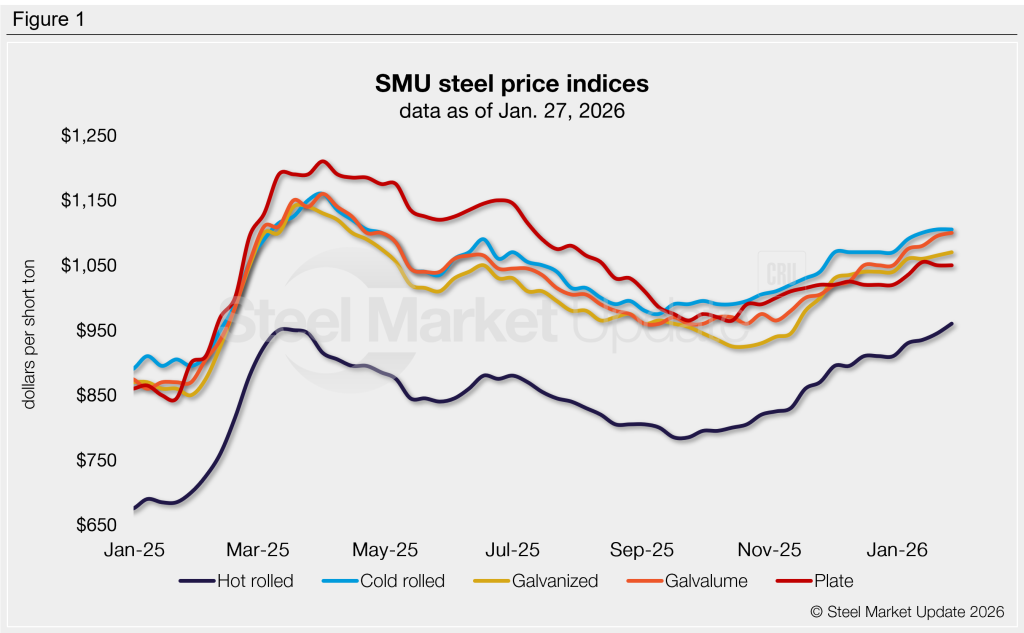

Our hot-rolled coil index increased $15/st week over week (w/w) to a near-two-year high of $960/st. Prices have surpassed the previous peak set last March ($950/st) and are up to levels last seen in February 2024.

Cold rolled held steady at $1,105/st, resting at a nine-month high.

Coated prices both increased by $5/st week over week (w/w) and are at the highest levels seen since last April. Galvanized increased to $1,070/st and Galvalume to $1,100/st.

Our plate index held at $1,050/st, just $5/st below the five-month high we saw in mid-January.

SMU’s price momentum indicator continues to point to higher for both sheet and plate products, signaling that we expect prices to increase further in the short term.

Refer to Table 1 (click to enlarge) for our latest price indices and trends.

Hot-rolled coil: $940–980/st, averaging $960/st

The lower end of our range is up $20/st w/w, while the top end is up $10/st. Our overall average is up $15/st w/w.

Hot-rolled lead times range from 5–8 weeks, averaging 6.0 weeks as of our Jan. 22 market survey.

Cold-rolled coil: $1,080–1,130/st, averaging $1,105/st

Our entire range is unchanged w/w.

Cold-rolled lead times range from 6–10 weeks, averaging 7.6 weeks through our latest survey.

Galvanized coil: $1,040–1,100/st, averaging $1,070/st

The lower end of our range is up $10/st w/w, while the top end is unchanged. Our overall average is up $5/st w/w.

Galvanized .060×48” G90 benchmark: SMU price range is $1,130–1,190/st, averaging $1,160/st FOB mill, east of the Rockies. Note that we have adjusted our galvanized price extras from $78/st to $90/st this week due to recent mill price book revisions.

Galvanized lead times range from 6-10 weeks, averaging 7.5 weeks through our latest survey.

Galvalume coil: $1,080–1,120/st, averaging $1,100/st

The lower end of our range is up $20/st w/w, while the top end is down $10/st. Our overall average is up $5/st w/w.

Galvalume .0142×42” AZ50, grade 80 benchmark: SMU price range is $1,509–1,549/st, averaging $1,529/st FOB mill, east of the Rockies. Note that we have adjusted our Galvalume price extras from $354/st to $429/st this week due to recent mill price book revisions.

Galvalume lead times range from 7–10 weeks, averaging 8.2 weeks through our latest survey.

Plate: $1,020–1,080/st, averaging $1,050/st

The lower end of our range is up $20/st w/w, while the top end is down $20/st. Our overall average is unchanged w/w.

Plate lead times range from 5–8 weeks, averaging 6.0 weeks through our latest survey.

Brett Linton

Read more from Brett Linton