Market Data

February 3, 2026

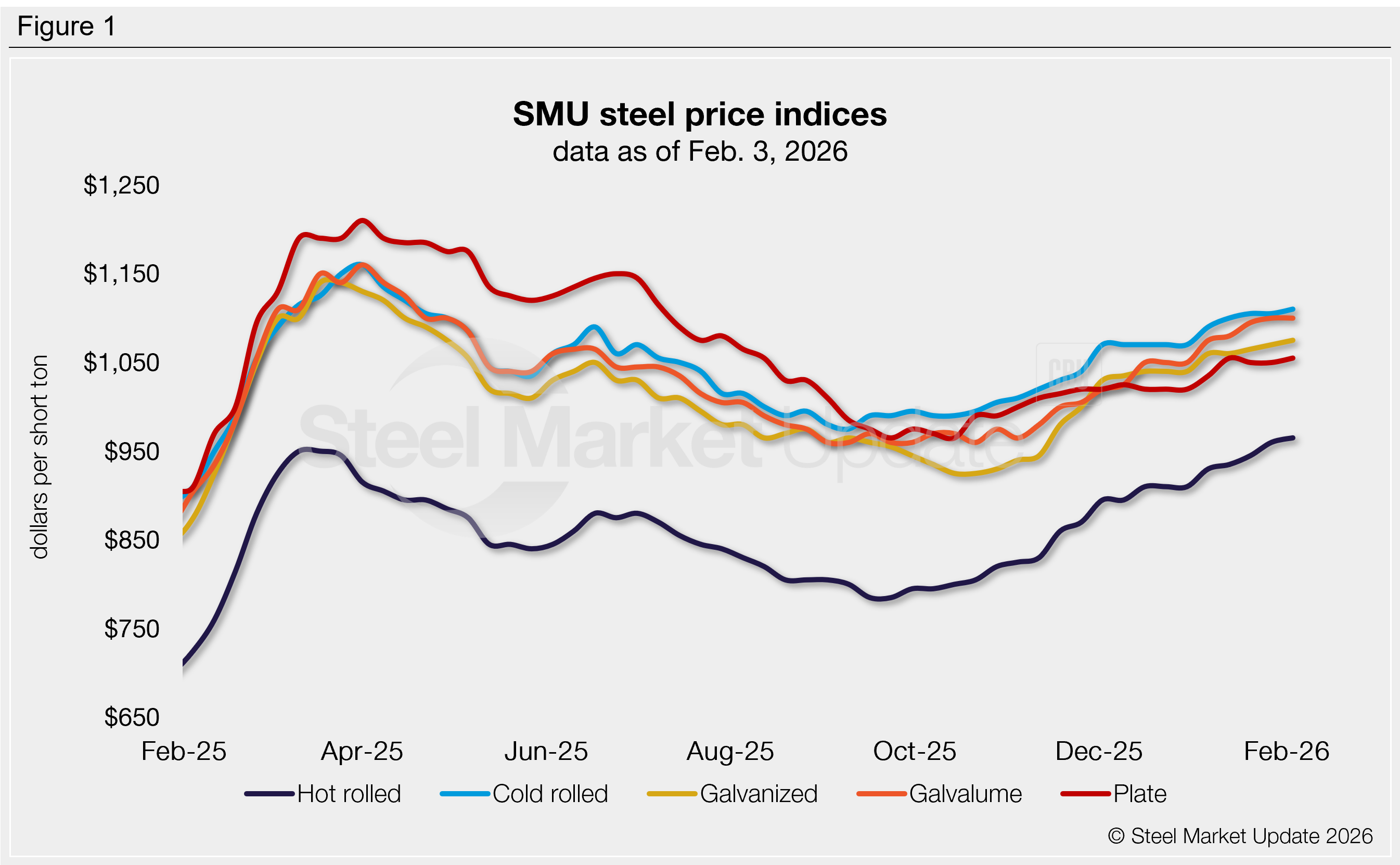

SMU Price Ranges: Sheet and plate prices continue to grind higher

Written by Brett Linton & Michael Cowden

Flat-rolled steel prices inched upward again this week as mixed demand appeared to be offset by limited supplies.

Case in point: SMU assessed hot-rolled coil prices at $965 per short ton (st), up $5/st from last week. Other products were flat or increased by the same amount.

Another notable feature of the market: The spread between our high ($980/st) and our low ($950/st) for HR was only $30/st. Such spreads were typical during pre-Covid years. In the years since, they have often been substantially wider.

It’s not clear whether a pattern of tighter high-low spreads will hold. But another feature of the current market clearly has staying power. Namely, limited supplies and higher tariffs setting a new, higher floor under flat-rolled prices.

SMU will publish updated apparent supply figures later this week. We would not be surprised if they indicate supply is at its lowest since early 2021. Such a trend would match what we’re seeing with import volumes, which have fallen to their lowest levels since late 2020.

Here’s another spread to watch: The gap between HR and plate prices has narrowed substantially. SMU’s plate assessment stands at $1,055/st on average, only $90/st higher than HR.

As recently as September, the spread between HR and plate stood at approximately $200/st. Some market participants predict plate mills might announce another round of price hikes to try to narrow that gap.

“Plate prices are ‘4 sure’ moving up more slowly than HR prices. There’s a really strong chance plate will see hikes soon,” one Midwest service center source said.

SMU’s price momentum indicator continues to point to higher for both sheet and plate products, signaling that we expect prices to increase further in the short term.

Refer to Table 1 (click to enlarge) for our latest price indices and trends.

Hot-rolled coil: $950–980/st, averaging $965/st

The lower end of our range is up $10/st week over week (w/w), while the top end is unchanged. Our overall average is up $5/st w/w.

Hot-rolled lead times range from 5–8 weeks, averaging 6.0 weeks as of our Jan. 22 market survey. We will publish updated lead times on Thursday.

Cold-rolled coil: $1,080–1,140/st, averaging $1,110/st

The lower end of our range is unchanged w/w, while the top end is up $10/st. Our overall average is up $5/st w/w.

Cold-rolled lead times range from 6–10 weeks, averaging 7.6 weeks through our latest survey.

Galvanized coil: $1,040–1,110/st, averaging $1,075/st

The lower end of our range is unchanged w/w, while the top end is up $10/st. Our overall average is up $5/st w/w.

Galvanized .060×48” G90 benchmark: SMU price range is $1,130–1,200/st, averaging $1,165/st FOB mill, east of the Rockies.

Galvanized lead times range from 6-10 weeks, averaging 7.5 weeks through our latest survey.

Galvalume coil: $1,060–1,140/st, averaging $1,100/st

The lower end of our range is down $20/st w/w, while the top end is up $20/st. Our overall average is unchanged w/w.

Galvalume .0142×42” AZ50, grade 80 benchmark: SMU price range is $1,489–1,569/st, averaging $1,529/st FOB mill, east of the Rockies.

Galvalume lead times range from 7–10 weeks, averaging 8.2 weeks through our latest survey.

Plate: $1,030–1,080/st, averaging $1,055/st

The lower end of our range is up $10/st w/w, while the top end is unchanged. Our overall average is up $5/st w/w.

Plate lead times range from 5–8 weeks, averaging 6.0 weeks through our latest survey.

Brett Linton

Read more from Brett Linton