Analysis

February 5, 2026

Final Thoughts

Written by Ethan Bernard & Stephen Miller

SMU’s ferrous scrap survey turns a year old this month. It’s been great to get all of your input on what has been an interesting year for scrap. While tariff news was in the background, prices just bumped along for most of 2025. So where do we stand now?

Well, it seems prices jumped this month as the market is mostly settled. But let’s give SMU’s Steve Miller, and his over 40 years in the scrap industry, a chance to analyze some of the data.

And, as we go into year two, we’d love for more of your opinions as we continue to grow. Contact david.schollaert@crugroup.com to be included in future market questionnaires. Also, if there are any other questions you’d be interested in seeing on the survey, don’t hesitate to drop us a line. (For Premium subscribers, the full results are available here.)

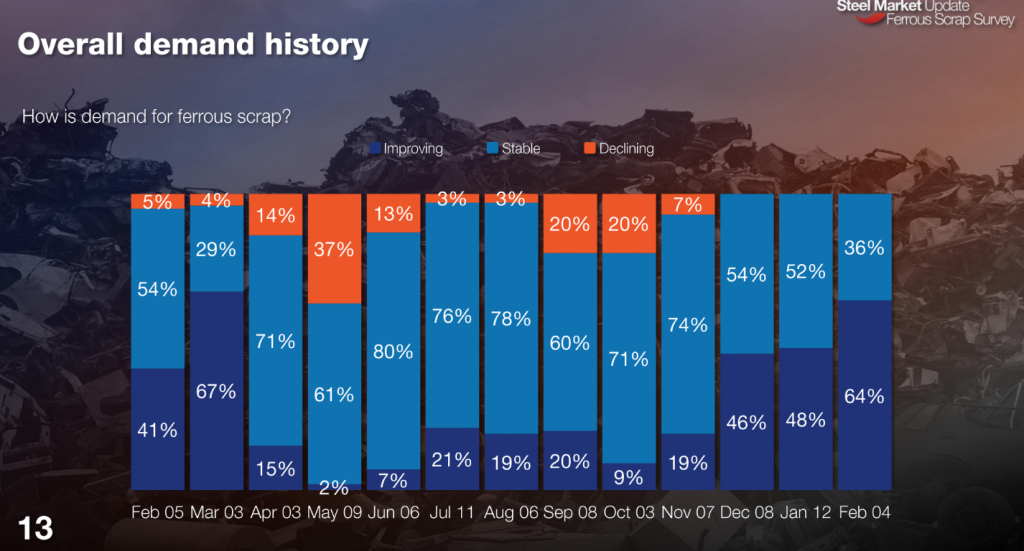

How is demand for ferrous scrap?

The chart seems to indicate participants think the scrap market is in balance when prices are at the higher end. And not in balance when prices are lower. This has been happening on a seasonal basis. During the winter months, scrap prices rise due to reduced supply, and for the rest of the year, they trend downward, flattening out until December. For the last three years, there have been no surges in demand to affect this perceived imbalance.

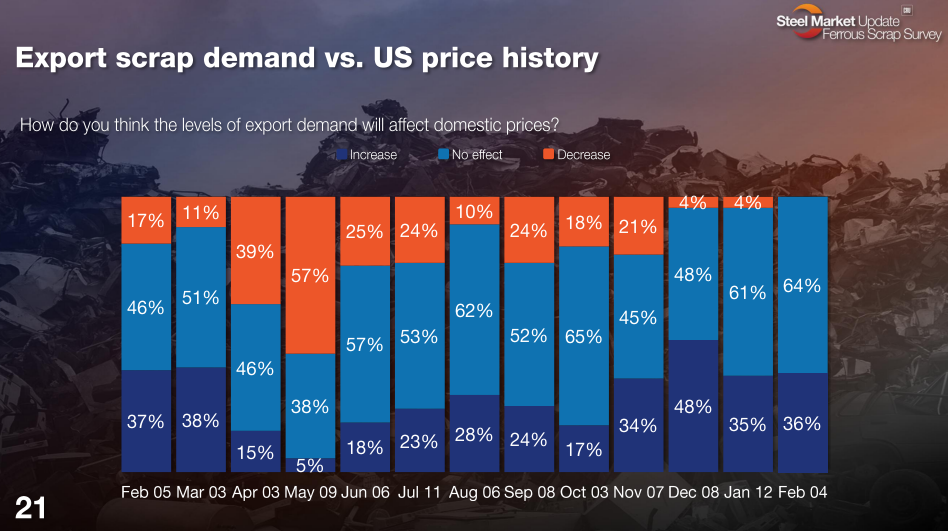

How do you think the levels of export demand will affect domestic prices?

The responses indicate most think export scrap prices have little effect on prices of domestic scrap. Based on 2025 data, this is understandable, as US export scrap shipments have declined. Export scrap demand needs to be much stronger to influence domestic scrap pricing to a meaningful extent. However, the influence could be considered bearish since the lack of usual export activity leaves more scrap available for domestic consumption. It works both ways regarding influence.

Where do you think shred prices will be in February?

The respondents were accurate on this question, as most mill buys on shredded scrap are plus $30 per gross ton (gt) from January. This lands shredded at an average delivered price of ~$455/gt, give or take. There is a sizable minority who thought shredded would spike higher. These respondents are likely from the scrap processor contingent, which views shredder production as limited.

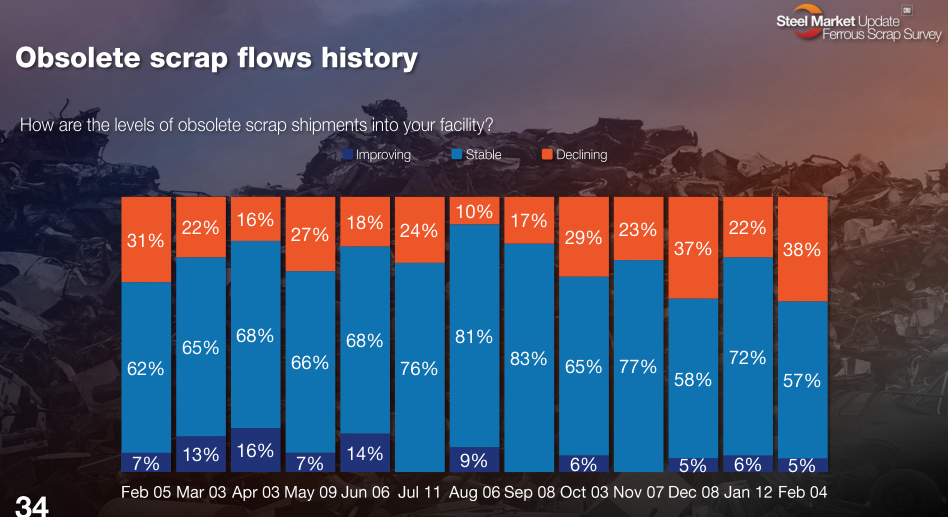

How are the levels of obsolete scrap shipments into your facility?

In a winter when many steelmaking areas have been affected by severe storms and low temperatures, there really has not been a noticeable change in obsolete scrap flows, as reported by our respondents. Based on input from both our scrap seller and buyer sources, the weather has impacted both collections and mill deliveries over the last two months. There were some movements on declining flows in February (38%), but only 22% in January. Go figure!

Tampa bound

We’re less than a week out from the start of SMU’s Tampa Steel Conference. (You can still register here.) Of course, scrap will be featured.

We’ll do a deep dive on raw materials with Matt Bell, president of OmniSource, and Canada-based Sean Cleary, CEO of Strategic Resources. We’ll talk about things like scrap supply dynamics, international and domestic sourcing risks, and evolving input-cost pressures shaping steelmaking. And we’re looking forward to taking audience questions as well.

We can’t wait to see you there!

Ethan Bernard

Read more from Ethan Bernard