Analysis

February 8, 2026

Final Thoughts

Written by Michael Cowden

I’m going to play devil’s advocate for a narrative that has become the consensus for much of the US steel market. You know how it goes. Domestic steel prices will continue to go up despite uneven demand thanks to low supplies stemming in large part from tariffs and limited import competition.

That’s been the case for months now. Will it continue to be?

To explore that question, I’m going to go through some of the data we typically highlight from our steel market surveys. Namely, questions around pricing and demand.

I’m also going to get into some of the survey questions we ask steel traders. It’s useful data that we don’t often highlight in the newsletter. And it’s worth your attention because it can, I think, be a leading indicator.

A quick note on format: I’m going to share a few slides from our most recent steel market survey. You can click on the slides to expand them. I’m also going to include comments from survey respondents (who always remain anonymous) in their own words.

Another note: The page numbers in the slides below correspond to where you can find them in the full survey deck. Our premium subscribers can find the full deck here. If you’d like to upgrade from executive to premium so you can see proprietary data like this, contact us at smu@crugroup.com.

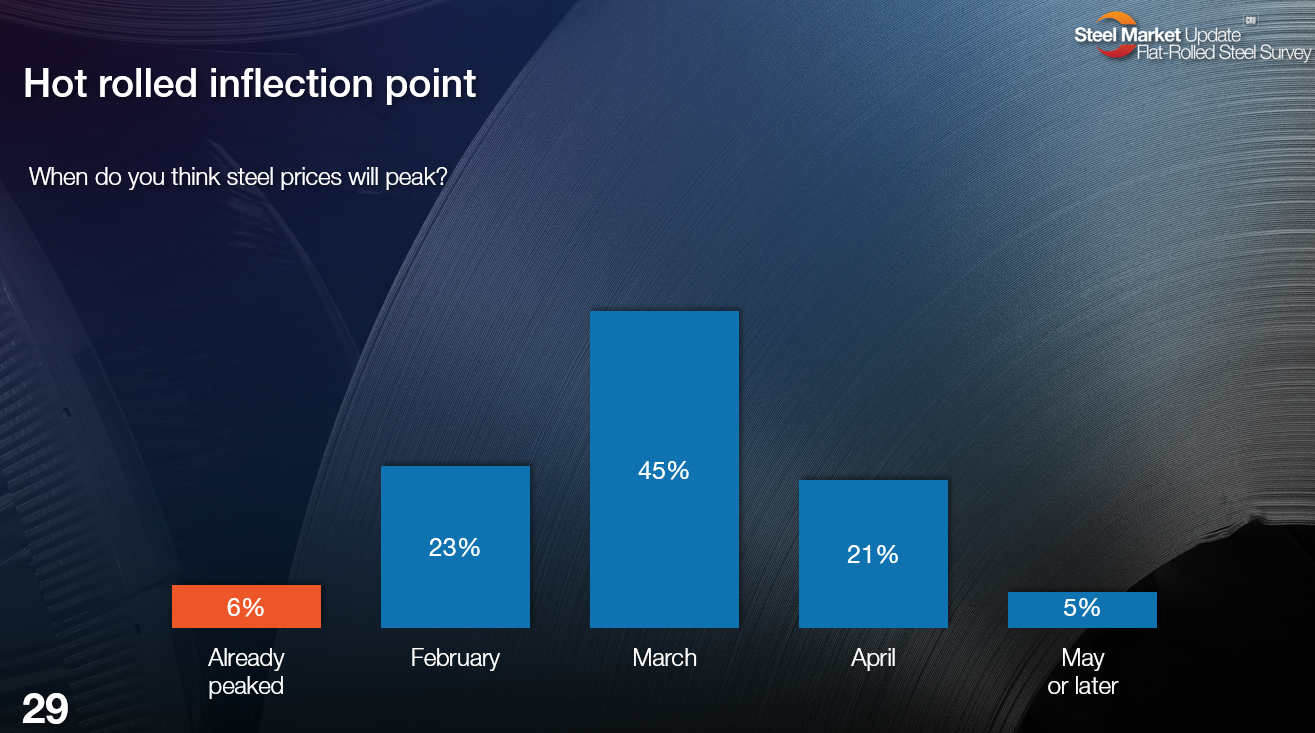

When will flat-rolled prices peak?

Let’s start with a question we typically focus on: when survey respondents think flat-rolled steel prices will peak.

As you can see in the chart below, most survey respondents think steel prices will peak (or have peaked) this month (29%) or next (45%). But a significant minority (26%) see the rally that got underway in Q4 extending into Q2.

Here is what some of them have to say:

Already peaked

“The last two increases have not really stuck, and demand hasn’t increased enough for them to try another one.”

February

“We aren’t there, but we’re getting there. If I’m being honest, $1,000/ton is just crazy in this market.”

“I believe the price increases are to soften the decreases when they start in March, to ensure we do not hit mid-$600s again.”

“I just can’t see prices going much higher until demand picks up.”

“Buyers are starting to hold back. The cycle has almost run its course.”

March

“I don’t think it has enough steam to make it into Q2.”

“I do not think there is much more room to go up. But there continues to be strength.”

“I think they are beginning to level off now.”

“All the supply side issues will have been addressed, other than late deliveries.”

“Still a little upside left, but demand is still too fragile.”

“Everything but demand is in place for sustained price increases.”

“Running out of room between domestic pricing and imports.”

April

“Between low imports and better demand as the weather improves, expect to see prices continue to edge higher.”

“Likely to rise on the back on scrap that could rise into the second quarter.”

“The demand trend looks to be getting some legs.”

“Seems like the increases have legs.”

“Lack of imports and tariffs will continue to push prices upward.”

FWIW, those who selected “May or later” aren’t showing their cards and telling us why they think that.

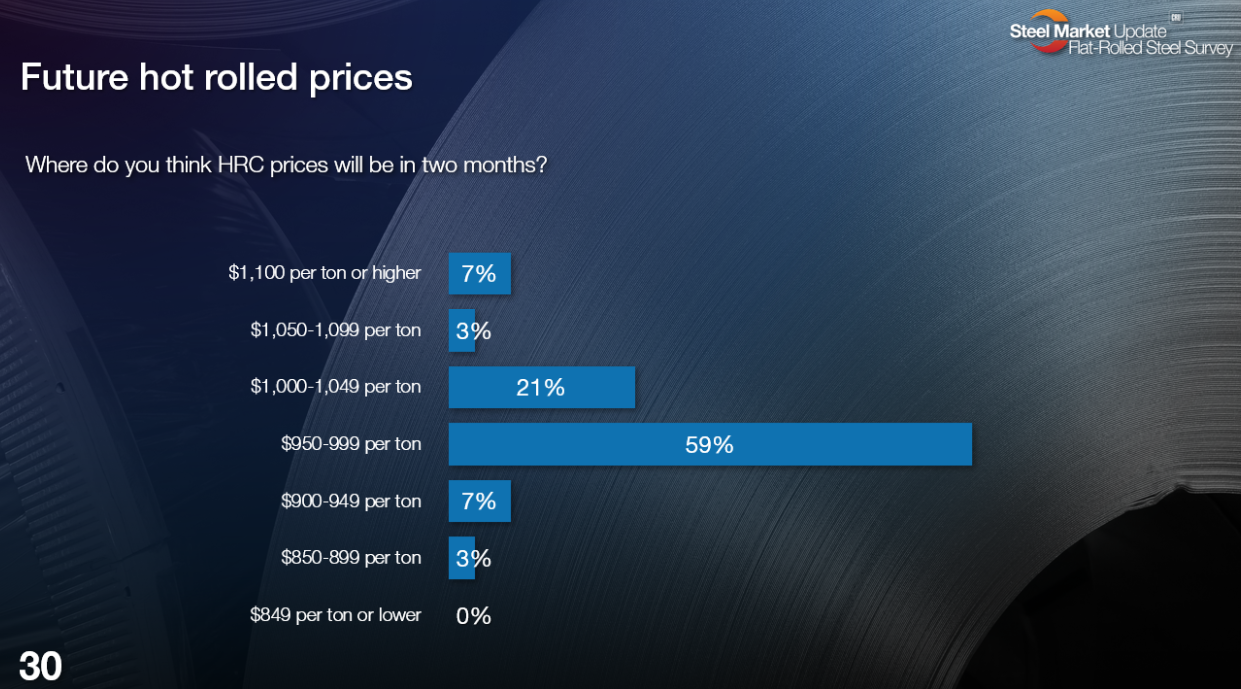

Where will HR prices be at the start of Q2?

Now let’s turn to where survey respondents think prices will be two months from now. In other words, at the start of Q2:

SMU’s HR price assessment stands at $965/st on average now. (We’ll assess prices again on Tuesday.) Most survey respondents (59%) think that prices will be in roughly the same ballpark two months from now. Only 10% see prices falling below $950/st on average. And nearly one-third (31%) see US HR prices starting out the quarter above $1,000/st.

Here is what some of them have to say:

$850-899

“Demand is not there in my opinion.”

“We might be an outlier group. But we think this thing reverses course in earnest as spring/summer rolls around.”

$900-949

“I think it will dip down and then move higher.”

$950-999

“Mill backlogs and upcoming outages should keep prices firm for the next 60 days.”

“It seems to me that the most likely reason that prices will drop is competition from imports. And I think we’re just about at the point where imports will start to be an option.”

“If price gets too high, imports will become more attractive.”

“Stock levels are getting healthier. Demand won’t support a further uptick.”

“Algoma out was a shock. But mills will re-align with modest demand.”

“I think demand will level off.”

“The market seems to be ready to plateau. Demand is unchanged.”

$1,000-1,049

“On the back of scrap, again.”

“It has a little more room to run.”

“Gut feeling.”

“Once it breaks $1,000, the market sentiment will balk.”

“Pricing has been stagnant for too long.”

“Nothing to stop the rise, and more maintenance outages are being announced for the spring.”

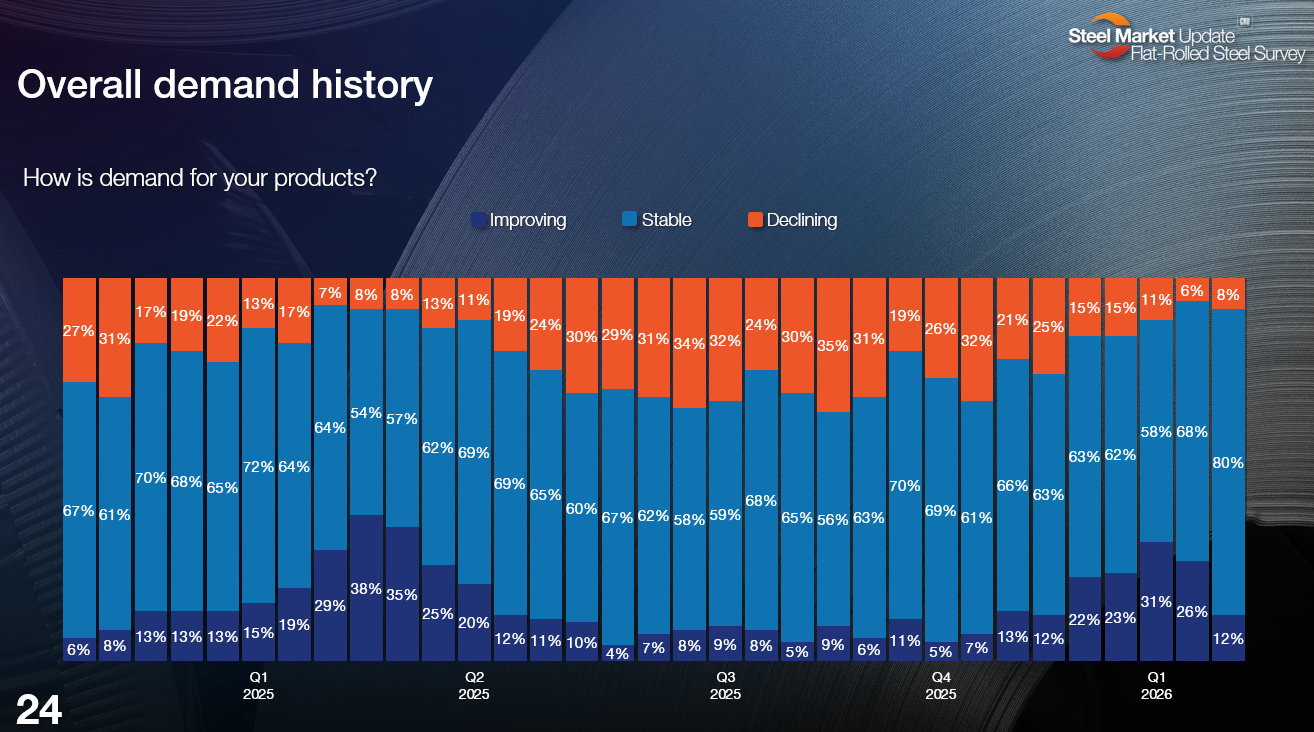

How is demand?

You’ve probably noticed that more than a few comments mention that demand is not exactly stellar. That’s reflected in our survey data as well.

And if you’re looking for cracks in the long upward trend we’ve seen in prices, this might be one.

The dark-blue bars in the chart above indicate the percentage of survey respondents who told us their companies were seeing improving demand. That number started ticking upward early in Q4 and peaked at 31% in January. The number has since dropped to 12%.

This is hardly a sign that the sky is falling. Nearly 80% of respondents say demand is stable, which is not a bad result.

I note the decline in those reporting improving demand because we saw a similar pattern in Q1-Q2 of last year. Recall we saw prices surge in Q1 of last year and then fall for most of Q2 and Q3. In 2025, the number of people reporting improving demand rose into the 30s% in Q1 and then fell back in Q2.

Cracks in the upcycle?

I also note the trend we’re seeing in overall demand because there are arguably signs of cracks in some of the other data we track.

Take spot price negotiation rates. Broadly speaking, mills still have pricing power. Most are not willing to negotiate lower spot prices. But when you drill down into the numbers by product, the picture becomes a little more complicated.

Survey respondents, for example, tell us the mills are even less willing to negotiate lower HR and cold rolled (CR) prices now than they were in January. But they also tell us that they’re finding producers more willing to talk price when it comes to coated products.

It’s a similar story on lead times. They dipped a little. I wasn’t expecting that. Yes, they slipped from relatively high levels. And, yes, it’s possible it’s just noise. We could very well see them extending again should weather-related issues be reflected in our next market survey.

In other words, it’s possible all of this – a slowing down in demand growth, mills more willing to negotiate lower prices on coated products, and a modest decline in lead times – is just noise. But it’s also worth considering whether such data points might be telling the story of a market nearing a plateau.

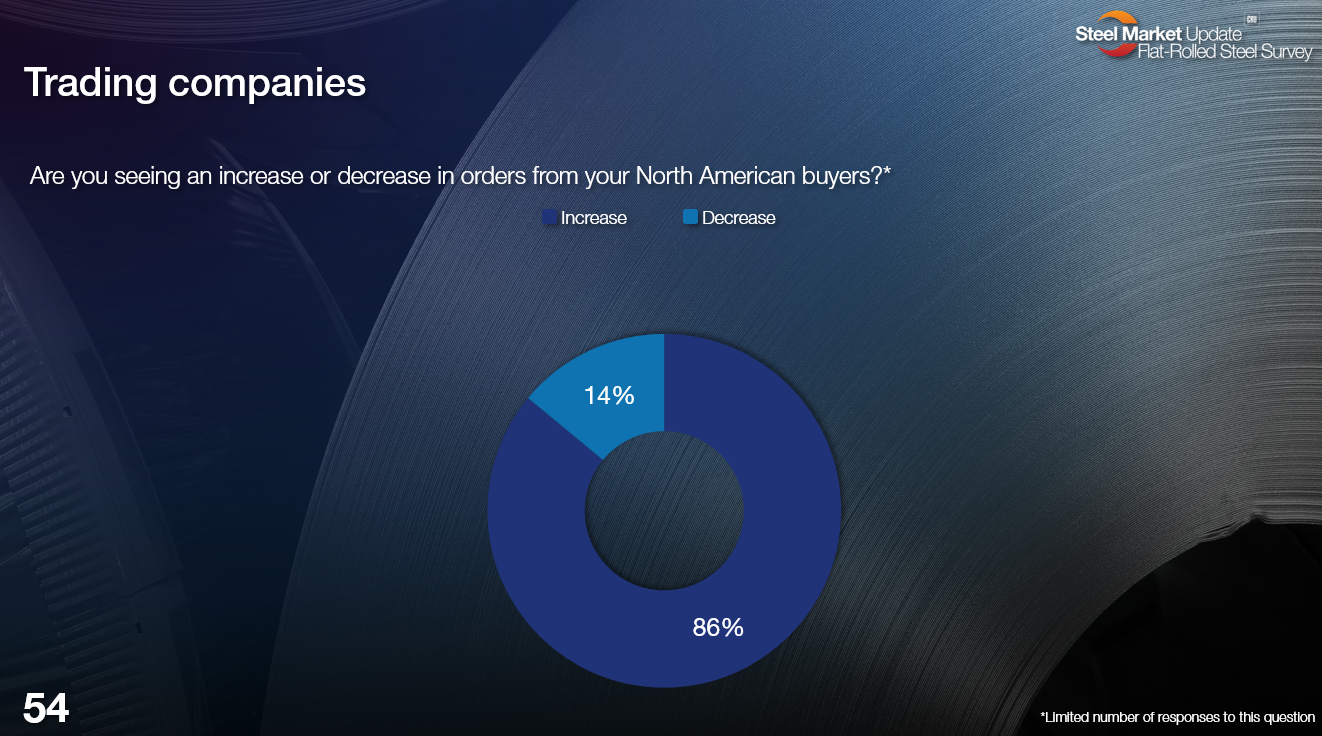

Imports making a (modest) comeback?

Let’s take the narrative about import volumes and overall supplies remaining low, for example. There can be no doubt that’s been the case. Just look at data on apparent supply for November, which is at its lowest level since February 2021 – a month that saw huge price gains. Current import volumes, meanwhile, stand at their lowest levels since late 2020.

But will import volumes remain at such historically low levels?

I ask in part because of survey results like the ones below:

Nearly 86% of traders who responded to our survey said they are seeing an increase in orders from their buyers in North America. Sources mentioned that material from Indonesia, South Korea, Vietnam, and Taiwan could compete with US prices, even once tariffs are factored in.

If you drill down into the results and comments, you’ll see that trader respondents are hardly predicting a flood of material into the US market. About 70% say they can offer competitive CR prices. For HR, that number is closer to 30%. And what they’re seeing is interest in certain specialty or higher-grade products.

But even a modest uptick in interest in foreign steel from US buyers represents a change from a long period in which there was almost no interest in imports, survey respondents said. Material ordered now won’t arrive until this spring. But it’s worth considering what the supply-demand balance could look like if import volumes rebound even slightly from current levels.

Which story is right?

Most (but hardly all) of the respondents to SMU’s steel market surveys are steel buyers. So our results will mostly reflect their view of the market.

If you think buyers are wrong, maybe you think they’re underestimating the impact of upcoming outages or other bottlenecks. U.S. Steel, for example, is taking a 100-day outage to reline the No. 14 blast furnace at Gary Works in northwest Indiana. And that comes on top of shorter, more typical spring outages. Individually, such spring outages might not amount to much. But taken together, they will be meaningful.

And maybe our survey data hasn’t yet captured the impact of weather-related production issues and delays in recent weeks. If that’s the case, buyers who think the market is poised to cycle down within the next 60 days could be surprised. Maybe they’ll be caught short steel if the rally we’ve seen continues into Q2.

Let’s also remember that the rally we saw last year ended abruptly in Q2 not because of any of the usual factors. It ended because President Trump’s “Liberation Day” tariffs – announced on April 2 (so as not to be confused with April Fools’ Day) – shocked the market.

But if our survey respondents are right, some of the talk of hot band at a grand (and I’ve been one of those talking about) might age as well as talk of hot band at two grand in 2H 2021.

Another thing I’ve been noticing: We’ve seen more bullishness from mills and larger service centers and distributors. Smaller and mid-sized buyers, meanwhile, appear to be more wary. You could be cynical and say that everyone is their own spin machine. I also wonder whether both sides are saying what they think is true – it’s just their experiences of the current market are different.

Make your voice heard!

Do you like what you read above because it matches what you see in the market? Are you shaking with rage because it doesn’t? Either way, make sure your voice is heard and your experience is reflected in our survey. Reach out to us at smu@crugroup.com and we can get you signed up to participate in our next survey.

Tampa Steel Conference

It’s going to be another record year for the Tampa Steel Conference this week, with nearly 600 people attending. If you’re going, we can’t wait to see you soon in Florida. If you haven’t registered yet, it’s not too late. You can see the latest agenda here and register here.