CRU

February 12, 2026

CRU: US prices move higher on supply squeeze

Written by Josh Spoores

This news item was first published by CRU. To learn about CRU’s global commodities research and analysis services, visit www.crugroup.com.

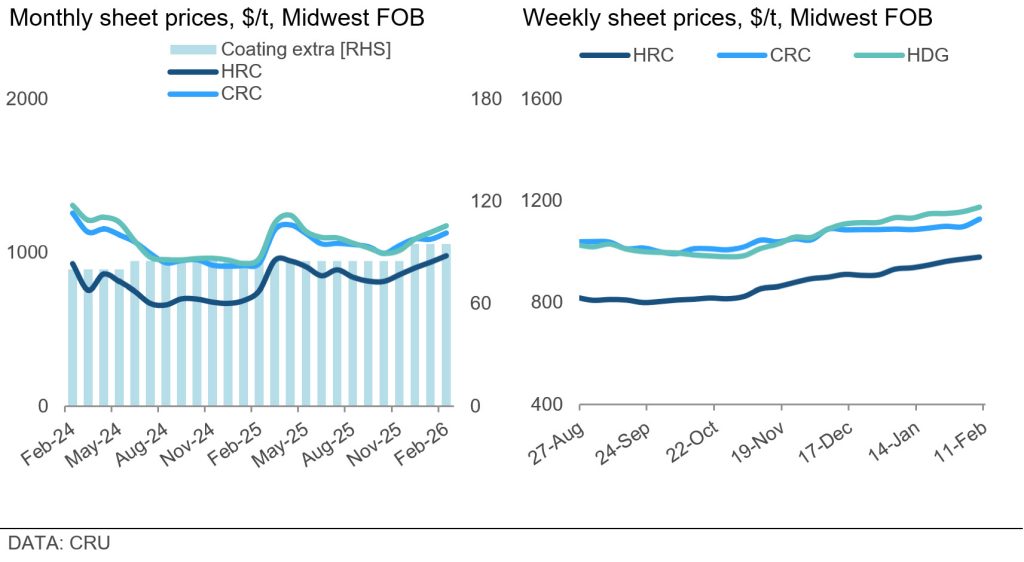

US Midwest sheet prices have continued to rise with gains of $40 per short ton (st) from our Jan. 14 assessment. Prices are now up $136-178/st from the lows assessed this past September and October.

Higher prices continued to be supported by tight supply, primarily for HR coil. As we covered last month, imports remained low, due to low domestic prices in 2025 Q3 and Q4. These low prices limited the competitiveness of imports, inclusive of the 50% S232. Today, we continue to see the results of this as import arrivals so far in January were down just over 400 kt y/y.

As domestic buyers have increased orders, mills have fallen behind in production for various reasons including recent winter storms, production issues, and delays to slab supply, among others. Due to this, lead times remained extended with HR coil near six weeks, while CR and HDG coil are near seven weeks, per Steel Market Update. This increase of orders at mills has come about alongside seasonal demand gains. Buyers have noted that demand is currently higher than levels seen before the year end. Additionally, some service centers have reported that end-users in construction and some manufacturing segments have increased production plans for early 2026 Q2, requiring higher order levels at mills today.

In Mexico, domestic sheet prices increased m/m due to improved demand amid lower domestic supply. According to market participants, demand has improved on the back of restocking in the distribution sector, while industrial sector restocking remained weak. In terms of trade, imports from Asia have decreased y/y. Mills continued to increase HR coil prices in Mexico, this time by $15 metric ton (mt) at the beginning of February to $785/mt FOB Monterrey, with lead times for HR coil extending to around 5 to 7 weeks.

In Brazil, domestic sheet prices decreased in February back to December levels, as supply availability remained high, particularly from imported material, while demand remained stable. According to some market participants, there is an expectation that the antidumping investigations for CR coil and HDG will result in new duties, but it will take some time for imported volumes to reduce in the coming months. The price premium for Brazilian HR coil prices over Chinese import parity prices increased only slightly m/m. For imports with a quota in the temporal quota system (duty of 10.8%), the premium increased from 20.4% to 20.9% m/m. For imports without a quota (import duty of 25%) the premium increased from 7.4% to 7.8% m/m.