Analysis

February 22, 2026

Final Thoughts

Written by Ethan Bernard

This week’s Friday surprise came from the US Supreme Court and its decision to rule again President Trump’s International Emergency Economic Powers Act (IEEPA) tariffs.

POTUS was quick to respond, threatening a new set of tariffs. One crucial thing to keep in mind: None of this drama impacts Section 232 steel tariffs, which remain in place.

But while tariff developments might be garnering the headlines, our latest steel market survey results show industry participants continuing to grind away with day-to-day business.

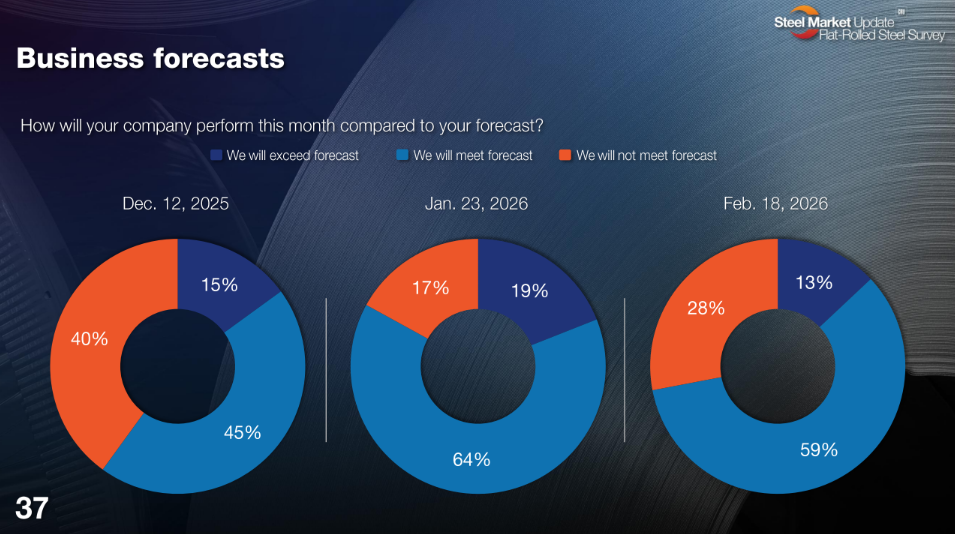

Something that jumped out at me was the slide on business forecasts. Our latest market check shows 28% of survey respondents reporting they will not meet their forecast this month, up from 17% last month.

One respondent wrote:

“We met forecast, but barely. Things still aren’t what I would consider ‘good’ by any stretch.”

It wasn’t all doom and gloom, though. We got a wide variety of viewpoints and perspectives on subjects like tariffs and pricing. Keep on reading to get a glimpse of what others were thinking ahead of Friday’s Supreme Court decision.

Want to share your thoughts? Contact david.schollaert@crugroup.com to be included in our market questionnaires. (Editor’s note: the numbers in the slides below reflect their order in the full survey deck.)

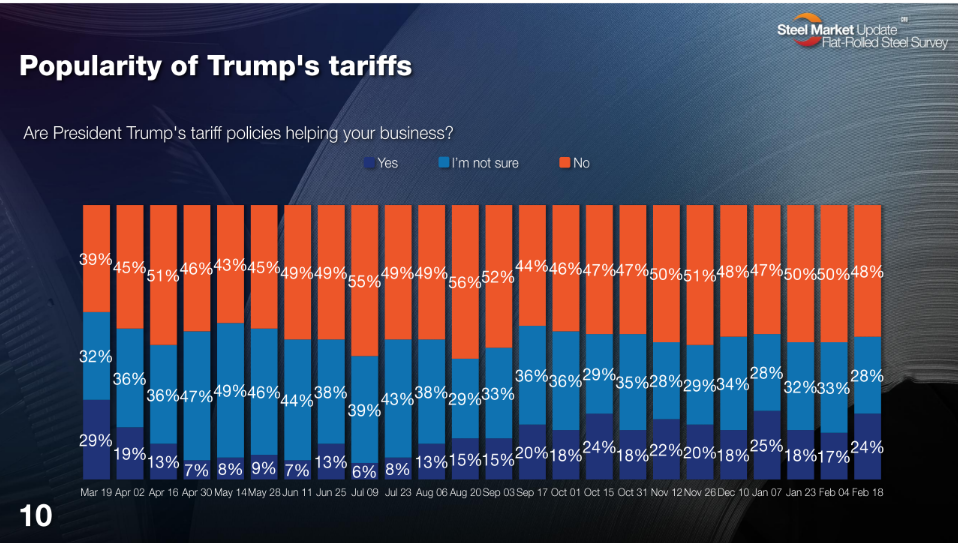

Are President Trump’s tariff policies helping your business?

“Raising input costs does not help the cause of domestic manufacturing.”

“Not sure the current tariff model is sustainable. Lots of pressure from manufacturing customers on costs.”

“Prices remain elevated.”

“His policies are definitely hurting our business.”

“One of our strengths is the import of coil and that was severely affected in 2025. We expect that to continue in 2026, so we’ll evolve and focus on our domestic partnerships.”

“If there is an effect, it’s minimal.”

“They are giving mills the ability to have overly inflated prices based on the limited supply, which is hurting demand.”

“Import offers are still cheap and plentiful.”

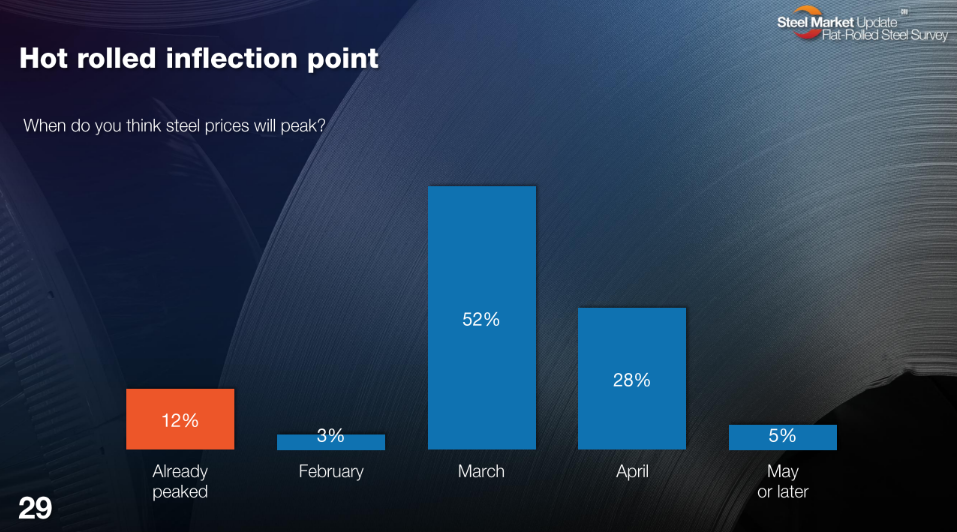

When do you think steel prices will peak?

“Demand will increase.”

“The last two increases have not really stuck, and demand hasn’t increased enough for them to try another one.”

“Running out of room between domestic pricing and imports.”

“Prices are beginning to level off.”

“I keep hearing about shortages in other products like beams. Feels like continued upward pressure.”

“Data centers are driving demand.”

“I thought we would have peaked by now, but we’re not there yet. Close, but not quite there.”

“Mills holding the line as long as possible.”

“Demand is no longer driving this market.”

“Do not believe prices get over $1,000, so March seems logical for a peak coming into the summer slowdown.”

Where do you think HRC prices will be in two months?

“What is going to stop pricing from continuing to rise? If the mills remain full at the current price point, what is to stop them from continuing to push pricing upward?”

“Upticks being announced on scrap basis. But there is no long-term indication this will stay or move upward further as supply rebalances.”

“Based on demand, I don’t feel we are going to move much further up.”

“I originally thought $950-$1000, but looks like we will pass that mark.”

“Any higher and you will start to receive more imports to drive the cost down.”

“HRC demand is strong on many fronts.”

“Input costs to go up.”

How will your company perform this month compared to your forecast?

“We just missed our volume target.”

“We’re conservative.”

“Resistance to price increases in the market.”

“US market due to tariffs has hurt our ability to be competitive.”

“Weather impacted shipments.”