Analysis

March 8, 2026

Final Thoughts: A strong market collides with war uncertainty

Written by Michael Cowden

Prices are moving up, and lead times are moving out. And most people expect them to continue to do so into Q2, according to our latest survey results.

As we get closer to summer, however, some market participants think imports could become more of a factor – limiting the upside for domestic prices and perhaps even forcing them lower.

And then there is the big wildcard: The Iran war.

Does war uncertainty trump tariff uncertainty?

We didn’t ask any questions specifically about the Iran war in this survey. But the subject came up repeatedly in the comments.

It’s easy enough to understand why. When I was writing this on Sunday, mainstream news outlets were reporting the Trump administration was considering a “special operation” to take Iran’s uranium. Meanwhile, oil prices looked set to top $100 a barrel.

As I see it, the big question is this: Does the Iran war put a damper on an otherwise solid domestic steel market? Basically, do we see something like what we saw last year when a strong Q1 was derailed in Q2 by confusion surrounding “Liberation Day” tariffs?

The steel industry has gotten used to tariffs. And business seems to be mostly plowing ahead despite tariff uncertainty. But what about war-related uncertainty? That’s a question that’s hard to immediately answer.

Our parent company, CRU, has had some really good stuff on where things stand in the Middle East. One example is here. And, sure, the US steel industry is more protected than the aluminum industry because there is more domestic steel production capacity. (AMU has some good coverage on the extent to which aluminum has been impacted here.) Also, North America is, fortunately, less reliant on imported energy than other regions – notably Asia and Europe. Even so, if oil gets to $100/barrel, that will obviously flow through to fuel prices and freight costs to a greater degree than what we’ve seen to date.

So, let’s make that important caveat, the survey data below reflect a period after news of the initial strikes on Iran had broken – but before the potential length of the conflict, and the potential impact on energy prices, had come into focus.

Editor’s note: You can expand all the slides below by clicking on them. The page numbers correspond to where our premium subscribers can find them in the deck with our latest full survey results, which is here. Results from past surveys are here. (And if you’d like to upgrade from an executive subscription to a premium one, let us know at smu@crugroup.com.)

When will the market peak?

The consensus that prices will be stronger for longer is no longer an outlier opinion. Look at the chart below:

Most survey respondents (68%) think hot-rolled (HR) coil prices won’t peak until Q2. And even if a substantial minority (25%) think prices will peak later this month, only a fraction (7%) thinks prices have already peaked.

What a contrast to our first survey of the year. In early January, which feels like a lifetime ago, only 19% thought HR prices would continue rising into Q2. (You can find that survey and all past SMU survey results here.)

Here is what respondents to our most recent survey had to say about when they thought the sheet market would peak.

Already peaked

“Demand is still soft. Any further increase would allow imports to come in and take away from domestic mills.”

March

“I thought for sure we would have peaked in January, but here we are…”

“The impact of war sentiment will lower demand.”

“I don’t feel demand is strong enough to sustain increases the mills are pushing out. I feel imports are going to become a factor due to mill greed.”

“Prices starting to exceed demand.”

“Seems we pulled March and April demand forward with January and February spot transactions.”

“Prices will fluctuate around their current levels due to tariffs propping prices up with mixed demand.”

“I expect the Section 232 percentage to be reduced.”

April

“I thought March but now think prices will stay high through the Iran issue.”

“Current geopolitical risks could extend this to a later date. If these risks don’t extend, pricing is getting to a point which could impact demand.”

“Demand doesn’t support the increases in Canada. However, Canadian mills can ship to the US and make money/absorb the tariff.”

“Everyone is already concerned about summer demand.”

“Import arrivals will create peak pricing in April.”

“I don’t think it has enough steam to make it through Q2.”

“Momentum carries into April, but shades of summer will begin to affect the market in May.”

“We need a demand spike to push the peak out.”

“Too much uncertainty.”

May

“Still many market dynamics yet to unfold, and we have not even hit the seasonal demand increase with warmer weather.”

“I think the war will keep them elevated a little longer.”

“War casts every previous assumption into doubt.”

“Demand will increase.”

“All bets are off from (the war in Iran).”

June or later

“Seasonal demand adds to supply limitations (domestic and imports). That will create a tight supply market.”

“Uncertainty in release of demand, so expecting a gradual increase.”

Where will HR prices be in two months?

Another question we always ask is where people think prices will be two months from now. Here are the results from our most recent survey:

What immediately stands out is this: A clear majority (61%) think HR prices will be above $1,000/st in May. That’s a massive change from early January, when only a minority (17%) thought HR prices would be above $1,000/st in early March.

Hey, let’s face it. What most think will happen doesn’t always happen. (That’s why news matters.)

What also stands out is that only seven percent of respondents think HR prices will breach $1,100/st. In other words, they think the pricing upcycle has limited upside.

Are they right about that? Only time will tell. But here is how some explained their thinking.

$940-949

“We still are sticking with our theory/belief that pricing will peak in Q1 and then retreat in Q2 as imports roll in.”

“Demand is weak. Prices are artificially high. Mills will eventually cave.”

“Trump is lowering the tariff on steel because of the feedback he is getting from automotive.”

$950-999

“Imports arrivals will have increased and filled the gap between demand and availability.”

“Demand is still soft, any further increase would allow imports to come in and take away from domestic mills.”

$1,000-1,049

“Momentum and March/April is normally the high point of the year.”

“Demand will still increase from here.”

“Current quote trends from the mills for hrc spot.”

“Very slow increases over the next several weeks.”

“Demand is still ramping up.”

“I feel imports are going to keep prices from moving up much further. We will see prices peak soon, then begin to decline.”

$1,050-1,099

“Current momentum. Thought foreign would soften the market. But sounds like some deals are being pulled.”

“It will go up as long as people buy. They will keep buying for now.”

$1,100 or higher

“Demand increase.”

Survey says

I typically go into depth on those two questions about pricing expectations. Below are some other survey results that caught my eye.

For starters, this is the longest price upcycle we’ve seen in a while. It started early in Q4 and has continued for much longer than the big upcycle last year, the one cut short by Liberation Day. (There is perhaps a theme here about unexpected government interventions.)

And it’s not just mills raising prices. Most service centers have been raising prices right along with producers:

If the Iran war has a negative impact, the chart above might be where it shows up first. Rewind to last year, and the percentage of service centers raising prices dropped almost immediately after “Liberation Day” on April 2.

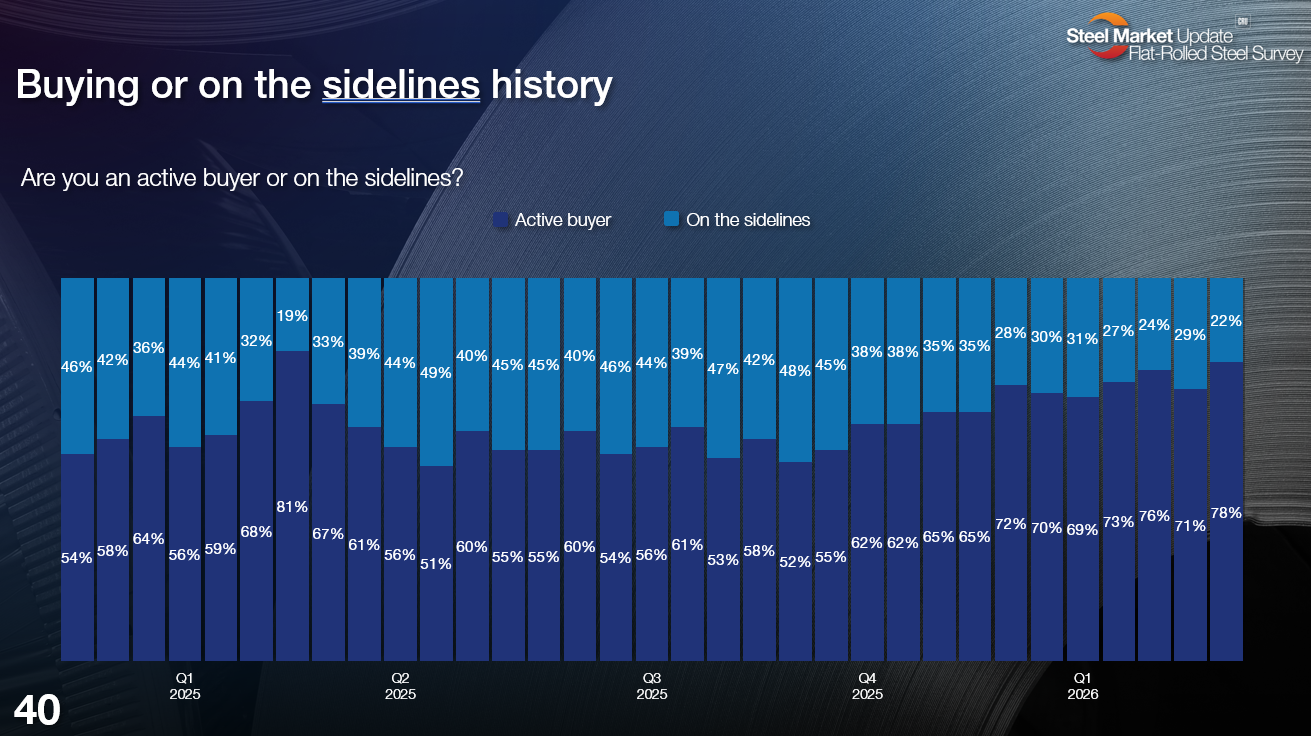

If prices don’t fall, this chart on the rising number of active steel buyers might explain why:

Last summer, when HR prices were mired in the $700s/st, only about 50% of buyers reported they were active in the market. That number has slowly but steadily crept higher and now stands closer to 80%.

Another reason why sheet prices might continue to rise? Sheet inventories might come in relatively low again in February.

Some context: January service center sheet inventories this year (58.5 days of supply) were notably lower than inventories in January 2025 (66 days of supply).

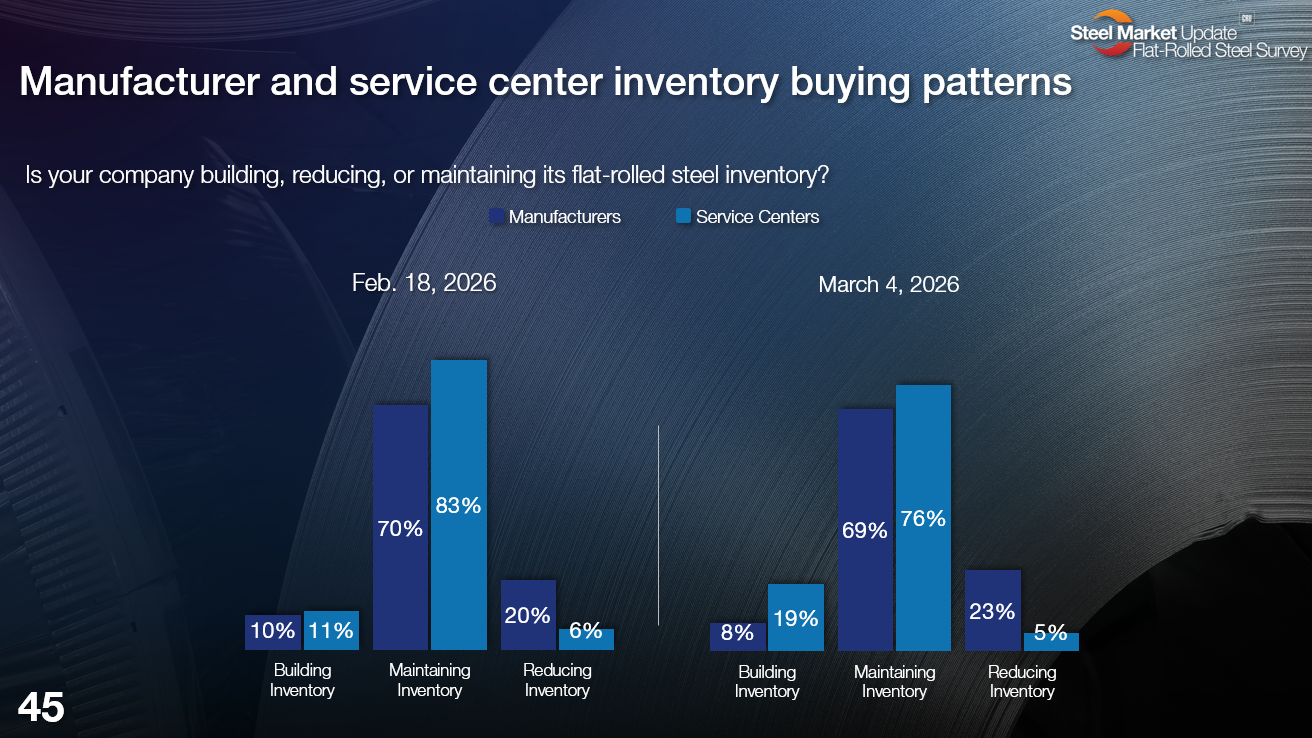

And look at this chart on inventory buying patterns:

Most steel buyers are simply maintaining or even reducing stocks. Few are building them.

Does that translate into lower inventories? We’ll find out soon enough. SMU will release February inventory data to our premium subscribers on Monday, March 16.

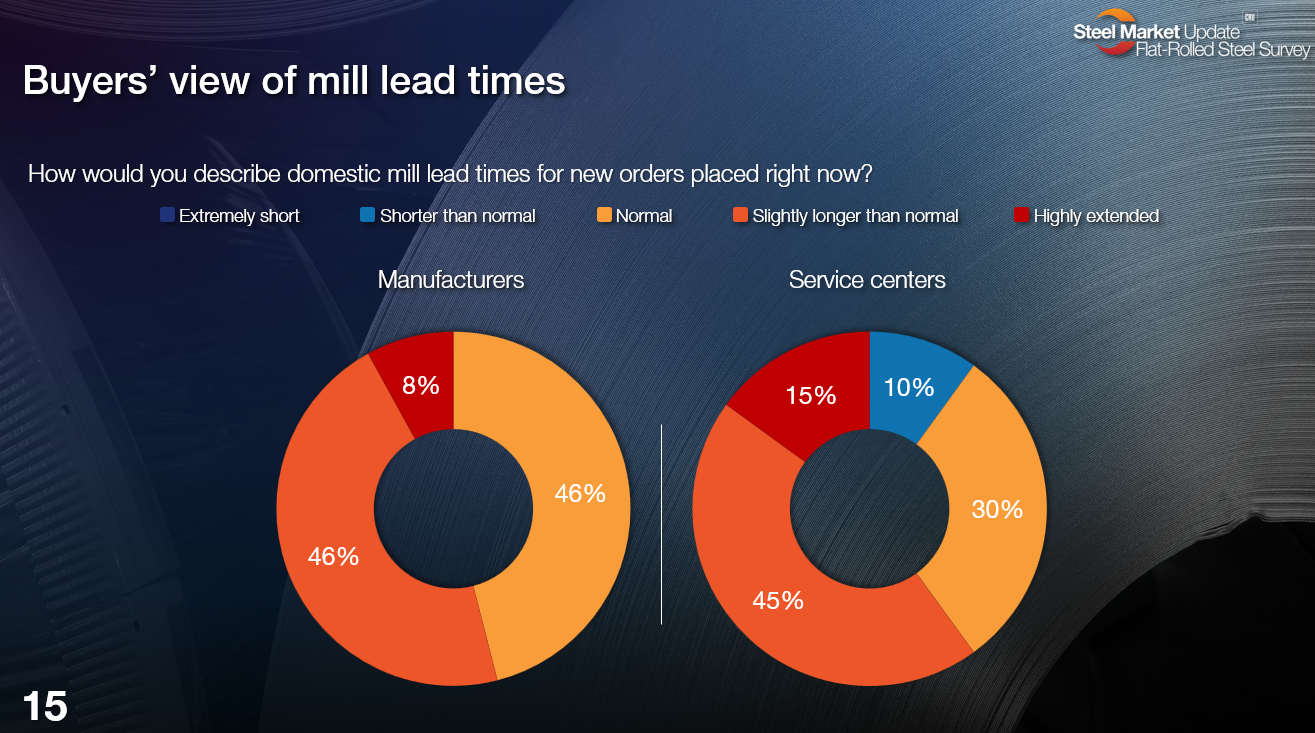

This isn’t Q1’2021. We’re not at a point where lead times are longer than inventories.

But lead times are already extended. And we’re seeing increasing numbers of steel buyers reporting lead times as longer than normal or even highly extended.

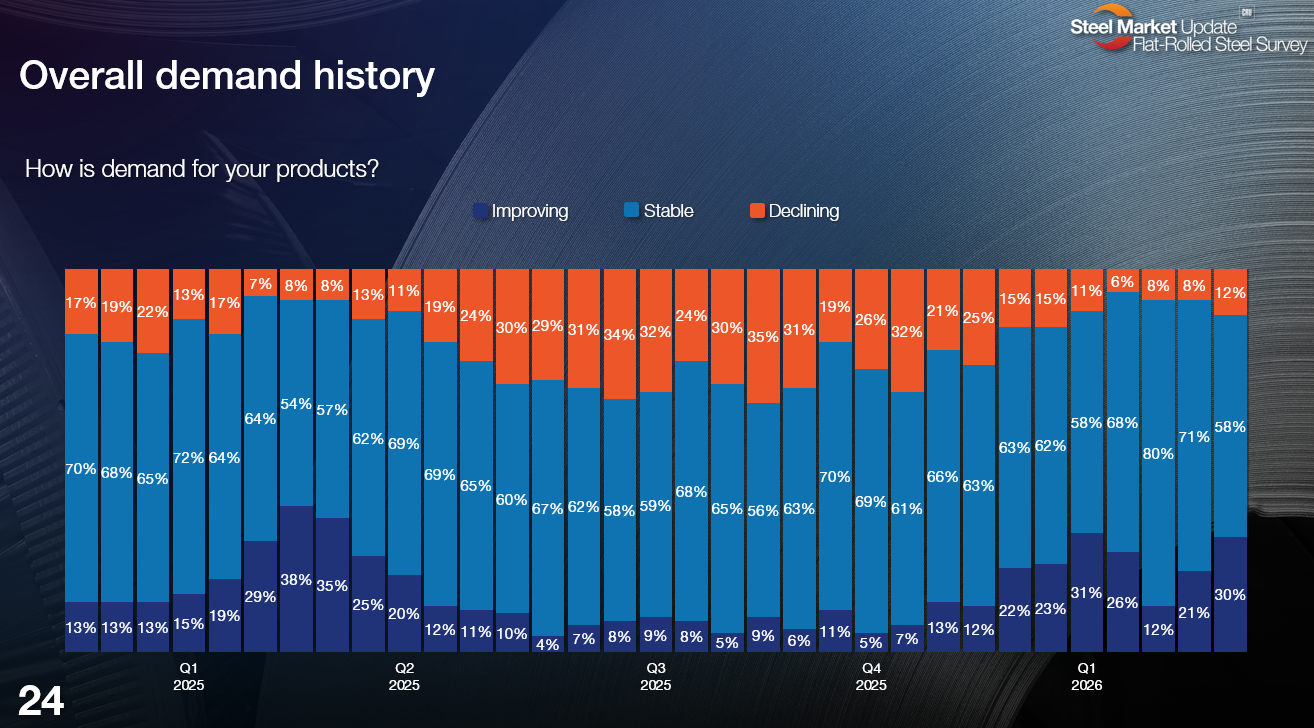

Meanwhile, after a dip earlier this year, we’re seeing more people reporting that demand is improving:

To be clear, most (58%) characterize demand as stable. And some (12%) see it as falling. But a significant minority (30%) reports improving demand. That’s a lot better than much of last summer and early fall, when that “improving demand” figure was routinely in the single digits.

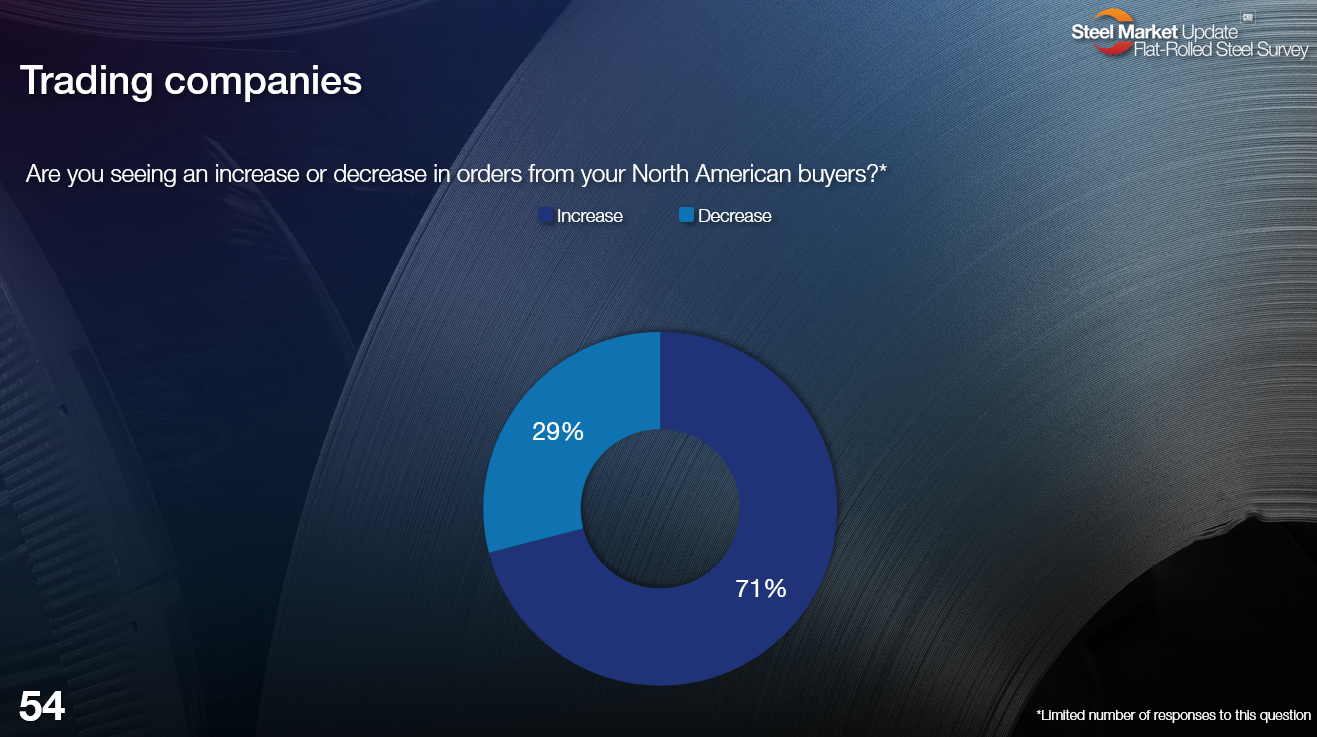

One question worth asking is whether imports could get a greater share of that demand.

I say that because more than 70% of trading companies responding to our survey see increased demand from North American customers. Compare that to about 40% at the beginning of the year.

Even so, a lot depends on product. About 40% of trader respondents said they could offer competitive prices for imported HR. When it comes to CR, that figure jumps to more than 80%.

Takeaways

What are my takeaways from the data and comments above? Broadly speaking, many companies expect demand to increase, especially as the weather warms. But some are still struggling with weaker business conditions.

People expect HR prices to hold at or above $1,000/st into Q2. But there are some fears that higher US prices could attract imports, even with a 50% Section 232 tariff in place. And there are scattered concerns that Section 232 tariffs could be reduced because of pushback from key consuming industries, notably automotive. Such factors help explain a consensus that prices could dip as we get closer to summer, a time that is typically seasonally weaker to begin with.

And, again, the big wildcard: The length of the Iran war and its impact on the market. Will the conflict lead to a pricing upcycle that lasts even longer and moves even higher than expected? Or could an overheated domestic market and widespread geopolitical uncertainty chill demand? Those questions are beyond the scope of our surveys right now. But we will be asking you more about the matter if the war continues to rage and should it have a more pronounced impact on domestic steel markets.

Make your voice heard!

We received responses to this survey from across North America. We truly appreciate it, no matter whether you’re writing in from Canada, Mexico, or the US.

Do you agree with the results above? Do you think we’re missing the mark? Either way, make your voice head. Contact us at smueditorial@crugroup.com if you’d like to participate in our surveys.

Your responses make sure our surveys reflect your company’s experience and help SMU keep its finger on the pulse of the market.