Analysis

July 9, 2026

SMU Survey: Extended sheet lead times take a breather, plate pushes out

Written by Laura Miller

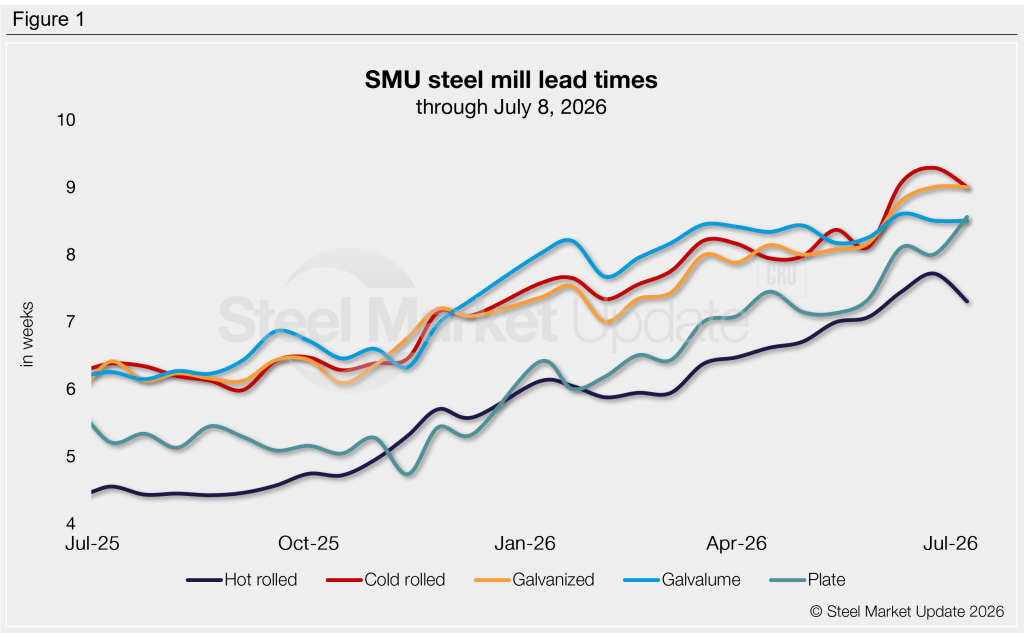

Steel mill lead times for flat-rolled steel this week remained extended at historical highs. Plate production times crept out further, while hot-rolled and cold-rolled (HR/CR) coil saw minor contractions.

Current lead times are now up to a week above where they were in late May and are three to four weeks longer than levels seen last summer.

Current mill production times are basically flat compared to a month ago, with negligible changes. And compared to this time last year, sheet production times are two to three weeks longer, while plate production times are four weeks longer.

Lead time breakdowns

- The average production time for hot-rolled coil is now under seven and a half weeks, a slight pullback from our last survey two weeks ago.

- Lead times for CR and galvanized coil came in at nine weeks, with CR declining and galvanized steady.

- Galvalume lead times are unchanged at eight and a half weeks, following the two-and-a-half-year high seen in early June.

- Plate production times extended by half a week to a five-year high.

Table 1 summarizes current lead times and recent changes by product (click to expand).

Compared to our previous market check, three of our lead-time ranges shifted this week:

- The shortest HR coil lead time considered decreased from six weeks to five weeks.

- The shortest production time for CR coil fell from seven to six.

- The shortest galvanized lead time decreased from seven to six weeks, while the longest increased from 11 to 13 weeks.

Comments

In this week’s survey, a majority (58%) of steel buyers said they believe lead times will be flat two months from now, down from 64% in our previous survey. Those believing they will be extending reached 24%, while those believing they will be contracting was 18%. Comments included:

“[Contracting] Just believe there will be availability.”

“[Contracting] We assume that imports this fall and winter will offset the fall outages. We’ll see, though.”

“[Contracting] I’ve heard that mills are catching up just a bit, perhaps in two months they’ll be even more caught up or contracting compared to the current longer lead times.”

“[Contracting] Turkey will jump back in soon, at least in my opinion.”

“[Flat] Seasonal shutdowns for factories to do maintenance.”

“[Flat] Lead times, like pricing, cannot extend forever, but market is strong, so they will remain extended.”

“Flat and then contracting.”

“[Extending] Stronger demand and constrained supply should gradually push lead times longer over the next two months.”

Trends

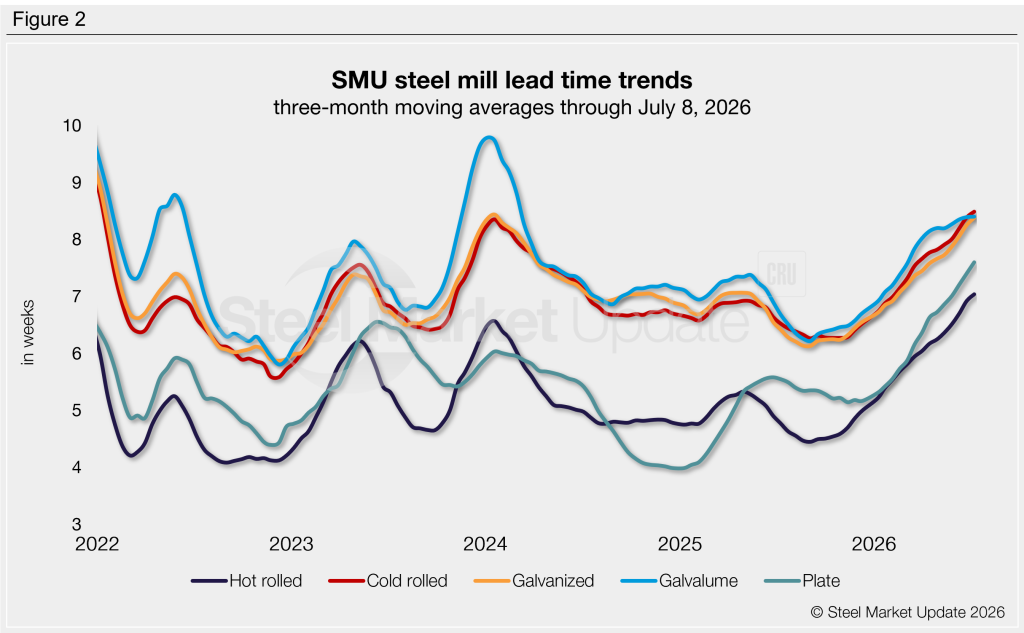

To better highlight underlying trends, lead times can be measured as a three-month moving average (3MMA). All five of our 3MMA lead times ticked higher again this week, a trend in place since late 2025 (Figure 2).

Sheet 3MMA lead times rose by one percentage point for HR, CR, and galvanized, to the highest levels seen since early 2024. Plate’s 3MMA inched up by two percentage points. Galvalume’s was unchanged.

Average lead times by product across the past three months were: HR at 7.0 weeks, CR at 8.5 weeks, galvanized and Galvalume at 8.4 weeks, and plate at 7.6 weeks.

Note: These lead times are based on the average from manufacturers and steel service centers participating in this week’s SMU market trends analysis survey. SMU measures lead times as the time it takes from when an order is placed with the mill to when it is processed and ready for shipping, not including delivery time to the buyer. Our lead times do not predict what any individual may get from any specific mill supplier. Consult your mill rep for actual lead times. Premium members can view an interactive history of our steel mill lead times data on our website. If you’d like to participate in our surveys, contact smu@crugroup.com.