Analysis

July 14, 2026

SMU Price Ranges: HR and CR steady (again) as coated, plate continue to tick upward

Written by Brett Linton & Michael Cowden

Hot-rolled and cold-rolled prices held steady again this week while prices for coated products and plate continued to tick upward.

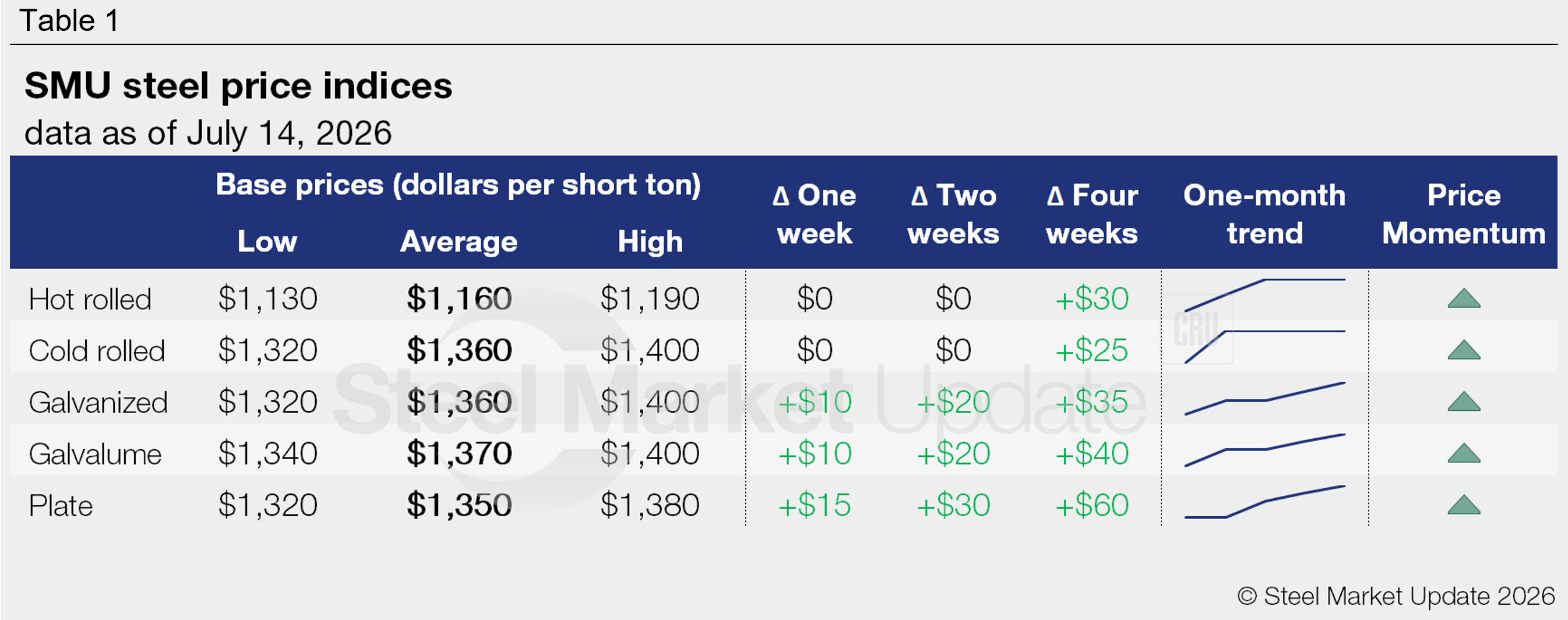

SMU’s hot-rolled (HR) coil price remained at $1,160 per short ton (st) on average and our cold-rolled coil price at $1,360/st on average.

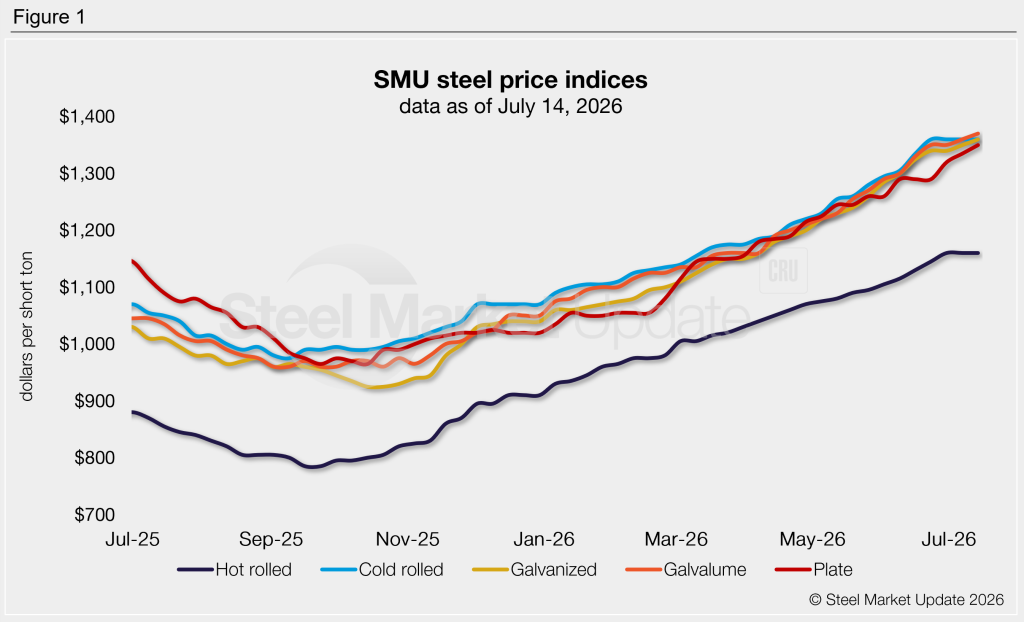

The stability is notable in a market that has trekked steadily higher all year. But most market participants didn’t read much into the flat trend. They chalked it up to the “summer doldrums,” which in past years has seen prices fall.

Many think HR and CR prices will resume their upward trend as more people return to the market following the typically slower summer period. To support that theory, they pointed to continued long lead times and production delays at several mills as well as to, especially on the HR side, persistent shortages.

Coated prices, meanwhile, continued to climb. SMU’s base price for galvanized product stands at $1,360/st and our Galvalume base price at $1,370/st. Both are up $10/st from a week ago.

Market participants attributed the stronger demand for coated products to continued firm demand from the solar and data sectors. Some also noted the impact of a successful trade petition by US mills against imports of coated products from 10 countries.

Take hot-dipped galvanized, for example. Import volumes stood at 242,601 metric tons (mt) in September 2024, the month coated trade petition was filed. Galvanized imports were only 85,023 mt in June, according to license data.

Plate prices, meanwhile, increased to $1,350/st on average this week, up $15/st from last week. The gains come amid a market that has become increasingly tight. They also follow a $40/st price hike announced by SSAB Americas earlier this month.

Market participants said they expected Nucor would also announce a price hike, or at least continue to quietly push prices upward.

SMU’s price momentum indicator remains at higher for both sheet and plate products, signaling we expect prices to increase further in the short term.

Refer to Table 1 (click to enlarge) for our latest price indices and trends.

Hot-rolled coil: $1,130–1,190/st, averaging $1,160/st

The lower end of our range is up $10/st week over week (w/w), while the top end is down $10/st. Our overall average is unchanged w/w.

Hot-rolled lead times range from 5–12 weeks, averaging 7.3 weeks as of our July 8 market survey.

Cold-rolled coil: $1,320–1,400/st, averaging $1,360/st

Our range is unchanged w/w.

Cold-rolled lead times range from 6–12 weeks, averaging 9.0 weeks through our latest survey.

Galvanized coil: $1,320–1,400/st, averaging $1,360/st

The lower end of our range is up $20/st w/w, while the top end is unchanged. Our overall average is up $10/st w/w.

Galvanized .060×48” G90 benchmark: SMU price range is $1,419–1,499/st, averaging $1,459/st FOB mill, east of the Rockies. Note that this spec includes $99/st in mill extras, and extras may vary by mill.

Galvanized lead times range from 6–13 weeks, averaging 9.0 weeks through our latest survey.

Galvalume coil: $1,340–1,400/st, averaging $1,370/st

The lower end of our range is up $20/st w/w, while the top end is unchanged. Our overall average is up $10/st w/w.

Galvalume .0142×42” AZ50, grade 80 benchmark: SMU price range is $1,940–2,000/st, averaging $1,970/st FOB mill, east of the Rockies. Note that this spec includes $600/st in mill extras, and extras may vary by mill.

Galvalume lead times range from 8–11 weeks, averaging 8.5 weeks through our latest survey.

Plate: $1,320–1,380/st, averaging $1,350/st

The lower end of our range is up $10/st w/w, while the top end is up $20/st. Our overall average is up $15/st w/w.

Plate lead times range from 6–12 weeks, averaging 8.6 weeks through our latest survey.

Brett Linton

Read more from Brett Linton