AMU: Midwest, European premiums favoring Canadian producers

Rising Midwest and European premiums are giving Canadian aluminum producers a rare boost, restoring pricing power just ahead of key 2026 negotiations.

Rising Midwest and European premiums are giving Canadian aluminum producers a rare boost, restoring pricing power just ahead of key 2026 negotiations.

U.S. Steel has revised its Galvalume coating extras higher effective Nov. 2, 2025. The steelmaker released new extras to customers on Friday, Sept. 12.

Apparent supply totaled 8.88 million short tons (st) in July, down 38,000 st from June and 6% higher than the same month last year

Sheet prices are expected to increase in the coming weeks in most markets. However, rising domestic capacity in the US, subdued demand in Europe, and high inventory levels in China and India will limit price near-term uptrend.

Active rig counts increased in both the US and Canada last week, according to figures released by Baker Hughes. Although rising, US counts continue to hover just above historic lows. Canadian figures remain comparatively healthy, rising to a six-month high this week. Total US rig counts climbed by two week over week (w/w) to 539. […]

When will we see prime scrap become scarce as the worldwide transition to EAF melting increases, especially for HRC production? It's a question I've been asked a lot.

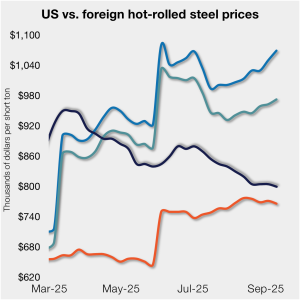

Domestic hot-rolled (HR) coil prices ticked down this week after holding flat since mid-August. Offshore prices largely all moved higher week over week (w/w), widening the margin between stateside and foreign product.

Following a 3% decline in June, the amount of steel shipped outside of the US edged up 1% in July to 623,000 short tons. July was the sixth-lowest monthly export rate since the COVID-19 pandemic, and...

Participants in the hot-rolled steel sheet market expect the market to remain subdued through the end of the year.

The price spread between prime scrap and hot-rolled coil (HRC) narrowed by a hair this month, according to SMU’s most recent pricing data.

Market sources say demand for domestic plate refuses to budge despite stagnating prices.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to tariffs, imports, and evolving market events.

With US economic indicators all over the map, it’s no wonder the steel market has experienced a whole lot of analysis paralysis this year.

Sheet prices were mixed this week as some mills continued to offer significant discounts to larger buyers while others have shifted toward being more disciplined, market participants said.

US steel imports declined for the second consecutive month in July, according to recently finalized US Commerce Department data.

Directors of Anglo American and Teck Resources have conditionally agreed to join together in what they describe as a merger of equals with a focus on copper.

If the steel industry professionals who made it to the very final presentation of this year’s SMU Steel Summit were expecting another round of cautious forecasting, they were in for a surprise. Because what they got was a wake-up call.

SMU’s current Scrap sentiment index increased this month while future sentiment declined, according to our latest ferrous scrap survey data.

Shipments of iron ore across the Great Lakes dropped to 5 million short tons (st) in August, according to the latest data from the Lake Carriers’ Association. That’s down 9.1% compared to August 2024 and 2% lower than the month’s 5-year average. All told, the year-to-date (YTD) iron ore volumes through August totaled 26.7 million […]

SMU’s September ferrous scrap market survey results are now available on our website to all premium members.

Nucor kept hot-rolled (HR) coil prices unchanged this week, according to its latest consumer spot price (CSP) notice on Sept. 8.

A recurring theme in conversations with some of you and in the comments submitted in our surveys is concerns about demand and uncertainty around tariffs. Where does SMU’s latest opinion polling on President Trump’s tariffs stand? Let’s take a look at the numbers.

Here are highlights of what’s happened this past week and a few upcoming things to keep an eye on.

Drilling activity increased in both the US and Canada last week, according to the latest oil and gas rig count data released by Baker Hughes.

Robert Kopf has been on U.S. Steel's acquiring side and is now part of the steelmaker's partnership with Japan’s Nippon Steel, and he sees bright days ahead for the steelmaker.

SMU’s Steel Buyers’ Sentiment Indices ticked higher this week, according to the latest data from our flat-rolled steel survey.

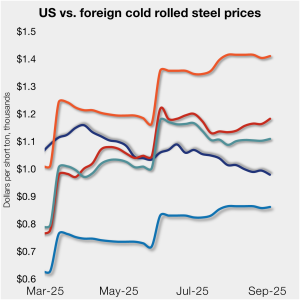

Cold-rolled (CR) coil prices ticked lower in the US this week, while prices in offshore markets diverged and ticked higher.

SMU’s latest steel buyers market survey results are now available on our website to all premium members.

The Brazilian-US pig iron market has remained quiet, market sources told SMU.

he US longs market remained stable this month despite ongoing challenges from tariff-impacted imports, even as end-use demand was relatively unchanged and scrap prices held flat in August.