HRC vs. busheling spread widens again in July

The price spread between prime scrap and hot-rolled coil widened marginally again in July.

The price spread between prime scrap and hot-rolled coil widened marginally again in July.

US oil and gas drilling activity continued to decline for the 11th consecutive week, while Canadian counts climbed for the sixth week in a row, according to the latest data from Baker Hughes.

SMU’s Steel Buyers’ Sentiment Indices moved in opposite directions this week. After rebounding from a near five-year low in late June, Current Sentiment slipped again. At the same time, Future Sentiment climbed to a four-month high. Both indices continue to show optimism among buyers about their company’s chances for success, but suggest there is less confidence in that optimism than earlier in the year.

SMU’s ferrous scrap market survey results are now available on our website to all premium members. After logging in at steelmarketupdate.com, visit the pricing and analysis tab and look under the “survey results” section for “ferrous scrap survey” results. Past scrap survey results are also available under that selection. If you need help accessing the survey results […]

SMU’s latest steel buyers market survey results are now available on our website to all premium members. After logging in at steelmarketupdate.com, visit the pricing and analysis tab and look under the “survey results” section for “latest survey results.” Past survey results are also available under that selection. If you need help accessing the survey results, or if […]

The difference: The spat with Turkey was a big deal for steel. This time, the 50% reciprocal tariff for Brazil – if it goes into effect as threatened on Aug.1 – hits everything from coffee and to pig iron. It seems almost custom-built to inflict as much pain as possible on Brazil.

Mill lead times for sheet products were steady to slightly longer this week compared to our late June market check, while plate lead times contracted, according to steel buyers responding to this week’s market survey.

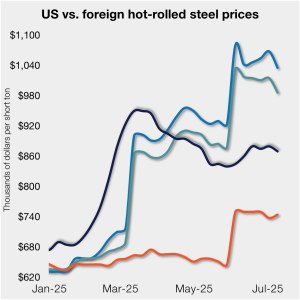

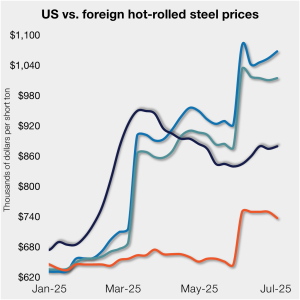

Hot-rolled (HR) coil prices in the US ticked down this week but have fluctuated little over the past month. Stateside tags continue to trail imports from Europe, supported by Section 232 steel tariffs that were doubled in early June.

Domestic mills are more open to talk price on new orders than they were in June, according to most steel buyers responding to our market survey this week. Negotiation rates have recovered from the early-June lull and are now just a few percentage points shy of the high levels seen late last year.

The announcement of 50% tariffs on Brazilian imports, including pig iron, could have a dramatic effect on steelmaking raw materials.

With steel prices drifting and trade flows shifting, CRU analysts provided a grounded look at what's really happening — and what's not — across the metallics supply chain during Wednesday's SMU Community Chat.

President Donald Trump on Wednesday said he would increase the “reciprocal” tariff on imports from Brazil to 50% effective Aug. 1. That could have big implications for pig iron.

Institute for Supply Management CEO Tom Derry will join SMU for our next Community Chat on Wednesday, July 23, at 11 a.m. ET (10 a.m. CT)

The latest SMU Community Chat webinar reply featuring Thais Terzian and Frank Nikolic of CRU Group, is now available on our website to all members. After logging in at steelmarketupdate.com, visit the community tab and look under the “previous webinars” section of the dropdown menu. All past Community Chat webinars are also available under that selection. If you need […]

Are we on the cusp of sorting out the tariff situation, or is this merely another round in the bout?

Sheet and plate prices slipped this week on so-so demand, sideways scrap prices, and chatter that certain mills were making unsolicited calls looking for tons.

Following one of the lowest levels seen in more than two years, US steel imports rebounded from April to May. However, trade remains low relative to recent years. Preliminary license data suggests another fall in June.

CRU Senior Steel Analyst Alexandra Anderson discusses current market and pricing dynamics for long steel products in the US.

The US ferrous scrap market settled sideways in July.

Industry veteran and longtime steel advocate Thomas A. Danjczek announced he will “finally fully retire” as senior advisor of Headwall Partners.

CRU analysts Thais Terzian and Frank Nikolic will be the featured guests on the next SMU Community Chat on Wednesday, July 9, at 11 am ET.

Domestic steel mill output inched higher last week, according to the American Iron and Steel Institute (AISI). Raw production remains historically strong and has been growing steadily since April.

I’m not sure how many different ways I can write that it’s been a quiet market ahead of Independence Day. There are variations on that theme. I’ve heard everything from the ominous “eerily quiet” to "getting better" and even the occasional “blissfully unaware” (because I’m enjoying my vacation).

It will be a shorter week as the United States celebrates Independence Day on Friday. But we won’t leave you high and dry.

US mills shipped slightly less steel in May than in April, according to the latest figures from the American Iron and Steel Institute (AISI).

The United Steelworkers (USW) labor union celebrated recent news of the signed agreement between Atlas Holdings and Evraz NA in which the Connecticut-based private equity company said it plans to acquire North America’s Evraz facilities.

The rig count declined for the 10th consecutive week in the US, while Canadian count rose for the fifth straight week, according to Baker Hughes.

Following the onset of the war in Ukraine in March 2022, concerns about import availability and expectations of rising demand from President Biden’s Infrastructure Bill pushed US rebar prices to record highs. In response, a flurry of new mills and capacity expansions were announced to meet the rise in demand from growth in the construction […]

David Schollaert presents this week's analysis of hot-rolled coil prices, foreign vs. domestic.

Steel buyers this week are lamenting weak demand, cautious buying, and So. Much. Uncertainty. I'm no doctor, but I suggest a dual diagnosis of extreme tariff fatigue and early-onset summer doldrums.