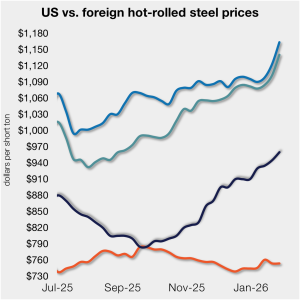

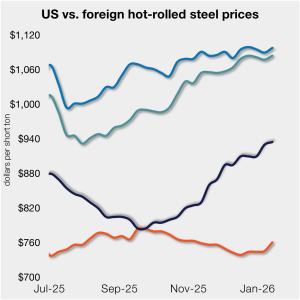

Final Thoughts

At SMU, we ask the big questions: To be or not to be? Hot band at a grand? On the one hand, whether hot-rolled coil price can or can’t go above $1,000 per short (st) is a silly argument. It’s just a number. On the other hand, round numbers are something that we tend to fixate on. They can be psychologically important to a market – even if they shouldn’t be.