SMU price ranges: Sheet moves lower, demand struggling

US sheet prices continued to tick down this week as supply seems to outweigh demand, and deep discounts are not only for large-ton buys.

US sheet prices continued to tick down this week as supply seems to outweigh demand, and deep discounts are not only for large-ton buys.

Nucor said on Monday that it would lower its weekly hot-rolled (HR) coil price effective immediately. In a letter to customers, the company said its consumer spot price (CSP) for the week of June 10 would be $720 per short ton (st), a $60/st cut vs. the prior week. This is not the first big […]

Let’s start by asking this: Were the proclamations that Nucor’s published index prices would drift lower with the reality of a bear market for flat rolled ultimately a bit premature with the benefit of hindsight?

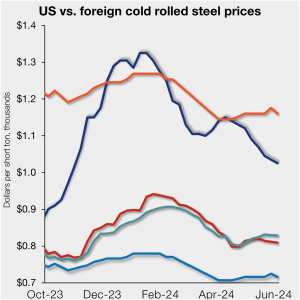

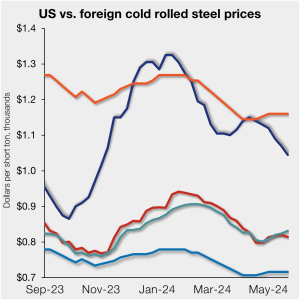

Offshore cold-rolled (CR) coil prices remain notably cheaper than domestic product. That remains the case even as US CR coil prices continue to tick lower.

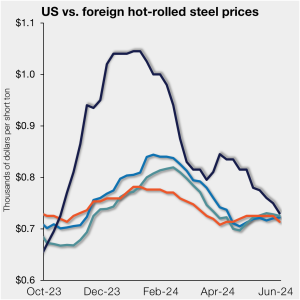

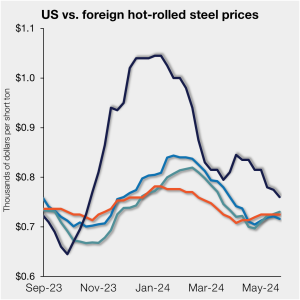

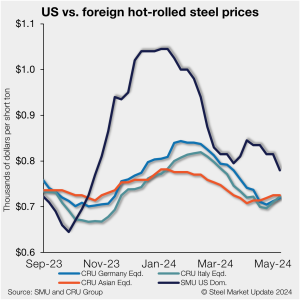

US hot-rolled (HR) coil prices ticked down again this past week, nearly reaching parity with offshore hot band prices on a landed basis. This week, domestic HR coil tags were $730 per short ton (st) on average based on SMU’s latest check of the market on Tuesday, June 4. Domestic HR coil prices are now […]

US sheet prices remained on a downward course again this week amid chatter in some corners about a potential broader slowdown in demand. SMU’s hot-rolled (HR) coil price now stands at $730 per short ton (st) on average, down $20/st from last week and down $115/st from a recent high of $845/st in early April. […]

Nucor will increase galvanized and galvannealed coating extras effective July 6, 2024.

Nucor said on Monday that it would keep its weekly hot-rolled (HR) coil price flat this week. In a letter to customers, the company said its consumer spot price (CSP) for the week of June 3 will remain $780 per short ton (st). The sideways move comes after two consecutive weeks of a $10/st increases […]

Offshore cold-rolled (CR) coil prices remain significantly cheaper than domestic product. That remains the cause even as US CR coil prices continued to tick lower. All told, US CR prices are now 17.6% more expensive than imports. While still high, that premium is down from 19.4% last week and down from 31.5% in early January.

Steel sheet prices across most regions of the world were little changed this week. European buyers remain cautious regarding their outlook towards end-use demand and largely remained out of the market. A similar trend was seen across Asia, although skepticism on real estate stimulus measures in China led to w/w price falls. In the US, […]

Week over week, the futures curve saw minimal change.

US hot-rolled (HR) coil prices ticked down further this past week, moving closer to parity with offshore hot band prices on a landed basis. This week, domestic HR coil tags were $750/st on average based on SMU’s latest check of the market on Tuesday, May 28.

Sheet prices slipped again this week on a combination of moderate demand, increased imports, and higher import volumes.

Nucor moved its published consumer spot price (CSP) up again this week.

Nucor’s Consumer Spot Price (CSP), a legitimate mill offer price, is a potential disruptor to North American steel sheet commercial and procurement strategies. We will dive into the details of what we think the CSP is and why we believe it is a potential disruption to how the North American sheet market operates.

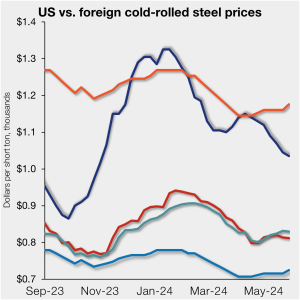

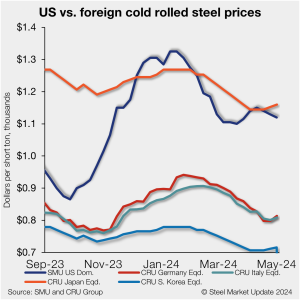

Offshore cold-rolled (CR) coil prices remain a cheaper option over domestic product, even as US CR coil prices tick lower, according to SMU’s latest check of the market.

US hot-rolled (HR) coil prices declined again and now stand nearly even with offshore hot band on a landed basis.

Sideways and range-bound describes the US steel derivatives market over the past week, though the monthly picture shows a more notable decline in front-end flat prices. Week-over-week saw the June futures contract firm slightly, from $770 per short ton (st) to $780/st as of Thursday, May 23’s provisional close. However, the contract was down by […]

Cleveland-Cliffs is seeking at least $800 per short ton (st) for hot-rolled (HR) coil with the opening of its July order book. The Cleveland-based steelmaker said the move was effective immediately in a letter to customers on Thursday, May 23. Recall that Cliffs announced in April that it would publish a monthly HR price. The […]

Nucor upped its published consumer spot price (CSP) this week.

The spread between hot-rolled coil (HRC) and prime scrap prices narrowed this month, according to SMU’s most recent pricing data.

The recent decline in US hot-rolled (HR) coil and longs prices has further restricted demand for imported material. Despite the decline in US sheet prices, CR coil and HDG imports remain attractive. While demand for imports of longs products has been limited, buyers have increased imports of wire products to avoid wire rods’ higher tariffs. […]

The last time we were together on April 18, the June hot-rolled coil (HRC) future was sitting around the $800 support level where the May future found a bottom in mid-February.

Steel prices were overall mixed this week, according to our latest check on the market. Sheet prices were flat to down, while plate prices inched up. SMU indices on hot rolled, cold rolled, and galvanized are now down to the lowest levels seen since November.

Prices for hot-rolled (HR) coil in recent weeks have been declining faster than those for galvanized sheet, resulting in a growing price spread between the two steel products.

US hot-rolled (HR) coil prices declined again, tightening their premium over offshore hot band, and moving closer to parity.

Sheet prices fell across the board this week – largely in response to Nucor’s $65-per-short-ton price cut for hot-rolled (HR) coil on Monday morning. SMU’s HR coil price is $780/st on average, a $35/st decrease week over week (w/w). Our average cold-rolled coil price is $1,090/st (down $30/st w/w). Our galvanized base price is $1,100/st […]

When we were asked to provide some additional commentary to SMU about the futures markets for flat rolled, our only reluctance to contribute was rooted merely in the fact that SMU (1) already offers an excellent array of authors on this topic and (2) a concern regarding what new ground could be covered that hasn’t already been discussed to death on this issue. Thankfully, however, Nucor has offered up something we can describe, without hyperbole, as simply revolutionary for spot pricing in flat rolled - a development that we simply could not resist commenting on with respect to its probable impacts on the futures market.

Nucor started off May with a bang, dropping its weekly base spot price for hot-rolled (HR) coil by $65 per short ton (st) this week.

Foreign cold-rolled (CR) coil remains much less expensive than domestic product even as domestic prices continue to decline, according to SMU’s latest check of the market.